|

市場調查報告書

商品編碼

1998806

神經血管器材市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Neurovascular Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

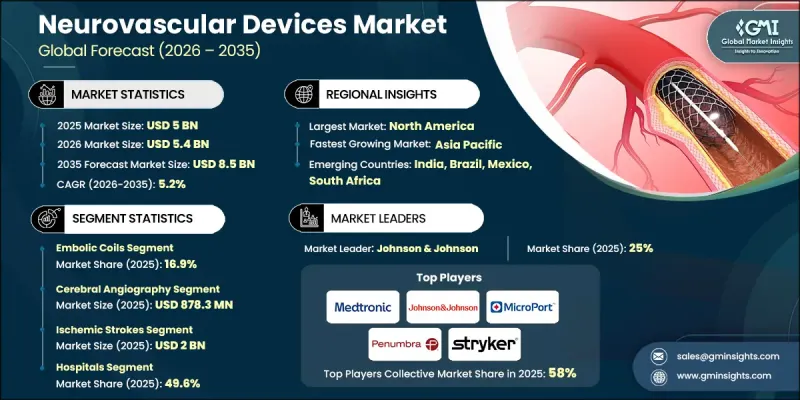

全球神經血管器械市場預計到 2025 年將達到 50 億美元,並預計以 5.2% 的複合年成長率成長,到 2035 年達到 85 億美元。

隨著全球醫療系統面臨日益嚴峻的神經血管疾病挑戰,神經血管器材市場正穩定成長。在對有效治療方法需求不斷成長的推動下,醫院和專科醫療中心正擴大採用旨在治療複雜腦血管疾病的先進醫療技術。推動這一成長的另一個關鍵因素是全球老年人口的增加,他們更容易患上影響大腦和中樞神經系統的血管疾病。器械工程、材料科學和診斷影像技術的不斷整合也有助於提高治療效率和臨床療效。此外,醫療機構越來越傾向於微創手術,這使得醫生能夠更精準地治療複雜的血管疾病,同時縮短患者復原時間並降低手術風險。許多地區的政府正在投資醫療現代化和改善先進醫療技術的可近性,這進一步促進了神經血管器械市場的發展。因此,醫療機構正擴大採用創新的介入神經放射學系統,以提高診斷準確性、治療精準度並支持患者的長期管理。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 50億美元 |

| 預測金額 | 85億美元 |

| 複合年成長率 | 5.2% |

神經血管器械是指專門用於診斷、治療和管理影響大腦和中樞神經系統血管疾病的醫療器械和植入。這些器械通常用於微創手術,旨在恢復正常血液循環、預防血管破裂並降低嚴重神經系統併發症的風險。器材設計、材料和功能的持續創新極大地改變了介入神經放射學手術。現代神經血管技術使醫生能夠進行高度精準的治療,提高手術成功率並最大限度地減少併發症。隨著器械性能的不斷提升,醫療專業人員能夠為複雜的腦血管疾病提供更快、更安全、更有效的治療。這些技術進步正推動神經血管治療從傳統方法轉向高度精確的系統,這些系統旨在支持微創治療並改善患者的復健效果。

預計到2025年,栓塞線圈市場規模將達到8.474億美元,市佔率為16.9%。栓塞線圈是一種用於介入神經放射學手術的專用醫療設備,用於控制或阻斷目標血管內的異常血流。這些器械透過促進受影響血管內可控血栓的形成來發揮作用,從而限制血管異常區域的血流。線圈設計、材料成分和傳輸技術的不斷進步提高了這些器械的安全性和性能。更高的植入精度和器械柔軟性也增強了醫生對這些系統的信心,進一步加速了其在醫療機構中的應用,並促進了神經血管器械市場的整體擴張。

預計到2025年,腦血管造影術市場規模將達到8.783億美元。腦血管造影術是一種基於導管的成像技術,用於評估大腦及其周圍的血管。該技術能夠極為清晰地顯示血管結構,使醫療專業人員能夠識別影響腦循環的異常情況。其產生精確動態影像的能力使其成為腦血管疾病診療中不可或缺的診斷工具。持續投入研發以改善血管造影術技術,正推動先進影像系統的問世。這些創新增強了診斷能力,並促進了用於成像程序的神經血管設備的普及,從而推動了市場擴張。

預計到2025年,北美神經血管器械市佔率將達到34.7%。該地區預計將繼續保持強勁成長,這得益於其先進的醫療基礎設施和醫療設備研發領域的快速技術進步。該地區的醫療機構正日益將創新的神經血管技術應用於臨床實踐,以提高治療效率並改善患者預後。美國憑藉著強大的研發能力和廣泛的專業醫療設施,在先進介入神經放射學器材的研發和應用方面發揮核心作用。對醫療創新持續投入,以及對先進神經血管療法日益成長的需求,鞏固了該地區在全球神經血管器材市場的主導地位。

全球神經血管器材市場涵蓋眾多領導企業,例如旭硝子(Asahi Intecc)、Acandis、Blockade Medical、Balt Extrusion、Integer Holdings Corporation、強生(Johnson & Johnson)、Kaneka Medix Corp、美敦力(Medtronic)、Merit Medical System、微創醫療(MicroPort Scientic Corporation、美敦力(Medtronic)、Merit Medical System、微創醫療(MicroPort Scientific Corporation)、Penbra、Pencoco) Corporation)。主要企業正積極實施各種策略,以鞏固市場地位並拓展全球業務。主要企業大力投資研發,致力於推出能提高治療精準度、手術安全性和臨床療效的先進器械。產品創新始終是企業關注的焦點,尤其注重開發微創技術,並透過材料和設計改進來提升器材性能。與醫療和研究機構建立策略合作夥伴關係也有助於企業加速技術進步並擴大臨床應用。許多製造商正透過建構銷售網路和在新興醫療市場建立合作夥伴關係來拓展地域版圖。此外,各企業都在積極爭取新產品的監管核准,並不斷擴展產品組合,以滿足多樣化的神經血管治療需求,從而在神經血管器械市場保持長期競爭力。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 影響產業的因素

- 成長促進因素

- 神經系統疾病盛行率增加

- 對微創手術的需求日益成長

- 神經血管裝置的技術進步

- 老年人口增加

- 產業潛在風險與挑戰

- 醫療設備高成本

- 嚴格的法規環境

- 市場機遇

- 新興國家醫療保健產業的擴張

- 成長促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 技術進步

- 當前技術趨勢

- 新興技術

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 栓塞線圈

- 頸動脈支架

- 顱內支架

- 導管

- 栓塞預防裝置

- 分流器

- 神經血栓除去裝置

- 膀胱內裝置

- 氣球系統

- 血栓摘取支架

- 導管導引線

- 其他產品

第6章 市場估計與預測:依治療方法分類,2022-2035年

- 神經血栓切除術

- 腦血管造影術

- 頸動脈切除術

- 支架置入術

- 顯微外科夾閉術

- 卷繞

- 流向

- 其他措施

第7章 市場估計與預測:依治療應用分類,2022-2035年

- 腦動脈瘤

- 收縮

- 缺血性中風

- 其他治療用途

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 醫院

- 門診手術中心

- 診所

- 其他最終用戶

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- Asahi Intecc

- Acandis

- Blockade Medical

- Balt Extrusion

- Integer Holdings Corporation

- Johnson &Johnson

- Kaneka Medix Corp

- Medtronic

- Merit Medical System

- MicroPort Scientific Corporation

- Penumbra

- Phenox

- Stryker

- Sensome

- Terumo Corporation

The Global Neurovascular Devices Market was valued at USD 5 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 8.5 billion by 2035.

The neurovascular devices market is witnessing steady expansion as healthcare systems worldwide face a growing burden of neurological vascular disorders. Rising demand for effective treatment solutions is encouraging hospitals and specialized care centers to adopt advanced medical technologies designed to manage complex cerebrovascular conditions. Another major factor supporting growth is the increasing global elderly population, which is more vulnerable to vascular disorders affecting the brain and central nervous system. Continuous progress in device engineering, material science, and imaging integration is also contributing to improvements in treatment efficiency and clinical outcomes. In addition, healthcare providers are increasingly favoring minimally invasive procedures that allow physicians to treat complex vascular conditions with greater precision while reducing patient recovery times and surgical risks. Governments in multiple regions are investing in healthcare modernization and improving access to advanced medical technologies, further supporting the development of the neurovascular devices market. As a result, healthcare institutions are increasingly integrating innovative neuro-interventional systems that enhance diagnostic accuracy, improve treatment precision, and support better long-term patient management.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5 Billion |

| Forecast Value | $8.5 Billion |

| CAGR | 5.2% |

Neurovascular devices refer to specialized medical instruments and implants designed to diagnose, treat, and manage disorders affecting the blood vessels of the brain and central nervous system. These devices are commonly used in minimally invasive procedures aimed at restoring healthy blood circulation, preventing vascular rupture, and lowering the risk of serious neurological complications. Continuous innovation in device design, materials, and functionality has significantly transformed neuro-interventional procedures. Modern neurovascular technologies enable physicians to perform highly precise treatments that improve procedural success rates while minimizing complications. As device capabilities continue to advance, healthcare professionals can deliver faster, safer, and more effective interventions for complex cerebrovascular conditions. The evolution of these technologies has shifted neurovascular treatment from conventional approaches toward highly sophisticated systems designed to support minimally invasive therapeutic procedures and improve patient recovery outcomes.

The embolic coils segment generated USD 847.4 million in 2025 and accounted for 16.9% share. Embolic coils are specialized medical devices utilized in neuro-interventional procedures to control or block abnormal blood flow within targeted vessels. These devices work by promoting controlled clot formation inside the affected vessel, which helps restrict circulation in areas where vascular abnormalities are present. Continuous advancements in coil design, material composition, and delivery technologies have enhanced the safety and performance of these devices. Improvements in deployment accuracy and device flexibility have also strengthened physician confidence in these systems, further encouraging their adoption across healthcare facilities and contributing to the overall expansion of the neurovascular devices market.

The cerebral angiography segment generated USD 878.3 million in 2025. Cerebral angiography is a catheter-based diagnostic imaging procedure used to evaluate blood vessels within the brain and surrounding regions. The technique provides a highly detailed visualization of vascular structures, allowing healthcare professionals to identify abnormalities affecting cerebral circulation. Its ability to produce precise and dynamic imaging makes it an essential diagnostic tool in neurovascular care. Continuous investment in research and product development aimed at improving angiography technologies is leading to the introduction of advanced imaging systems. These innovations are enhancing diagnostic capabilities and supporting the broader adoption of neurovascular devices used in imaging procedures, which is contributing to market expansion.

North America Neurovascular Devices Market accounted for 34.7% share in 2025. The region continues to experience strong growth supported by advanced healthcare infrastructure and rapid technological progress in medical device development. Healthcare providers in the region are increasingly integrating innovative neurovascular technologies into clinical practice to improve treatment efficiency and patient outcomes. The United States plays a central role in both the development and adoption of advanced neuro-interventional devices, supported by strong research capabilities and widespread access to specialized healthcare facilities. Ongoing investments in healthcare innovation, combined with increasing demand for advanced neurovascular treatments, continue to support the region's leading position in the global neurovascular devices market.

Several key companies operate in the Global Neurovascular Devices Market, including Asahi Intecc, Acandis, Blockade Medical, Balt Extrusion, Integer Holdings Corporation, Johnson & Johnson, Kaneka Medix Corp, Medtronic, Merit Medical System, MicroPort Scientific Corporation, Penumbra, Phenox, Stryker, Sensome, and Terumo Corporation. Companies participating in the Global Neurovascular Devices Market are implementing a range of strategies to strengthen their market position and expand global reach. Major players are investing significantly in research and development to introduce advanced devices that improve treatment precision, procedural safety, and clinical efficiency. Product innovation remains a central focus, particularly in developing minimally invasive technologies and enhancing device performance through improved materials and engineering. Strategic partnerships with healthcare institutions and research organizations are also helping companies accelerate technological advancements and expand clinical adoption. Many manufacturers are pursuing geographic expansion by establishing distribution networks and collaborations in emerging healthcare markets. In addition, companies are actively working to secure regulatory approvals for new products while broadening their device portfolios to address diverse neurovascular treatment needs and maintain long-term competitiveness in the neurovascular devices market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Process trends

- 2.2.4 Therapeutic application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of neurological diseases

- 3.2.1.2 Rising demand for minimally invasive surgical procedures

- 3.2.1.3 Technological advancement in neurovascular devices

- 3.2.1.4 Growing geriatric population base

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Growing healthcare expansion in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Impact of AI and generative AI on the market

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Embolic coils

- 5.3 Carotid stents

- 5.4 Intracranial stents

- 5.5 Catheters

- 5.6 Embolic protection devices

- 5.7 Flow diverters

- 5.8 Neurothrombectomy devices

- 5.9 Intrasaccular devices

- 5.10 Balloon systems

- 5.11 Stent retrievers

- 5.12 Guidewires

- 5.13 Other products

Chapter 6 Market Estimates and Forecast, By Process, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Neurothrombectomy

- 6.3 Cerebral angiography

- 6.4 Carotid endarterectomy

- 6.5 Stenting

- 6.6 Microsurgical clipping

- 6.7 Coiling

- 6.8 Flow diversion

- 6.9 Other processes

Chapter 7 Market Estimates and Forecast, By Therapeutic Applications, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Brain aneurysm

- 7.3 Stenosis

- 7.4 Ischemic strokes

- 7.5 Other therapeutic applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Clinics

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Asahi Intecc

- 10.2 Acandis

- 10.3 Blockade Medical

- 10.4 Balt Extrusion

- 10.5 Integer Holdings Corporation

- 10.6 Johnson & Johnson

- 10.7 Kaneka Medix Corp

- 10.8 Medtronic

- 10.9 Merit Medical System

- 10.10 MicroPort Scientific Corporation

- 10.11 Penumbra

- 10.12 Phenox

- 10.13 Stryker

- 10.14 Sensome

- 10.15 Terumo Corporation

神經血管醫療設備市場規模、佔有率、趨勢和預測:按產品、應用、最終用戶和地區分類,2026-2034年

神經血管醫療設備市場規模、佔有率、趨勢和預測:按產品、應用、最終用戶和地區分類,2026-2034年 神經血管介入器材市場:依產品類型、適應症、手術類型及最終用戶分類-2026年至2032年全球市場預測神經血管器材市場:按產品類型、適應症、最終用戶和通路分類的全球市場預測,2026-2032年神經血管和神經系統醫療設備市場:按產品、適應症、技術、最終用戶和分銷管道分類-2026-2032年全球市場預測

神經血管介入器材市場:依產品類型、適應症、手術類型及最終用戶分類-2026年至2032年全球市場預測神經血管器材市場:按產品類型、適應症、最終用戶和通路分類的全球市場預測,2026-2032年神經血管和神經系統醫療設備市場:按產品、適應症、技術、最終用戶和分銷管道分類-2026-2032年全球市場預測 全球神經血管醫療設備市場:市場規模、佔有率和趨勢分析(按器材、治療應用、最終用途和地區分類),基於細分市場的預測(2026-2033 年)

全球神經血管醫療設備市場:市場規模、佔有率和趨勢分析(按器材、治療應用、最終用途和地區分類),基於細分市場的預測(2026-2033 年) 全球出血性中風治療器械市場:按器械類型、中風類型、手術類型、最終用戶、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032年)全球出血性和缺血性中風治療設備市場(按設備類型、治療類型、最終用戶、技術、國家和地區分類)—產業分析、市場規模、市場佔有率和產業預測(2025-2032年)出血性/缺血性中風治療器械市場規模、佔有率和趨勢分析報告:按治療類型、最終用途、地區和細分市場分類,預測期為2026-2033年

全球出血性中風治療器械市場:按器械類型、中風類型、手術類型、最終用戶、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032年)全球出血性和缺血性中風治療設備市場(按設備類型、治療類型、最終用戶、技術、國家和地區分類)—產業分析、市場規模、市場佔有率和產業預測(2025-2032年)出血性/缺血性中風治療器械市場規模、佔有率和趨勢分析報告:按治療類型、最終用途、地區和細分市場分類,預測期為2026-2033年 神經血管器材市場分析及預測(至2035年):依類型、產品類型、技術、應用、最終用戶、材質、器材、製程及功能分類

神經血管器材市場分析及預測(至2035年):依類型、產品類型、技術、應用、最終用戶、材質、器材、製程及功能分類 全球神經血管器材市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球神經血管器材市場規模、佔有率、趨勢和成長分析報告(2026-2034年)