|

市場調查報告書

商品編碼

1998791

陸基遙控武器站市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Land-Based Remote Weapon Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

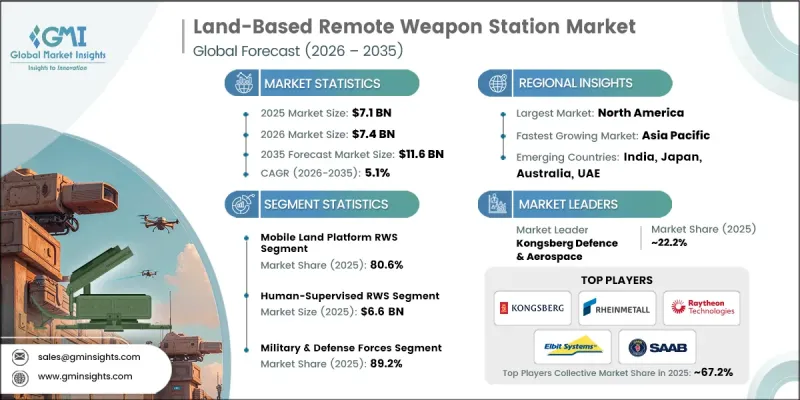

全球陸基遙控武器站市場預計到 2025 年價值 71 億美元,年複合成長率為 5.1%,到 2035 年將達到 116 億美元。

市場擴張的促進因素包括北約和印太地區裝甲車輛現代化項目的增加、非對稱戰爭中對乘員生存能力的日益重視,以及反無人機系統(UAS)解決方案在戰術車輛層面的日益整合。此外,各國軍隊正在將先進的遠程致命系統整合到網路化戰場架構中,並擴大採購輕型、可快速部署的武器站,用於邊防安全和機動作戰。北約東線現代化計畫是主要驅動力,成員國正在提高車輛的生存能力,以應對該地區不斷演變的威脅。隨著各國政府為第一線車輛部署先進的遠程射擊系統,無人砲塔的應用也不斷擴展。在2022年以後的高度複雜和非對稱衝突中,反無人機能力將至關重要,預計車輛層面的整合將持續到2032年。這些創新將提高人員的戰術性防護能力,同時擴展遠程武器系統的作戰多功能性,使其超越傳統的直接射擊能力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 71億美元 |

| 預計金額 | 116億美元 |

| 複合年成長率 | 5.1% |

預計2026年至2035年間,固定式地面遙控武器站市場將以7.3%的複合年成長率成長。這一成長主要得益於在邊境要塞、關鍵基礎設施和前沿作戰基地的部署。日益緊張的跨境局勢和無人機的擴散正在推動對用於周界安全的遠端操控防禦系統的需求。這些系統能夠提供持續監控、自動目標追蹤並降低操作人員的風險,從而提高靜態防禦網路的效能,並刺激持續投資。

預計到2025年,有人值守監視遙控武器站(RWS)市場規模將達66億美元。之所以偏好操作員在環(OITL)系統,是因為國際交戰規則和法規結構要求在民用領域課責並降低風險。軍方之所以青睞監視系統,是因為它們與現有的裝甲車隊和傳統指揮網路相容。這使他們能夠在遵守安全和人道主義標準的同時,保持作戰優勢。

到2025年,北美陸基遙控武器站市佔率將達到33.8%。該地區的成長主要得益於持續的國防現代化項目、不斷成長的國防預算以及先進遙控武器站技術的採購。美國陸軍和國防部的現代化舉措、邊境國防安全保障需求以及成熟的工業基礎,都為該市場提供了支持,使其能夠將遙控武器系統整合到軍隊和安全部隊中。預計到2035年,北美地區對網路化武器、自主作戰系統和邊境防禦能力的重視將持續推動市場穩定成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 成長促進因素

- 提高北約東線戰車的生存能力

- 美國陸軍 CROWS 現代化計劃

- 對無人砲塔整合的需求日益成長

- 步兵戰車數位化

- 輕型遙控武器系統(RWS)在戰術車輛的應用

- 產業潛在風險與挑戰

- 根據《國際武器貿易條例》(ITAR) 實施的出口限制

- 與現有裝甲車輛單元整合的複雜性

- 市場機遇

- 利用人工智慧升級自主目標辨識功能

- 混合動力戰車的整合

- 成長促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依平台類型分類,2022-2035年

- 用於移動地面平台的遙控武器系統(RWS)

- 作戰車輛(裝甲戰車)

- 步兵戰車(IFV)

- 裝甲運兵車(APC)

- 主戰坦克(MBT)-輔助武器

- 戰術車輛

- 聯合輕型戰術車輛(JLTV)

- 防地雷和防伏擊車輛(MRAP)

- 戰術卡車和支援車輛

- 無人地面車輛(UGV)

- 作戰車輛(裝甲戰車)

- 固定地面設施的RWS

- 永久安裝

- 可部署/容器化系統

第6章 市場估價與預測:依武器類型分類,2022-2035年

- 輕武器(5.56毫米至7.62毫米)

- 中型武器(12.7毫米至14.5毫米)

- 重型武器(20毫米至40毫米或更大)

第7章 市場估價與預測:依自動駕駛等級分類,2022-2035年

- 人工監督的RWS

- 自主RWS

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 軍事/國防部隊

- 執法機關和邊防部隊

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- Rheinmetall AG

- BAE Systems plc

- Kongsberg Defence & Aerospace

- 該地區的主要企業

- 北美洲

- General Dynamics Corporation

- RTX Corporation

- 亞太地區

- ASELSAN AS

- Electro Optic Systems

- ST Engineering

- 歐洲

- Saab AB

- Leonardo SpA

- FN Herstal

- 北美洲

- 特殊玩家/干擾者

- Elbit Systems Ltd.

- Rafael Advanced Defense Systems

- Thales Group

The Global Land-Based Remote Weapon Station Market was valued at USD 7.1 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 11.6 billion in 2035.

Market expansion is fueled by increasing armored vehicle modernization programs across NATO and Indo-Pacific regions, the growing emphasis on crew survivability in asymmetric warfare, and the rising integration of counter-UAS solutions at the tactical vehicle level. Military forces are also incorporating advanced remote lethality systems into networked battlefield architectures, while lightweight, rapidly deployable weapon stations are increasingly being procured for border security and mobile operations. NATO Eastern flank modernization programs are a key driver, with member states enhancing vehicle survivability to address evolving regional threats. The adoption of unmanned turrets is gaining traction as governments implement advanced remote fire systems for frontline vehicles. Counter-drone capabilities have become critical in high-intensity and asymmetric conflicts post-2022, and their integration at the vehicle level is expected to continue until 2032. These innovations improve tactical protection for personnel while expanding the operational versatility of remote weapon systems beyond traditional direct-fire functions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.1 Billion |

| Forecast Value | $11.6 Billion |

| CAGR | 5.1% |

The fixed land installation remote weapon stations segment is expected to grow at a CAGR of 7.3% during 2026-2035. This growth is supported by deployments across fortified borders, critical infrastructure, and forward operating bases. Heightened cross-border tensions and the proliferation of drones are driving demand for remotely operated defense systems for perimeter security. These installations offer persistent surveillance, automated target tracking, and reduced operator exposure, which enhances the effectiveness of static defense networks and encourages continued investment.

The human-supervised RWS segment reached USD 6.6 billion in 2025. Preference for operator-in-the-loop systems is driven by international rules of engagement and regulatory frameworks that demand accountability and risk reduction in civilian areas. Military forces favor supervised systems for their compatibility with existing armored vehicle fleets and legacy command networks, which allows them to maintain operational dominance while adhering to safety and humanitarian standards.

North America Land-Based Remote Weapon Station Market held a 33.8% share in 2025. Growth in this region is driven by ongoing defense modernization programs, elevated defense budgets, and procurement of advanced RWS technologies. The market benefits from U.S. Army and Department of Defense modernization initiatives, homeland security requirements along borders, and a well-established industrial base that supports integration of remote weapon systems across military and security forces. North America's focus on networked weapons, autonomous engagement systems, and border defense capabilities is expected to sustain steady growth through 2035.

Key players in the Global Land-Based Remote Weapon Station Market include Kongsberg Defence & Aerospace, Electro Optic Systems, ASELSAN A.S, General Dynamics Corporation, Thales Group, FN Herstal, Elbit Systems Ltd., Rafael Advanced Defense Systems, BAE Systems plc, Leonardo S.p.A, Rheinmetall AG, Saab AB, ST Engineering, and RTX Corporation. Companies operating in the Global Land-Based Remote Weapon Station Market are employing multiple strategies to strengthen their position and expand market share. They are investing in R&D to develop autonomous engagement systems, counter-UAS technologies, and lightweight modular weapon stations. Strategic alliances with defense agencies and technology firms allow integration of advanced systems into existing fleets. Manufacturers are also expanding production capacity, establishing regional service centers, and offering operator training programs. Emphasis on interoperability, networked battlefield solutions, and modular designs enables rapid upgrades and multi-platform deployment.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Platform type trends

- 2.2.2 Weapon type trends

- 2.2.3 Autonomy level trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 NATO Eastern flank vehicle survivability upgrades

- 3.2.1.2 U.S. Army CROWS modernization programs

- 3.2.1.3 Rising demand for unmanned turret integration

- 3.2.1.4 Infantry fighting vehicle fleet digitization

- 3.2.1.5 Lightweight RWS adoption on tactical vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Export restrictions under ITAR regulations

- 3.2.2.2 Integration complexity with legacy armored fleets

- 3.2.3 Market opportunities

- 3.2.3.1 AI-enabled autonomous target recognition upgrades

- 3.2.3.2 Hybrid electric combat vehicle integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Mobile land platform RWS

- 5.2.1 Combat vehicles (armored fighting vehicles)

- 5.2.1.1 Infantry fighting vehicles (IFVs)

- 5.2.1.2 Armored personnel carriers (APCs)

- 5.2.1.3 Main battle tanks (MBTs)-secondary armament

- 5.2.2 Tactical Vehicles

- 5.2.2.1 Joint light tactical vehicles (JLTV)

- 5.2.2.2 Mine-resistant ambush protected (MRAP) vehicles

- 5.2.2.3 Tactical trucks & logistics vehicles

- 5.2.3 Unmanned ground vehicles (UGVs)

- 5.2.1 Combat vehicles (armored fighting vehicles)

- 5.3 Fixed land installation RWS

- 5.3.1 Permanent installations

- 5.3.2 Deployable / containerized systems

Chapter 6 Market Estimates and Forecast, By Weapon Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Light (5.56mm - 7.62mm)

- 6.3 Medium (12.7mm - 14.5mm)

- 6.4 Heavy (20mm - 40mm+)

Chapter 7 Market Estimates and Forecast, By Autonomy Level, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Human-supervised RWS

- 7.3 Autonomous engagement RWS

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Military & defense forces

- 8.3 Law enforcement & border security forces

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Rheinmetall AG

- 10.1.2 BAE Systems plc

- 10.1.3 Kongsberg Defence & Aerospace

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 General Dynamics Corporation

- 10.2.1.2 RTX Corporation

- 10.2.2 Asia Pacific

- 10.2.2.1 ASELSAN A.S

- 10.2.2.2 Electro Optic Systems

- 10.2.2.3 ST Engineering

- 10.2.3 Europe

- 10.2.3.1 Saab AB

- 10.2.3.2 Leonardo S.p.A

- 10.2.3.3 FN Herstal

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Elbit Systems Ltd.

- 10.3.2 Rafael Advanced Defense Systems

- 10.3.3 Thales Group