|

市場調查報告書

商品編碼

1998790

動物飼料防腐劑市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Animal Feed Preservatives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

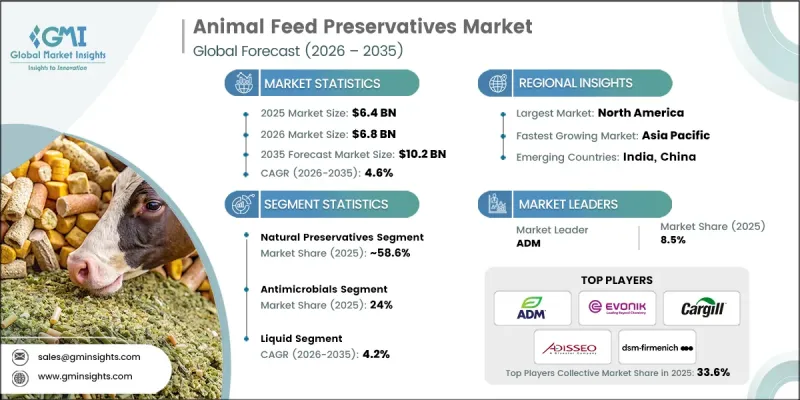

全球動物飼料防腐劑市場預計到 2025 年價值 64 億美元,預計到 2035 年將以 4.6% 的複合年成長率成長至 102 億美元。

動物飼料防腐劑市場已發展成為飼料和畜牧業價值鏈不可或缺的環節。防腐劑最初主要用於延長飼料的保存期限,如今其作用已顯著擴展,涵蓋維持飼料品質、保存必需營養成分以及最大限度降低畜牧養殖戶的生產風險。現代畜牧業依賴防腐劑在各種環境、儲存和運輸條件下保持飼料的穩定性,使其成為現代飼料管理策略中不可或缺的組成部分。在日益關注動物健康、食品安全和可靠供應鏈的推動下,飼料生產商正在採用更先進的保鮮技術。因此,各公司正在開發旨在支持潔淨標示的配方,同時提供抗菌保護,防止污染和腐敗。相關人員也正在投資先進的保鮮解決方案,這些方案透過減少廢棄物、改善原料處理以及延長飼料原料在儲存和運輸過程中的保存期限來提高營運效率。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 64億美元 |

| 預測金額 | 102億美元 |

| 複合年成長率 | 4.6% |

預計到2025年,天然防腐劑市佔率將達到58.6%,並在2035年之前以4.7%的複合年成長率成長。隨著畜牧養殖戶越來越重視更安全、更永續的飼料原料,該細分市場的重要性日益凸顯。天然防腐劑解決方案之所以被廣泛採用,是因為它們符合不斷發展的負責任畜牧養殖監管標準以及消費者日益成長的期望。這些防腐劑能夠有效防止微生物污染,同時滿足消費者對注重透明度、永續性和減少合成添加劑依賴的飼料產品日益成長的需求。

預計到2025年,抗菌劑市佔率將達到24%,並在2026年至2035年間以4.7%的複合年成長率成長。抗菌防腐劑應用廣泛,因為它們有助於保護飼料產品免受有害微生物的侵害,這些微生物會損害飼料品質和動物健康。抗菌劑在儲存、運輸和處理過程中有效抑制微生物生長,使其成為飼料保存策略的關鍵組成部分。這些解決方案透過維護衛生和降低集約化和大規模畜牧養殖中的污染風險,支持安全的飼料管理實踐。

至2025年,北美動物飼料防腐劑市場將佔據31.5%的市場。該地區擁有高度發展的畜牧業體系和成熟的飼料生產產業,這些產業高度重視品質和合規性。嚴格的飼料安全、污染控制和生物安全產業標準正在推動對先進防腐技術的需求。隨著畜牧養殖戶致力於保持飼料品質穩定並提高營運效率,該地區的大型飼料生產系統對先進防腐解決方案的需求持續成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 成長促進因素

- 對優質動物飼料的需求不斷增加

- 意識提高和廣泛採用

- 嚴格的法規和對食品安全的擔憂

- 產業潛在風險與挑戰

- 成本考量

- 環境和健康問題

- 市場機遇

- 對天然和有機防腐劑的需求日益成長

- 精準營養和數位化配方技術的進步

- 成長促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按防腐劑類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依防腐劑類型分類,2022-2035年

- 天然防腐劑

- 植物萃取物

- 精油

- 有機酸

- 生育酚(維生素E)

- 合成防腐劑

- BHA

- BHT

- 乙氧喹

- 丙酸

- 甲酸

第6章 市場估計與預測:依化合物類型分類,2022-2035年

- 飼料酸化劑

- 抗氧化劑

- 抗菌劑

- 黴菌抑制劑

- 黴菌毒素吸附劑

- 抗結塊劑

第7章 市場估計與預測:依類型分類,2022-2035年

- 液體

- 水溶液

- 油性懸浮液

- 乾燥

- 粉末

- 顆粒

- 顆粒

第8章 市場估計與預測:依飼料類型分類,2022-2035年

- 複合飼料

- 飼料預混合料

- 青貯飼料

- 動物飼料用穀物

第9章 市場估計與預測:依動物類型分類,2022-2035年

- 家禽

- 肉雞

- 產蛋母雞

- 火雞

- 豬

- 起動機

- 發展期

- 種母豬

- 牛

- 乳製品

- 牛肉

- 牛

- 水產養殖

- 鮭魚

- 鱒魚

- 蝦

- 鯉魚

- 吳郭魚

- 寵物食品

- 狗

- 貓

- 其他寵物

- 馬

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第11章:公司簡介

- Cargill, Incorporated

- ADM

- BASF SE

- Evonik Industries AG

- IFF

- Kemin Industries

- DSM-Firmenich AG

- Nutreco NV

- Adisseo

- Novus International

- Alltech, Inc.

- Phibro Animal Health

- Solvay SA

- Novonesis Group

The Global Animal Feed Preservatives Market was valued at USD 6.4 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 10.2 billion by 2035.

The animal feed preservatives market has evolved into a vital component of the broader feed and livestock value chain. While preservatives were originally introduced primarily to extend feed shelf life, their role has significantly expanded to include maintaining feed quality, preserving essential nutrients, and minimizing production risks for livestock producers. Modern livestock operations rely on preservatives to maintain feed stability across diverse environmental, storage, and transportation conditions, making them an essential element of contemporary feed management strategies. Increasing focus on animal health, food safety, and reliable supply chains is encouraging feed manufacturers to adopt higher-performance preservation technologies. As a result, companies are developing formulations designed to support clean labeling practices while providing antimicrobial protection that helps limit contamination and spoilage. Industry stakeholders are also investing in advanced preservation solutions that improve operational efficiency by reducing waste, improving ingredient handling, and extending the usability of feed materials during storage and distribution.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.4 Billion |

| Forecast Value | $10.2 Billion |

| CAGR | 4.6% |

The natural preservatives segment accounted for 58.6% share in 2025 and is projected to grow at a CAGR of 4.7% through 2035. This segment has gained prominence as livestock producers increasingly prioritize safer and more sustainable feed ingredients. Natural preservative solutions are being widely adopted because they align well with evolving regulatory standards and rising consumer expectations regarding responsible livestock production. These preservatives offer effective protection against microbial contamination while supporting the growing demand for feed products that emphasize transparency, sustainability, and reduced reliance on synthetic additives.

The antimicrobial segment held 24% share in 2025 and is expected to grow at a CAGR of 4.7% between 2026 and 2035. Antimicrobial preservatives are widely utilized because they help protect feed products from harmful microorganisms that can compromise both feed quality and animal health. Their effectiveness in preventing microbial growth during storage, transportation, and handling makes them a critical component of feed preservation strategies. These solutions support safe feed management practices by maintaining hygienic conditions and reducing the risk of contamination across both intensive and large-scale livestock operations.

North America Animal Feed Preservatives Market held 31.5% share in 2025. The region benefits from highly developed livestock production systems and a well-established feed manufacturing industry that emphasizes quality and regulatory compliance. Strong industry standards related to feed safety, contamination control, and biosecurity have increased the demand for advanced preservation technologies. As livestock producers focus on maintaining consistent feed quality and improving operational efficiency, adoption of advanced preservative solutions continues to rise across large-scale feed production systems in the region.

Major companies operating in the Global Animal Feed Preservatives Market include BASF SE, Cargill, Incorporated, ADM, Evonik Industries AG, DSM-Firmenich AG, Kemin Industries, IFF, Nutreco N.V., Adisseo, Novus International, Alltech, Inc., Phibro Animal Health, Solvay S.A., and Novonesis Group. Companies active in the Animal Feed Preservatives Market are strengthening their competitive position through innovation, strategic collaborations, and expanded production capabilities. Leading firms are investing in research and development to create advanced preservative formulations that improve feed stability while meeting evolving regulatory standards and sustainability expectations. Many companies are also focusing on developing naturally derived preservation solutions to address the growing demand for clean-label livestock feed products. Strategic partnerships with feed manufacturers and livestock producers are helping companies expand their product applications and strengthen market reach. In addition, organizations are enhancing their global distribution networks and improving supply chain capabilities to support consistent product availability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Preservative Type

- 2.2.3 Compound Type

- 2.2.4 Form

- 2.2.5 Feed Type

- 2.2.6 Animal Type

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for high-quality animal nutrition

- 3.2.1.2 Rising awareness and adoption

- 3.2.1.3 Stringent regulations and food safety concerns

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cost concerns

- 3.2.2.2 Environmental and health concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for natural & organic preservatives

- 3.2.3.2 Advances in precision nutrition & digital formulation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By preservative type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Preservative Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Natural preservatives

- 5.2.1 Plant extracts

- 5.2.2 Essential oils

- 5.2.3 Organic acids

- 5.2.4 Tocopherols (Vitamin E)

- 5.3 Synthetic preservatives

- 5.3.1 BHA

- 5.3.2 BHT

- 5.3.3 Ethoxyquin

- 5.3.4 Propionic acid

- 5.3.5 Formic acid

Chapter 6 Market Estimates and Forecast, By Compound Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Feed acidifiers

- 6.3 Antioxidants

- 6.4 Antimicrobials

- 6.5 Mold inhibitors

- 6.6 Mycotoxin binders

- 6.7 Anti-caking agents

Chapter 7 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Liquid

- 7.2.1 Aqueous Solutions

- 7.2.2 Oil-Based Suspensions

- 7.3 Dry

- 7.3.1 Powders

- 7.3.2 Granules

- 7.3.3 Pellets

Chapter 8 Market Estimates and Forecast, By Feed Type, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Compound Feed

- 8.3 Feed Premix

- 8.4 Silage

- 8.5 Feed Meal

Chapter 9 Market Estimates and Forecast, By Animal Type, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Poultry

- 9.2.1 Broiler

- 9.2.2 Layer

- 9.2.3 Turkey

- 9.3 Swine

- 9.3.1 Starter

- 9.3.2 Grower

- 9.3.3 Sow

- 9.4 Cattle

- 9.4.1 Dairy

- 9.4.2 Beef

- 9.4.3 Calf

- 9.5 Aquaculture

- 9.5.1 Salmon

- 9.5.2 Trout

- 9.5.3 Shrimp

- 9.5.4 Carp

- 9.5.5 Tilapia

- 9.6 Pet Food

- 9.6.1 Dog

- 9.6.2 Cat

- 9.6.3 Other Pets

- 9.7 Equine

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Cargill, Incorporated

- 11.2 ADM

- 11.3 BASF SE

- 11.4 Evonik Industries AG

- 11.5 IFF

- 11.6 Kemin Industries

- 11.7 DSM-Firmenich AG

- 11.8 Nutreco N.V.

- 11.9 Adisseo

- 11.10 Novus International

- 11.11 Alltech, Inc.

- 11.12 Phibro Animal Health

- 11.13 Solvay S.A.

- 11.14 Novonesis Group

茶皂素市場規模、佔有率和成長分析:按產品類型、應用、純度、最終用戶、分銷管道和地區分類-2026-2033年產業預測

茶皂素市場規模、佔有率和成長分析:按產品類型、應用、純度、最終用戶、分銷管道和地區分類-2026-2033年產業預測 動物消化物市場規模、佔有率和成長分析:按原料、形態、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測

動物消化物市場規模、佔有率和成長分析:按原料、形態、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測 動物消化:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)動物飼料防腐劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

動物消化:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)動物飼料防腐劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 合成飼料添加劑市場規模、佔有率和成長分析:依產品類型、牲畜種類、劑型、通路和地區分類-2026-2033年產業預測

合成飼料添加劑市場規模、佔有率和成長分析:依產品類型、牲畜種類、劑型、通路和地區分類-2026-2033年產業預測 飼料添加劑市場:依產品類型、牲畜類型和地區分類

飼料添加劑市場:依產品類型、牲畜類型和地區分類 藥用飼料市場規模、佔有率和成長分析:按產品類型、動物種類、配方、通路和地區分類-2026-2033年產業預測

藥用飼料市場規模、佔有率和成長分析:按產品類型、動物種類、配方、通路和地區分類-2026-2033年產業預測 動物飼料用沸石市場規模、佔有率和成長分析:按沸石類型、牲畜類型、配方類型、給藥途徑、地區和產業預測,2026-2033年

動物飼料用沸石市場規模、佔有率和成長分析:按沸石類型、牲畜類型、配方類型、給藥途徑、地區和產業預測,2026-2033年 全球動物飼料添加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球動物飼料添加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 動物飼料添加劑市場規模、佔有率和成長分析(按產品類型、畜種、形態、功能和地區分類)-2026-2033年產業預測

動物飼料添加劑市場規模、佔有率和成長分析(按產品類型、畜種、形態、功能和地區分類)-2026-2033年產業預測