|

市場調查報告書

商品編碼

1998788

駕駛警告系統市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Driver Alert System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

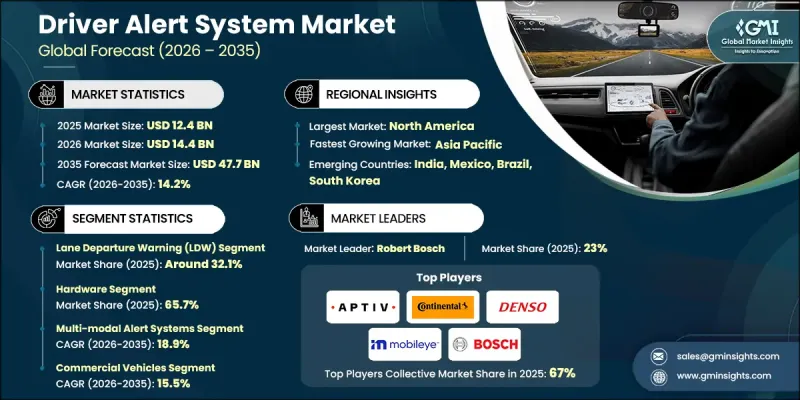

全球駕駛員警報系統市場預計到 2025 年將達到 124 億美元,並將以 14.2% 的複合年成長率成長,到 2035 年達到 477 億美元。

人為失誤仍是全球交通事故的主要原因之一,促使各國政府推出法規,強制要求車輛安裝先進的安全技術。汽車製造商正日益將駕駛警告系統整合到乘用車和商用車中,作為高級駕駛輔助系統(ADAS)的一部分。這些系統利用人工智慧、攝影機、紅外線感測器和轉向輸入監控技術,追蹤眼瞼運動、視線方向和頭部位置,以偵測駕駛者的疲勞和注意力分散。系統透過視覺、聽覺或觸覺訊號發出警告,幫助預防事故發生。人工智慧感知技術、多感測器融合和深度學習模型的日益普及,提高了檢測精度,減少了誤報,並增強了系統在各種環境條件下的可靠性。日益成長的監管壓力和對道路安全更高要求的推動,正促使全球多個細分市場不斷擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 124億美元 |

| 預測金額 | 477億美元 |

| 複合年成長率 | 14.2% |

車道偏離預警(LDW)系統目前佔據32.1%的市場佔有率,預計2025年市場規模將達到40億美元。 LDW系統有助於防止車輛偏離車道,從而有效應對交通事故的主要原因之一。透過在車輛偏離車道前發出警告,這些系統能夠提高安全性,降低事故相關成本,並滿足消費者和監管機構的期望。 LDW技術的日益普及正在擴大市場滲透率和收入,以鞏固其作為現代車輛關鍵安全解決方案的地位。隨著高級駕駛輔助系統(ADAS)的日益普及,預計該細分市場在乘用車和商用車領域都將持續成長。

預計到2025年,硬體部分將佔據65.7%的市場佔有率,到2035年將達到300億美元。高解析度攝影機、雷達、LiDAR感測器和超音波設備等關鍵組件能夠即時監測車道變更、碰撞和駕駛員注意力。 800萬至1200萬像素攝影機、角解析度更高的雷達以及速度提升10至100倍的人工智慧處理器等技術進步,顯著提高了偵測精度,即使在惡劣天氣條件下也能保持效能。這些改進使駕駛員預警系統能夠有效識別疲勞、分心和駕駛員意圖,同時保持能源效率和溫度控管。

預計2025年,美國駕駛警告系統市場規模將達42億美元。強勁的汽車產量、消費者對安全性的偏好重視以及嚴格的監管正在推動該地區市場的成長。由美國國家公路交通安全管理局(NHTSA)和新車評估項目(NCAP)等監管機構主導的項目,正在促進盲點監測、車道維持輔助和自動緊急煞車等先進安全功能的整合。這些措施鼓勵汽車製造商更廣泛地採用駕駛警告技術,進一步推動市場擴張。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 嚴格的政府安全法規和義務

- 消費者對道路安全的意識日益增強

- 車隊營運商對駕駛員監控的需求

- 與自動駕駛系統的整合

- 產業潛在風險與挑戰

- 先進DAS組件的初始成本較高

- 各區域之間缺乏標準化

- 市場機遇

- 隨著汽車銷售的成長,新興市場的擴張也不斷推進。

- 現有車輛的售後改裝解決方案

- 人工智慧驅動的個人化警報系統

- 商用車和物流行業的成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國國家公路交通安全管理局(NHTSA)

- 聯邦機動車輛安全標準(FMVSS)

- 歐洲

- 歐盟委員會

- UNECE WP.29

- 歐盟通用安全法規 (GSR) 2019/2144

- 亞太地區

- Japan NCAP

- 中國新車評測

- AIS(汽車產業標準)

- 拉丁美洲

- 巴西國家交通委員會(CONTRAN)

- INMETRO

- ANSV

- 中東和非洲

- 海灣標準化組織(GSO)

- ESMA(阿拉伯聯合大公國標準化和計量局)

- 北美洲

- 投資與資金籌措分析

- 創業投資與私募股權的發展趨勢

- 企業投資趨勢

- 政府資金和獎勵

- 併購交易趨勢分析

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 基於人工智慧的駕駛員監控系統(DMS)

- 感測器融合整合

- 紅外線(IR)攝影機的引入

- 與ADAS平台整合

- 新興技術

- 利用雷達進行車載監控

- 人工智慧驅動的行為預測模型

- 利用人工智慧技術的自適應警報系統

- 當前技術趨勢

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按球員類型分類的定價策略(高階/超值/成本加成)

- 原廠配套產品與售後市場產品之間的價格差異

- 區域價格波動分析

- 專利趨勢(基於初步調查)

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- GenAI 各細分市場的應用案例與部署藍圖

- 風險、限制和監管考量

- 與自動駕駛和ADAS生態系統的整合

- 感測器資料共用和融合架構

- V2X通訊的整合

- 自動駕駛和手動駕駛之間的切換通訊協定

- 冗餘和故障安全機制

- 網路安全與功能安全分析

- 網路安全威脅與攻擊途徑

- 加密和資料保護通訊協定

- 安全關鍵系統的檢驗

- 空中下載 (OTA) 更新的安全性

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要製造商分類的產能

- 運轉率和擴張計劃

- 案例研究

- 未來展望與機遇

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估計與預測:依系統分類,2022-2035年

- 車道偏離預警(LDW)

- 前向碰撞警報(FCW)

- 盲點偵測(BSD)

- 駕駛員疲勞監測系統(DFM)

- 駕駛分心檢測

- 其他

第6章 市場估計與預測:依解法分類,2022-2035年

- 硬體

- 感應器

- 相機

- 其他

- 軟體

- 車上用軟體

- 基於行動應用程式

第7章 市場估算與預測:依 Alert 分類,2022-2035 年

- 視覺警告系統

- 語音警報系統

- 觸覺警報系統

- 多模態警報系統

第8章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- LCV

- MCV

- 重型車輛(HCV)

第9章 市場估價與預測:依通路分類,2022-2035年

- OEM

- 售後市場

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 比利時

- 俄羅斯

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 世界公司

- Robert Bosch

- Continental

- DENSO

- ZF

- Aptiv

- Magna

- Autoliv

- Mobileye

- Valeo

- Hyundai Mobis

- 本地球員

- Smart Eye

- Seeing Machines

- Ficosa

- Visteon

- Harman

- Faurecia

- 新興企業

- Jungo Connectivity

- Affectiva

- Xperi/Perceive

- Neonode

The Global Driver Alert System Market was valued at USD 12.4 billion in 2025 and is estimated to grow at a CAGR of 14.2% to reach USD 47.7 billion by 2035.

Human error remains the leading cause of road accidents worldwide, prompting governments to implement regulations mandating advanced safety technologies in vehicles. Automakers are increasingly integrating driver alert systems into passenger and commercial vehicles as part of Advanced Driver Assistance Systems (ADAS). These systems utilize AI, cameras, infrared sensors, and steering input monitoring to track eyelid movement, gaze direction, and head position, allowing them to detect driver fatigue or distraction. Alerts are delivered through visual, auditory, or tactile signals, helping prevent accidents before they occur. The growing adoption of AI-powered perception, multi-sensor fusion, and deep learning models is enhancing detection accuracy, reducing false alarms, and improving system reliability under varying environmental conditions. Rising regulatory pressure and the demand for improved road safety are driving market expansion across multiple vehicle segments globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.4 Billion |

| Forecast Value | $47.7 Billion |

| CAGR | 14.2% |

The lane departure warning (LDW) segment held a 32.1% share, generating USD 4 billion in 2025. LDW systems help prevent vehicles from drifting out of lanes, addressing one of the primary causes of traffic accidents. By alerting drivers before lane departures, these systems enhance safety, reduce accident-related costs, and meet both consumer and regulatory expectations. Widespread adoption of LDW technology has boosted market penetration and revenue, solidifying its position as a key safety solution in modern vehicles. Increasing inclusion in ADAS packages ensures continued growth for this segment across both passenger and commercial vehicles.

The hardware segment accounted for 65.7% share in 2025 and is expected to reach USD 30 billion by 2035. Critical components such as high-resolution cameras, radar, LiDAR sensors, and ultrasonic devices enable real-time monitoring of lane changes, collisions, and driver alertness. Technological advances, including 8-12 MP cameras, radar with improved angular resolution, and AI processors offering 10-100X faster performance, have significantly enhanced detection accuracy even in adverse weather. These improvements allow driver alert systems to effectively identify fatigue, distraction, and driver intentions while maintaining energy efficiency and thermal management.

United States Driver Alert System Market reached USD 4.2 billion in 2025. Strong automotive manufacturing, consumer preference for safety, and stringent regulations are driving growth in the region. Programs led by regulatory bodies such as the National Highway Traffic Safety Administration (NHTSA) and New Car Assessment Program (NCAP) encourage the integration of advanced safety features, including blind-spot detection, lane-keeping assist, and automatic emergency braking. These initiatives incentivize automakers to incorporate driver alert technologies more broadly, reinforcing market expansion.

Key companies operating in the Global Driver Alert System Market include Mobileye, Autoliv, Aptiv, Robert Bosch, ZF, Valeo, Hyundai Mobis, Magna, DENSO, and Continental. Companies in the Global Driver Alert System Market are strengthening their position through strategic investments in AI and sensor technology, enhancing detection accuracy and system reliability. Leading manufacturers are expanding partnerships with automakers to integrate driver alert systems into new models and ADAS packages. Firms are investing in research and development for multi-sensor fusion and machine learning algorithms to reduce false alerts and improve performance in diverse conditions. Geographic expansion into emerging automotive markets supports broader adoption. Companies are also focusing on compliance with evolving safety regulations, offering tailored solutions for passenger and commercial vehicles.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System

- 2.2.3 Solution

- 2.2.4 Alert

- 2.2.5 Vehicle

- 2.2.6 Distribution Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent government safety regulations & mandates

- 3.2.1.2 Rising consumer awareness on road safety

- 3.2.1.3 Fleet operator demand for driver monitoring

- 3.2.1.4 Integration with autonomous driving systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of advanced DAS components

- 3.2.2.2 Lack of standardization across regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets with growing vehicle sales

- 3.2.3.2 Aftermarket retrofit solutions for existing fleets

- 3.2.3.3 AI-powered personalized alert systems

- 3.2.3.4 Commercial vehicle & logistics sector growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Federal Motor Vehicle Safety Standards (FMVSS)

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 UNECE WP.29

- 3.4.2.3 EU General Safety Regulation (GSR) 2019/2144

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan NCAP

- 3.4.3.2 China NCAP

- 3.4.3.3 AIS (Automotive Industry Standards)

- 3.4.4 Latin America

- 3.4.4.1 Brazil National Traffic Council (CONTRAN)

- 3.4.4.2 INMETRO

- 3.4.4.3 ANSV

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Standardization Organization (GSO)

- 3.4.5.2 Emirates Authority for Standardization and Metrology (ESMA)

- 3.4.1 North America

- 3.5 Investment & Funding Analysis

- 3.5.1 Venture Capital & Private Equity Activity

- 3.5.2 Corporate Investment Trends

- 3.5.3 Government Funding & Incentives

- 3.5.4 M&A Deal Flow Analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.1.1 AI-based driver monitoring systems (DMS)

- 3.8.1.2 Sensor fusion integration

- 3.8.1.3 Infrared (IR) camera deployment

- 3.8.1.4 Integration with ADAS platforms

- 3.8.2 Emerging technologies

- 3.8.2.1 Radar-based in-cabin monitoring

- 3.8.2.2 AI-powered behavioral prediction models

- 3.8.2.3 Generative AI-assisted adaptive alert systems

- 3.8.1 Current technological trends

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus)

- 3.9.3 OEM vs Aftermarket Price Differentiation

- 3.9.4 Regional Price Variation Analysis

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Integration with autonomous & ADAS ecosystem

- 3.12.1 Sensor data sharing & fusion architectures

- 3.12.2 V2X communication integration

- 3.12.3 Handover protocols between automated & manual driving

- 3.12.4 Redundancy & fail-safe mechanisms

- 3.13 Cybersecurity & functional safety analysis

- 3.13.1 Cybersecurity threats & attack vectors

- 3.13.2 Encryption & data protection protocols

- 3.13.3 Safety-critical system validation

- 3.13.4 Over-the-Air (OTA) update security

- 3.14 Capacity & production landscape (Driven by Primary Research)

- 3.14.1 Installed capacity by region & key producer

- 3.14.2 Capacity utilization rates & expansion pipelines

- 3.15 Case studies

- 3.16 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By System, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Lane Departure Warning (LDW)

- 5.3 Forward Collision Warning (FCW)

- 5.4 Blind Spot Detection (BSD)

- 5.5 Driver Fatigue Monitor (DFM)

- 5.6 Driver Distraction Detection

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 Sensors

- 6.2.2 Cameras

- 6.2.3 Others

- 6.3 Software

- 6.3.1 In-vehicle software

- 6.3.2 Mobile app based

Chapter 7 Market Estimates & Forecast, By Alert, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Visual Alert Systems

- 7.3 Audio Alert Systems

- 7.4 Tactile Alert Systems

- 7.5 Multi-Modal Alert Systems

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 LCV

- 8.3.2 MCV

- 8.3.3 HCV

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Russia

- 10.3.8 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Vietnam

- 10.4.9 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Robert Bosch

- 11.1.2 Continental

- 11.1.3 DENSO

- 11.1.4 ZF

- 11.1.5 Aptiv

- 11.1.6 Magna

- 11.1.7 Autoliv

- 11.1.8 Mobileye

- 11.1.9 Valeo

- 11.1.10 Hyundai Mobis

- 11.2 Regional players

- 11.2.1 Smart Eye

- 11.2.2 Seeing Machines

- 11.2.3 Ficosa

- 11.2.4 Visteon

- 11.2.5 Harman

- 11.2.6 Faurecia

- 11.3 Emerging players

- 11.3.1 Jungo Connectivity

- 11.3.2 Affectiva

- 11.3.3 Xperi/Perceive

- 11.3.4 Neonode

汽車後側路口交通警報系統市場-2026-2032年全球市場預測駕駛預警系統市場:2026-2032年全球市場預測(依系統類型、技術、監控類型、自動化程度、應用和車輛類型分類)

汽車後側路口交通警報系統市場-2026-2032年全球市場預測駕駛預警系統市場:2026-2032年全球市場預測(依系統類型、技術、監控類型、自動化程度、應用和車輛類型分類) 駕駛預警系統市場:依系統、解決方案、預警類型、車輛類型、驅動系統、銷售管道、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

駕駛預警系統市場:依系統、解決方案、預警類型、車輛類型、驅動系統、銷售管道、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 駕駛警告系統市場分析與預測(至2035年):依類型、產品、技術、應用、最終使用者、功能及安裝方式分類

駕駛警告系統市場分析與預測(至2035年):依類型、產品、技術、應用、最終使用者、功能及安裝方式分類 智慧車道警報系統市場預測—全球分析(按組件、偵測方法、偵測範圍、技術、應用和地區分類)—2034年

智慧車道警報系統市場預測—全球分析(按組件、偵測方法、偵測範圍、技術、應用和地區分類)—2034年 2026年全球弱勢道路使用者(VRU)指標市場報告2026年全球酒駕預防設備市場報告2026年全球駕駛警示系統市場報告聲電式車輛警報系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶及功能分類

2026年全球弱勢道路使用者(VRU)指標市場報告2026年全球酒駕預防設備市場報告2026年全球駕駛警示系統市場報告聲電式車輛警報系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶及功能分類 2026-2030年全球汽車後方交叉路口警示(RCTA)市場

2026-2030年全球汽車後方交叉路口警示(RCTA)市場