|

市場調查報告書

商品編碼

1998776

番茄加工市場機會、成長要素、產業趨勢分析及2026-2035年預測Tomato Processing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

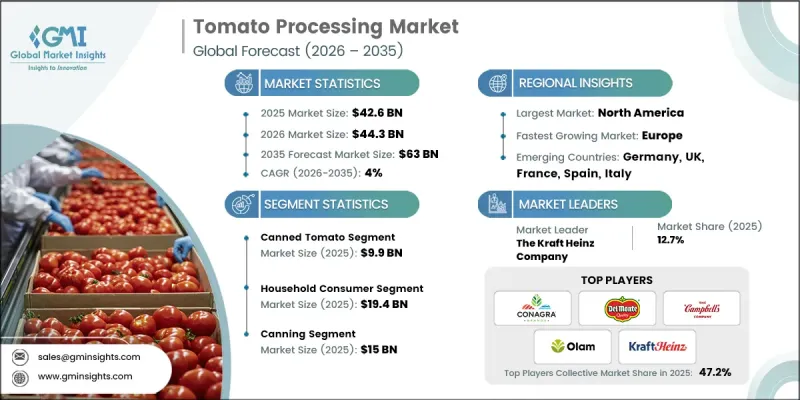

預計到 2025 年,全球番茄加工市場價值將達到 426 億美元,並預計以 4% 的複合年成長率成長,到 2035 年達到 630 億美元。

市場成長的驅動力在於消費者對番茄加工產品(如番茄醬、番茄膏、番茄汁、番茄沙司和罐頭番茄)的需求不斷成長。這些產品的生產過程包括分類、清洗、去皮、製漿、濃縮和包裝。這些加工過程能夠延長保存期限、維持營養價值、確保食品安全、減少採後損失,並實現全年供應。番茄加工將易腐的新鮮番茄轉化為商業性價值且方便的產品。該行業涵蓋各種規模的加工設施,從採用機械、熱力和化學加工技術的小規模工廠到大規模自動化工廠。在番茄過剩的地區,加工在應對季節性波動、減少廢棄物和持續滿足消費者需求方面發揮著至關重要的作用。此外,健康意識的增強、都市化的推進以及零售和電子商務網路的擴張進一步推動了該行業的發展,使番茄加工產品成為全球食品行業的重要組成部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 426億美元 |

| 預測金額 | 630億美元 |

| 複合年成長率 | 4% |

由於罐頭食品保存期限長、能維持產品安全,且方便消費者和零售商,預計到2025年,罐頭食品市場規模將達到150億美元。除了罐裝之外,其他加工方法,例如醬料和果汁的生產、濃縮、乾燥、冷凍和發酵,可以滿足各種產品類型和消費者偏好。隨著家庭和餐飲服務業對即食、易烹飪食材的需求不斷成長,醬料和調味醬的生產也持續擴大。果汁萃取越來越受到注重健康的消費者的歡迎,他們重視飲食中的營養成分保留、天然風味和功能性益處。

預計到2025年,家庭消費市場規模將達到194億美元,這主要得益於消費者健康飲食意識的增強以及對便捷即食產品的偏好。家庭消費者需要能夠簡化烹飪流程、同時又能確保品質、營養和口味穩定的番茄製品。除了家庭消費外,食品加工商、餐廳和飲料業也是該市場的主要驅動力。這些產業依賴加工番茄製品,因為其原料品質穩定、生產擴充性且供應鏈可靠,能夠高效滿足客戶需求。

預計2025年,美國番茄加工市場規模將達到1,16億美元,主要得益於消費者對便利、健康、高品質番茄產品的強勁需求。人們生活方式的轉變,更加重視快速便捷的烹飪方式,同時又不犧牲營養,這推動了番茄醬、番茄膏和番茄汁等食品的家庭消費量激增。現代化的零售基礎設施、高效的電商平台和先進的配送網路,確保了加工番茄產品從都市區到鄉村的順暢流通。對加工和包裝效率的投資,保證了產品品質和穩定性;而低溫運輸和延長保存期限的創新,則進一步增強了供應的穩定性。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球對加工番茄製品的需求不斷成長

- 提高效率和品質的技術進步

- 零售、餐飲服務和分銷管道的擴張

- 產業潛在風險與挑戰

- 新鮮番茄的價格波動和供應波動

- 市場競爭激烈,品牌飽和

- 市場機遇

- 健康意識的增強和對有機產品的需求增加

- 透過產品專屬應用程式創造額外收入來源。

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 番茄醬

- 番茄食物泥

- 罐裝番茄

- 番茄醬

- 番茄醬

- 番茄汁/濃縮番茄

- 乾番茄粉

- 其他

第6章 市場估算與預測:依加工方式分類,2022-2035年

- 罐頭

- 醬料生產

- 果汁萃取

- 集中

- 乾燥

- 冰凍

- 發酵

- 其他

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 普通家庭

- 食品加工機

- 餐飲服務業

- 飲料業

第8章 市場估算與預測:依通路分類,2022-2035年

- 大賣場和超級市場

- 特色食品店

- 便利商店

- 線上/電子商務

- 直銷

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Campbell Soup Company

- ConAgra Brands, Inc.

- Dabur

- Del Monte Foods, Inc.

- Erregi srl

- General Mills, Inc.

- Mutti SpA

- Neil Jones Food Company

- Olam International

- Pacific Coast Producers

- The Kraft Heinz Company

The Global Tomato Processing Market was valued at USD 42.6 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 63 billion by 2035.

The market is driven by the rising demand for processed tomato products such as sauces, pastes, juices, ketchup, and canned tomatoes, which are produced through operations like sorting, washing, peeling, pulping, concentrating, and packaging. These processes extend shelf life, preserve nutritional value, and ensure food safety, while reducing post-harvest losses and providing year-round availability. Tomato processing enables the transformation of perishable raw tomatoes into commercially viable, convenient products. The industry encompasses a mix of small-scale facilities and large automated plants that employ mechanical, thermal, and chemical processing techniques. In regions with surplus tomato production, processing plays a critical role in managing seasonal fluctuations, minimizing waste, and meeting consumer demand consistently. The industry is further reinforced by growing health awareness, urbanization, and the expansion of retail and e-commerce networks, making processed tomato products an essential component of the global food sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $42.6 Billion |

| Forecast Value | $63 Billion |

| CAGR | 4% |

The canning segment generated USD 15 billion in 2025, owing to its ability to provide long shelf life, maintain product safety, and offer convenience for consumers and retailers alike. Alongside canning, other processing methods, such as sauce and juice production, concentration, drying, freezing, and fermentation, cater to diverse product types and consumer preferences. Sauce and paste production continue to expand as demand rises for ready-to-use and easy-to-cook ingredients in households and foodservice channels. Juice extraction has gained traction with health-conscious consumers who prioritize nutrient retention, natural flavor, and functional benefits in their diets.

The household consumer segment reached USD 19.4 billion in 2025, driven by rising awareness about healthy diets and the increasing preference for ready-to-use, convenient products. Households are seeking tomato-based items that simplify meal preparation while delivering consistent quality, nutrition, and taste. Beyond households, industrial food processors, restaurants, and the beverage industry are substantial contributors to the market. These segments rely on processed tomato products for consistent ingredient quality, scalability in production, and reliable supply chains to meet customer demand efficiently.

U.S. Tomato Processing Market accounted for USD 11.6 billion in 2025, underpinned by strong consumer demand for convenient, healthy, and high-quality tomato products. Household consumption of sauces, pastes, and juices has surged due to evolving lifestyles that prioritize time-saving meal solutions without compromising nutrition. Modern retail infrastructure, efficient e-commerce platforms, and advanced distribution networks support the seamless delivery of processed tomato products across urban and rural areas. Investments in processing and packaging efficiency ensure product quality and consistency, while technological innovations in cold chain and shelf-life extension reinforce supply stability.

Prominent players in the Global Tomato Processing Market include Del Monte Foods, Inc., Campbell Soup Company, ConAgra Brands, Inc., Dabur, Erregi s.r.l., General Mills, Inc., Mutti S.p.A., Neil Jones Food Company, Mizkan Americas, Pacific Coast Producers, and Kraft Heinz Inc. Companies in the Global Tomato Processing Market are leveraging several strategies to strengthen market presence and expand their foothold. Key approaches include investment in advanced processing and packaging technologies to enhance product quality and shelf life, adoption of automated manufacturing systems to improve efficiency, and expansion into emerging markets to capture new consumer bases. Firms are also focusing on product diversification with health-oriented, organic, and convenient tomato-based offerings. Strategic partnerships with distributors, retailers, and e-commerce platforms enable wider market reach, while branding and marketing initiatives drive consumer loyalty. Sustainability practices, such as reducing post-harvest losses and eco-friendly packaging, are also being employed to enhance competitiveness and align with growing consumer and regulatory expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Processing Method

- 2.2.3 End Use

- 2.2.4 Distribution Channel

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global demand for processed tomato products

- 3.2.1.2 Technological advancements enhancing efficiency and quality

- 3.2.1.3 Expansion of retail, foodservice, and distribution channels

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Price volatility and supply fluctuations of raw tomatoes

- 3.2.2.2 Intense competition and brand saturation in market

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for health-oriented and organic products

- 3.2.3.2 Utilization of byproducts for additional revenue streams

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Tomato paste

- 5.3 Tomato puree

- 5.4 Canned tomatoes

- 5.5 Tomato sauces

- 5.6 Tomato ketchup

- 5.7 Tomato juice & concentrate

- 5.8 Dried tomatoes & powder

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Processing Method, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Canning

- 6.3 Sauce production

- 6.4 Juice extraction

- 6.5 Concentration

- 6.6 Drying

- 6.7 Freezing

- 6.8 Fermentation

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Household consumers

- 7.3 Industrial food processors

- 7.4 Restaurants & foodservice

- 7.5 Beverage industry

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Hypermarkets & supermarkets

- 8.3 Food Specialty Stores

- 8.4 Convenience Stores

- 8.5 Online/E-commerce

- 8.6 Direct Sales

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Campbell Soup Company

- 10.2 ConAgra Brands, Inc.

- 10.3 Dabur

- 10.4 Del Monte Foods, Inc.

- 10.5 Erregi s.r.l.

- 10.6 General Mills, Inc.

- 10.7 Mutti S.p.A.

- 10.8 Neil Jones Food Company

- 10.9 Olam International

- 10.10 Pacific Coast Producers

- 10.11 The Kraft Heinz Company