|

市場調查報告書

商品編碼

1998775

流感快速診斷測試市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Rapid Influenza Diagnostic Tests (RIDT) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

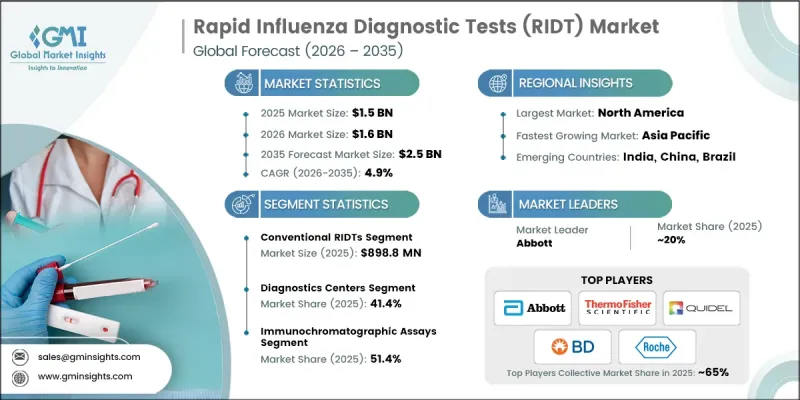

全球快速流感診斷測試 (RIDT) 市場預計到 2025 年將價值 15 億美元,預計到 2035 年將以 4.9% 的複合年成長率成長至 25 億美元。

快速流感診斷檢測有助於快速發現流感感染,使醫護人員能夠及早啟動治療和預防措施。快速診斷技術的廣泛應用、持續的技術進步以及對及時識別疾病的日益重視,都顯著推動了市場成長。診斷技術的改進提高了靈敏度和特異性,增強了這些檢測的可靠性,並提升了其在臨床實踐中的價值。從傳統的定性檢測轉向半定量診斷方法,也提高了臨床評估能力。此外,能夠同時識別流感和其他呼吸道感染疾病的多重診斷解決方案的開發,進一步提升了這些檢測在醫療機構中的整體效用診斷檢測的可近性,使更多患者能夠獲得這些檢測服務。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 15億美元 |

| 預計金額 | 25億美元 |

| 複合年成長率 | 4.9% |

許多地方公共衛生部門正在加強疾病監測和診斷能力,以更有效地應對流感的影響。多項全球健康舉措強調準確、早期檢測流感感染的重要性,以支持有效的疾病監測和應對。監管機構也正在加速快速流感診斷技術的應用,包括加快核准流程和支援先進診斷解決方案的推廣。

預計到2025年,傳統流感快速診斷檢測的市場規模將達到8.988億美元。由於其檢測速度比許多先進的分子檢測方法更快,因此該市場持續保持強勁勢頭。傳統檢測方法之所以被廣泛採用,是因為它們經濟實惠且易於醫護人員取得。其相對簡單的生產流程和較低的基礎設施要求使其適用於各種醫療環境。此外,其價格優勢也支持了醫療預算有限地區的公共衛生篩檢計畫。傳統流感快速診斷檢測也因其易用性而備受青睞,無需接受過專業技術培訓即可進行操作。快速出結果的能力使醫護人員能夠及時做出臨床決策,這在流感爆發期間尤其重要。

預計到2025年,層析法法將佔據51.4%的市場。這些診斷方法因其卓越的分析性能(包括高靈敏度和特異性)而被廣泛接受。它們能夠檢測到相對較低的病毒濃度,從而在疾病早期階段準確地識別感染。早期檢測對於可能面臨併發症併發症高風險的人尤其重要。此外,由於其結構緊湊、設備要求低,層析法在分散式醫療環境中的應用日益廣泛。其便攜性和易操作性使其成為即使在檢查室基礎設施有限的環境中也實用的診斷工具。技術進步正在進一步提高這些檢測的速度和可靠性,使其在尋求高效可靠的流感檢測解決方案的醫療專業人員中更受歡迎。

美國快速流感診斷測試(RIDT)市場預計到2025年將達到4.793億美元,成為北美最大的市場。健全的醫療保健體系、民眾對流感預防和診斷的廣泛認知以及對診斷技術的巨額投資,持續推動著美國市場的成長。隨著流感檢測服務在多個醫療網路基地台的普及,患者尋求快速診斷的便利性得到了提升。此外,旨在加強流感疫情應對策略的國家級準備工作,也加速了快速診斷檢測技術的廣泛應用。成熟的診斷設備製造商的存在以及醫療網路檢測能力的持續提升,也為市場發展提供了支持。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策及對資料完整性的承諾

- 資訊來源一致性通訊協定

- GMI人工智慧政策及對資料完整性的承諾

- 調查過程和可靠性評分

- 研究路徑的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 流感疫情蔓延

- 技術進步

- 對流感早期診斷和治療的需求日益成長

- 快速診斷測試日益普及

- 產業潛在風險與挑戰

- 熟練專業人員短缺

- 嚴格的監管核准

- 機會

- 人工智慧增強型解讀工具,提升準確性

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 歐洲

- 亞太地區

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術(基於初步調查)

- 未來市場趨勢(基於初步研究)

- 消費行為分析

- 價值鏈分析

- 產品特定定價分析(2025 年)(基於初步調查)

- 人工智慧和生成式人工智慧對市場的影響(基於初步研究)

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 差距分析

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 常規RIDT

- 數字RIDT

第6章 市場估計與預測:依技術分類,2022-2035年

- 層析法

- 橫向流動化驗

- 聚合酵素鏈鎖反應

- 其他技術

第7章 市場估計與預測:依檢體類型分類,2022-2035年

- 鼻拭子

- 咽拭子

- 其他檢體

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 診斷中心

- 醫院

- 研究所

- 其他最終用戶

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 3B BlackBio

- Abbott

- Access Bio

- Becton, Dickinson and Company(BD)

- bioMerieux

- CHEMBIO

- DiaSorin

- Meridian

- Quidel Corporation

- Roche

- SEKISUI

- Siemens Healthineers

- Thermo Fisher Scientific

The Global Rapid Influenza Diagnostic Tests (RIDT) Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 2.5 billion by 2035.

Rapid influenza diagnostic tests help in the quick detection of influenza infections, enabling healthcare professionals to initiate treatment and preventive measures at an early stage. Growing acceptance of rapid diagnostic technologies, continuous technological progress, and increasing emphasis on timely disease identification are contributing significantly to market growth. Improvements in diagnostic technologies have strengthened the reliability of these tests by enhancing sensitivity and specificity, making them increasingly valuable in clinical practice. The transition from traditional qualitative testing toward semi-quantitative diagnostic approaches is also improving clinical assessment capabilities. Furthermore, the development of multiplex diagnostic solutions capable of identifying influenza alongside other respiratory infections has enhanced the overall usefulness of these tests in healthcare settings. Emerging digital technologies, including artificial intelligence and machine learning, are further supporting this evolution by enabling automated result interpretation and minimizing the risk of human error. At the same time, rising investments in healthcare infrastructure are improving the availability and accessibility of rapid influenza diagnostic tests for a larger patient population.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 4.9% |

Public health authorities across multiple regions are strengthening disease monitoring and diagnostic capabilities to manage the impact of influenza more effectively. Several global health initiatives emphasize the importance of accurate and early detection of influenza infections to support effective disease surveillance and response efforts. Regulatory organizations are also encouraging the adoption of rapid influenza diagnostic technologies by accelerating approval pathways and supporting the availability of advanced diagnostic solutions.

The conventional rapid influenza diagnostic tests segment generated USD 898.8 million in 2025. This segment continues to maintain a strong presence due to its ability to deliver results more quickly than many advanced molecular testing approaches. Conventional tests remain widely adopted because they are cost-effective and easily accessible for healthcare providers. Their relatively simple manufacturing process and minimal infrastructure requirements make them suitable for a broad range of healthcare environments. In addition, the affordability of these tests supports public health screening programs in regions where healthcare budgets are limited. Conventional rapid influenza diagnostic tests are also valued for their ease of use, as they can be administered without extensive technical training. Their ability to produce results within a short time frame allows healthcare professionals to make timely clinical decisions, which is particularly important during periods of increased influenza transmission.

The immunochromatographic assays segment held a 51.4% share in 2025. These diagnostic methods have gained considerable acceptance because of their strong analytical performance, including high levels of sensitivity and specificity. Their capability to detect relatively small viral concentrations supports accurate identification of infections during the early stages of illness. Early detection is particularly important for individuals who may face higher risks of complications from influenza infections. Immunochromatographic assays are also increasingly utilized in decentralized healthcare environments due to their compact design and minimal equipment requirements. Their portability and operational simplicity make them practical diagnostic tools in settings where laboratory infrastructure may be limited. Technological improvements have further enhanced the speed and reliability of these assays, which have contributed to growing preference among healthcare professionals seeking efficient and dependable influenza testing solutions.

United States Rapid Influenza Diagnostic Tests (RIDT) Market reached USD 479.3 million in 2025, positioning the country as the largest contributor within the North American region. Strong healthcare frameworks, widespread awareness of influenza prevention and diagnosis, and substantial investment in diagnostic technologies continue to support market expansion in the country. The growing availability of influenza testing services across multiple healthcare access points has improved convenience for patients seeking a timely diagnosis. Additionally, national preparedness initiatives aimed at strengthening response strategies for influenza outbreaks have encouraged broader adoption of rapid diagnostic testing technologies. The presence of established diagnostic manufacturers and the continued expansion of testing capabilities across healthcare networks are also supporting market development.

Key companies participating in the Global Rapid Influenza Diagnostic Tests (RIDT) Market include Abbott, Siemens Healthineers, Roche, Quidel Corporation, Thermo Fisher Scientific, bioMerieux, Becton, Dickinson and Company (BD), DiaSorin, Meridian, Access Bio, CHEMBIO, 3B BlackBio, and SEKISUI. Companies operating in the Rapid Influenza Diagnostic Tests (RIDT) Market are adopting a range of strategies to strengthen their competitive position and expand their market presence. A major focus remains on research and development activities aimed at improving test sensitivity, accuracy, and speed. Many manufacturers are investing in advanced diagnostic technologies such as digital testing platforms and multiplex detection systems to enhance clinical value. Strategic collaborations with healthcare providers and diagnostic laboratories are helping companies broaden product adoption and improve distribution networks. In addition, organizations are expanding manufacturing capacity and strengthening supply chains to meet increasing global demand for rapid testing solutions. Companies are also emphasizing regulatory approvals and quality certifications to support product credibility and market entry.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Technology trends

- 2.2.4 Sample type trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of influenza

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising demand for early influenza diagnosis and management

- 3.2.1.4 Increasing popularity of rapid diagnostic tests

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals

- 3.2.2.2 Stringent regulatory approvals

- 3.2.3 Opportunities

- 3.2.3.1 AI-enhanced interpretation tools for better accuracy

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by primary research)

- 3.6 Future market trends (Driven by primary research)

- 3.7 Consumer behavior analysis

- 3.8 Value chain analysis

- 3.9 Pricing analysis, by products, 2025 (Driven by primary research)

- 3.10 Impact of AI & generative AI on the market (Driven by primary research)

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Gap analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Conventional RIDTs

- 5.3 Digital RIDTs

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Immunochromatographic assays

- 6.3 Lateral flow assays

- 6.4 Polymerase Chain Reaction

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Sample Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Nasal Swab

- 7.3 Throat Swab

- 7.4 Other samples

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Diagnostics centers

- 8.3 Hospitals

- 8.4 Research laboratories

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3B BlackBio

- 10.2 Abbott

- 10.3 Access Bio

- 10.4 Becton, Dickinson and Company (BD)

- 10.5 bioMerieux

- 10.6 CHEMBIO

- 10.7 DiaSorin

- 10.8 Meridian

- 10.9 Quidel Corporation

- 10.10 Roche

- 10.11 SEKISUI

- 10.12 Siemens Healthineers

- 10.13 Thermo Fisher Scientific

全球流感診斷市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球流感診斷市場規模、佔有率、趨勢和成長分析報告(2026-2034) 流感診斷市場-全球產業規模、佔有率、趨勢、機會、預測:按檢測類型、最終用戶、地區和競爭格局分類,2021-2031年

流感診斷市場-全球產業規模、佔有率、趨勢、機會、預測:按檢測類型、最終用戶、地區和競爭格局分類,2021-2031年 日本流感診斷市場報告(按產品、檢測類型、流感類型、最終用戶和地區分類,2026-2034年)

日本流感診斷市場報告(按產品、檢測類型、流感類型、最終用戶和地區分類,2026-2034年) 流感診斷市場規模、佔有率和成長分析(按產品、檢測方法、最終用戶和地區分類)—產業預測(2026-2033 年)

流感診斷市場規模、佔有率和成長分析(按產品、檢測方法、最終用戶和地區分類)—產業預測(2026-2033 年) 2025年流感診斷全球市場報告

2025年流感診斷全球市場報告 流感診斷全球市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

流感診斷全球市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年) 快速流感診斷檢測市場,按類型、按產品類型、按最終用途、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測全球流感診斷市場規模(按產品、最終用戶、測試類型、地區、範圍和預測)

快速流感診斷檢測市場,按類型、按產品類型、按最終用途、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測全球流感診斷市場規模(按產品、最終用戶、測試類型、地區、範圍和預測) 2024-2028年全球流感診斷市場

2024-2028年全球流感診斷市場