|

市場調查報告書

商品編碼

1998774

肽類抗生素市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測。Peptide Antibiotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

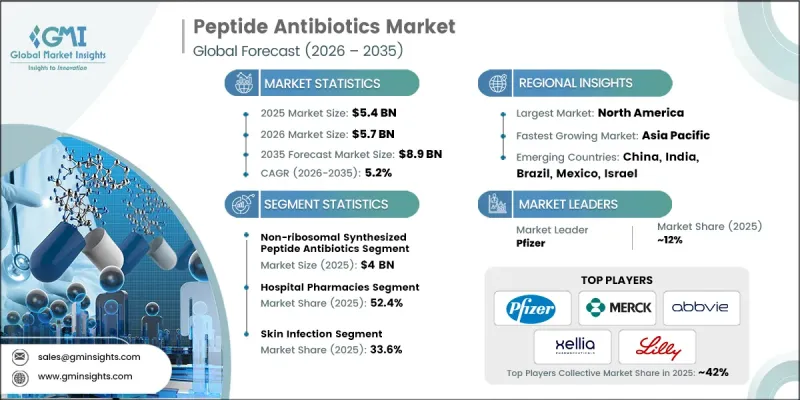

全球胜肽類抗生素市場預計到 2025 年將價值 54 億美元,並將以 5.2% 的複合年成長率成長,到 2035 年將達到 89 億美元。

肽類抗生素產業的整體成長主要受抗藥性問題日益嚴峻以及對抗抗藥性感染疾病的新治療方法迫切需求的推動。公共和私人機構的資金投入在加速該領域的創新中發揮著至關重要的作用。旨在發現先進抗菌解決方案的投資項目正在推動新型肽類治療方法的研發。同時,胜肽合成技術和尖端藥物遞送平台的快速發展也拓展了胜肽類抗生素的開發平臺。這些進步使研究人員能夠設計出更有效的抗菌藥物,以應對不斷湧現的抗藥性挑戰。隨著醫療專業人員對能夠帶來切實療效的標靶治療的需求持續成長,肽類抗生素在藥物研發和臨床治療項目中日益受到關注,從而增強了肽類抗生素市場的長期成長前景。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 54億美元 |

| 預計金額 | 89億美元 |

| 複合年成長率 | 5.2% |

生物工程和製劑技術的進步顯著提高了胜肽類抗生素的穩定性、生物利用度和治療效果,從而大幅增強了其療效。標靶治療的日益普及也推動了胜肽類抗菌療法的發展,因為這些化合物可以被設計成攻擊抗藥性菌株,同時最大限度地減少不良的全身反應。肽類抗生素,通常被稱為抗菌肽,由能夠抑制微生物生存過程的短鏈氨基酸組成。這些分子透過干擾重要的細胞機制和結構成分來抑制微生物的生長。這類胜肽可以天然存在於生物系統中,也可以透過實驗室合成技術合成。

預計2025年,非核醣體合成胜肽類抗生素市場規模將達40億美元。該細分市場憑藉其廣譜抗菌活性和強大的抗酶分解能力,保持著主導地位。非核醣體合成胜肽類抗生素透過特殊的酵素複合物生產,從而實現高度的結構多樣性,並可引入通常不使用的胺基酸成分。這種結構柔軟性增強了這些抗生素的治療效果和持久性,使其在治療多重抗藥性菌株引起的感染疾病特別有效。

預計到2025年,皮膚感染疾病領域將佔據33.6%的市場。肽類抗生素在該領域的強勁表現與細菌性皮膚病發病率的上升以及對有效治療方法日益成長的需求密切相關。此外,難癒合傷口和醫療手術後感染疾病相關併發症的發生率不斷上升,也促進了對肽類抗生素的需求成長。這些藥物之所以被選中,是因為它們具有靶向抗菌活性,同時也能降低全身性副作用的風險。

預計到2025年,北美肽類抗生素市佔率將達到40.5%。該地區在全球肽類抗生素行業的主導地位得益於其先進的藥物研發能力、嚴格的法律規範以及雄厚的醫療保健支出。成熟的生物技術和製藥產業進一步推動了抗生素研發的創新。此外,政府支持的研究資助計畫和旨在促進新型抗菌療法發現的政策舉措,也有助於加速全部區域的研發和商業化。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 多重抗藥性(MDR))細菌)的傳播

- 急性和慢性感染疾病發生率增加

- 肽合成技術步驟

- 增加對下一代抗菌劑研發的投入

- 產業潛在風險與挑戰

- 高昂的製造成本

- 口服生物有效性度低

- 市場機遇

- 利用胜肽工程擴展藥物遞送系統

- 為預防抗菌藥物抗藥性,對新型抗菌藥物的需求日益成長。

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 管道分析

- 未來市場趨勢(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 核醣體合成的胜肽類抗生素

- 非核醣體合成胜肽類抗生素

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 皮膚感染疾病

- 本院獲得性細菌性肺炎和人工呼吸器相關性細菌性肺炎(HABP/VABP)

- 血液感染疾病

- 其他跡象

第7章 市場估計與預測:依給藥途徑分類,2022-2035年

- 注射藥物

- 口服

- 外用

- 其他給藥途徑

第8章 市場估算與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AbbVie

- ANI Pharmaceuticals

- Cumberland Pharmaceuticals

- Eli Lilly and Company

- GSK plc

- JHP Pharmaceuticals

- Merck

- Monarch Pharmachem

- Melinta Therapeutics

- NPS Pharmaceuticals

- Pfizer

- Sanofi

- Sandoz

- Teva Pharmaceuticals

- The Menarini Group

- Xellia Pharmaceutical

The Global Peptide Antibiotics Market generated USD 5.4 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 8.9 billion by 2035.

Growth across the peptide antibiotic industry is strongly influenced by increasing concerns regarding antimicrobial resistance and the urgent need for new treatment approaches capable of combating drug-resistant infections. Financial support from public institutions as well as independent organizations is playing a significant role in accelerating innovation within this field. Investment programs aimed at discovering advanced antimicrobial solutions are encouraging the development of new peptide-based therapeutic options. At the same time, rapid progress in peptide synthesis technologies and modern drug delivery platforms is expanding the development pipeline for peptide antibiotics. These advancements are enabling researchers to design more effective antimicrobial agents that can address emerging resistance challenges. As healthcare providers continue seeking targeted therapies capable of delivering reliable outcomes, peptide antibiotics are gaining greater attention within pharmaceutical research and clinical treatment programs, strengthening the long-term growth outlook for the peptide antibiotics market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.4 Billion |

| Forecast Value | $8.9 Billion |

| CAGR | 5.2% |

Technological progress in bioengineering and pharmaceutical formulation has significantly enhanced the therapeutic performance of peptide antibiotics by improving their stability, bioavailability, and treatment efficiency. The increasing focus on targeted medical treatments is also encouraging the development of peptide-based antimicrobial therapies, as these compounds can be engineered to attack resistant microbial strains while minimizing unwanted systemic effects. Peptide antibiotics, commonly referred to as antimicrobial peptides, consist of short chains of amino acids capable of disrupting microbial survival processes. These molecules inhibit microbial growth by interfering with essential cellular mechanisms and structural components. Such peptides may originate naturally within biological systems or be produced synthetically through laboratory-based development methods.

The non-ribosomal synthesized peptide antibiotics segment generated USD 4 billion in 2025. This segment maintains a leading position because of its broad antimicrobial activity and strong resistance to enzymatic degradation. Non-ribosomal peptide antibiotics are generated through specialized enzyme complexes that allow extensive structural diversity and the incorporation of uncommon amino acid components. This structural flexibility improves the therapeutic strength and durability of these antibiotics, making them particularly valuable for addressing infections caused by multidrug-resistant bacterial strains.

The skin infection segment held 33.6% share in 2025. The segment's strong presence within the peptide antibiotics industry is associated with the growing occurrence of bacterial skin-related conditions and the rising need for effective therapeutic solutions. The increasing incidence of persistent wounds and infection-related complications following medical procedures has also contributed to higher demand for peptide-based antibiotics. These medications are often selected because they provide targeted antimicrobial activity while reducing the likelihood of broader systemic side effects.

North America Peptide Antibiotics Market accounted for 40.5% share in 2025. The region's leadership within the global peptide antibiotics industry is supported by advanced pharmaceutical research capabilities, strong regulatory oversight, and significant healthcare spending. A well-established biotechnology and pharmaceutical sector further encourages innovation in antibiotic drug development. In addition, government-backed research funding programs and policy initiatives designed to promote the discovery of new antimicrobial therapies are helping accelerate development and commercialization activities across the region.

Key companies operating in the Global Peptide Antibiotics Market include Pfizer, Merck, Sanofi, GSK plc, Eli Lilly and Company, AbbVie, Teva Pharmaceuticals, Sandoz, The Menarini Group, ANI Pharmaceuticals, Cumberland Pharmaceuticals, Melinta Therapeutics, Monarch Pharmachem, JHP Pharmaceuticals, NPS Pharmaceuticals, and Xellia Pharmaceuticals. Companies in the Global Peptide Antibiotics Market are adopting several strategic approaches to strengthen their market position and support long-term growth. Major pharmaceutical manufacturers are prioritizing investment in research and development to create advanced antimicrobial compounds capable of addressing drug-resistant infections. Strategic collaborations with biotechnology firms, academic institutions, and research organizations are also helping accelerate drug discovery and clinical development programs. Many companies are expanding their product pipelines by focusing on innovative peptide synthesis technologies and advanced drug delivery systems. In addition, organizations are pursuing regulatory approvals across multiple regions to broaden global market access.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Route of administration trends

- 2.2.4 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of multi-drug resistant (MDR) bacteria

- 3.2.1.2 Increasing incidence of acute and chronic infectious diseases

- 3.2.1.3 Technological advancements in peptide synthesis

- 3.2.1.4 Rising investments in next-generation antimicrobial R&D

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Limited oral bioavailability

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of peptide-engineered drug delivery systems

- 3.2.3.2 Growing demand for novel antimicrobial classes for AMR prevention

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.5 Pipeline analysis

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Impact of AI and generative AI on the market

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Ribosomal synthesized peptide antibiotics

- 5.3 Non-ribosomal synthesized peptide antibiotics

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Skin infection

- 6.3 Hospital-acquired bacterial pneumonia and ventilator-associated bacterial pneumonia (HABP/VABP)

- 6.4 Blood stream infections

- 6.5 Other indications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Injectable

- 7.3 Oral

- 7.4 Topical

- 7.5 Other routes of administration

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 ANI Pharmaceuticals

- 10.3 Cumberland Pharmaceuticals

- 10.4 Eli Lilly and Company

- 10.5 GSK plc

- 10.6 JHP Pharmaceuticals

- 10.7 Merck

- 10.8 Monarch Pharmachem

- 10.9 Melinta Therapeutics

- 10.10 NPS Pharmaceuticals

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Sandoz

- 10.14 Teva Pharmaceuticals

- 10.15 The Menarini Group

- 10.16 Xellia Pharmaceutical