|

市場調查報告書

商品編碼

1998767

健康體檢市場機會、成長要素、產業趨勢分析及2026-2035年預測。Health Check-up Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

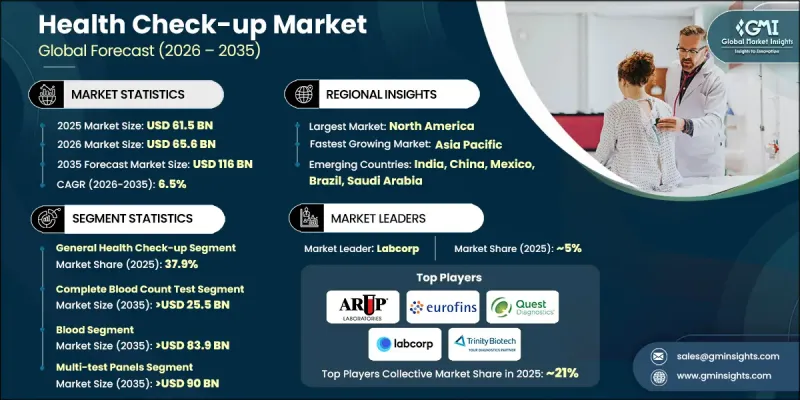

2025年全球健康體檢市場價值為615億美元,預計2035年將以6.5%的複合年成長率成長至1,160億美元。

健康篩檢市場的成長主要受以下因素驅動:國家健康篩檢投入的增加、慢性病盛行率的上升以及公眾對早期疾病檢測重要性的認知不斷提高。健康篩檢是由訓練有素的醫療專業人員進行的全面醫學評估,旨在了解個人的整體健康狀況。這些檢查旨在識別潛在的健康風險、發現疾病的早期徵兆,並提供預防保健建議。在許多地區,政府和醫療機構正日益推行相關政策,透過定期健康篩檢來推廣預防保健服務。這些措施旨在透過促進早期診斷和及時治療,減輕晚期疾病帶來的長期經濟負擔。此外,許多機構正在將健康篩檢服務納入員工健康計劃,以支持員工的健康和生產力。這些計劃建議定期進行健康篩檢,以便及早發現健康風險並支持長期健康維護。所有這些因素共同推動了全球健康篩檢市場的擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 615億美元 |

| 預測金額 | 1160億美元 |

| 複合年成長率 | 6.5% |

預計2025年,定期體檢及健康體檢市場規模將達183億美元,2035年將達331億美元。人們對生活方式相關健康風險的認知不斷提高,推動了定期體檢的普及,旨在監測整體健康狀況並及早發現潛在的健康問題。此外,經濟實惠的健康套餐日益普及、數位化預約平台蓬勃發展以及個人化預防保健項目的日益流行,都將推動該市場在預測期內持續成長。

血液常規檢查市場預計將以6.1%的複合年成長率成長,到2035年達到255億美元。這項診斷測試透過分析各種血球及其濃度,在評估個體健康狀況方面發揮著至關重要的作用。醫療專業人員依靠這項測試來評估生理健康的各個方面,包括有助於識別營養失衡和其他潛在健康問題的指標。此外,血球水平的波動能夠提供有價值的訊息,幫助醫療專業人員識別潛在的感染疾病和發炎反應,從而實現及時的臨床評估和適當的醫療管理。

美國健康體檢市場預計到2025年將達到202億美元,並在2026年至2035年間以5.6%的複合年成長率成長。人們對預防性健康管理的日益重視,持續推動著美國各地對預防性醫療保健服務的需求。慢性病發病率的上升,促使患者和醫療保健專業人員更加重視定期健康體檢,以支持早期發現和持續的健康監測。此外,人口結構變化和人口老化也增加了對更頻繁、更全面的健康體檢的需求。診斷設備的科技進步也提高了健康體檢的準確性和效率,使篩檢測試更加普及,並鼓勵更多人參與定期健康體檢。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 對大規模健康篩檢的投資正在激增。

- 疾病盛行率上升

- 人們對預防性醫療保健的認知不斷提高

- 數位科技、遠端醫療和居家照護服務的廣泛應用。

- 產業潛在風險與挑戰

- 篩檢成本高昂

- 發展中地區意識水平低且基礎設施不足

- 市場機遇

- 人工智慧驅動的診斷工具和數位健康平台

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 歐洲

- 亞太地區

- 技術趨勢(基於初步調查)

- 當前技術趨勢

- 新興技術

- 救贖方案

- 差距分析(基於初步調查)

- 波特五力分析

- PESTEL 分析

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 價值鏈分析

- 健康體檢套餐概述(基於初步調查)

- Start-Ups場景

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- LAMEA

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品類型發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 一般健康檢查

- 定期健康檢查

- 專業健康檢查

- 預防性健康檢查

第6章 市場估計與預測:依測試類型分類,2022-2035年

- 血液常規檢查

- 血糖測試

- 電解質測試

- 血脂譜檢測

- 荷爾蒙和維生素

- 腫瘤標記

- 肝功能檢查

- 心臟生物標記

- 腎功能檢查

- 骨輪廓檢查

- 其他類型的測試

第7章 市場估計與預測:依檢體類型分類,2022-2035年

- 血

- 尿

- 唾液

- 其他檢體類型

第8章 市場估算與預測:依面板類型分類,2022-2035年

- 多重測試面板

- 單檢修面板

第9章 市場估算與預測:依服務供應商,2022-2035年

- 醫院檢查室

- 獨立檢查室

- 門診部

- 中心檢查室

- 其他服務供應商

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- ARUP Laboratories

- Cerba Healthcare

- Eurofins

- Exact Sciences

- GRAIL

- INNOVA

- Labcorp

- Natera, Inc.

- OPKO

- Q2 Solutions

- Quest Diagnostics

- Sonic Healthcare

- SYNLAB

- Trinity Biotech

- UNILABS

The Global Health Check-up Market was valued at USD 61.5 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 116 billion by 2035.

Growth in the health check-up market is driven by rising investments in population health screening initiatives, increasing prevalence of chronic diseases, and greater public awareness regarding the importance of early disease detection. A health check-up refers to a comprehensive medical evaluation conducted by trained healthcare professionals to assess an individual's overall health status. These examinations are designed to identify potential health risks, detect early signs of medical conditions, and provide recommendations for preventive care. Governments and healthcare institutions across several regions are increasingly implementing policies that encourage preventive health services through regular medical examinations. Such initiatives aim to reduce the long-term economic burden associated with advanced-stage diseases by promoting early diagnosis and timely treatment. In addition, many organizations are integrating health screening services into employee wellness initiatives designed to support workforce health and improve productivity. These programs encourage regular medical assessments that help identify health risks early and support long-term wellbeing. Together, these factors are significantly contributing to the expansion of the global health check-up market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $61.5 Billion |

| Forecast Value | $116 Billion |

| CAGR | 6.5% |

The routine and wellness health check-up segment generated USD 18.3 billion in 2025 and is expected to reach USD 33.1 billion by 2035. Increasing awareness of lifestyle-related health risks is encouraging individuals to participate in regular medical screenings designed to monitor overall wellness and detect potential health concerns at an early stage. In addition, the growing availability of cost-effective wellness packages, the expansion of digital appointment scheduling platforms, and the rising popularity of personalized preventive health programs are supporting continued growth in this segment throughout the forecast period.

The complete blood count test segment is anticipated to grow at a CAGR of 6.1% and is projected to reach USD 25.5 billion by 2035. This diagnostic test plays an important role in evaluating an individual's health by analyzing different types of blood cells and their concentrations. Medical professionals rely on this test to assess various aspects of physiological health, including indicators that support the identification of nutritional imbalances and other underlying health conditions. In addition, variations in blood cell levels can provide valuable insights that assist healthcare providers in recognizing potential infections or inflammatory responses, enabling timely clinical evaluation and appropriate medical management.

United States Health Check-up Market was valued at USD 20.2 billion in 2025 and is projected to grow at a CAGR of 5.6% between 2026 and 2035. Increasing awareness regarding proactive health management continues to drive the demand for preventive healthcare services across the country. The rising incidence of chronic health conditions has encouraged both patients and healthcare professionals to prioritize regular medical assessments that support early detection and ongoing health monitoring. In addition, demographic changes and a growing elderly population are increasing the need for more frequent and comprehensive medical evaluations. Technological advancements in diagnostic equipment are also improving the accuracy and efficiency of health assessments, making screening procedures more accessible and encouraging broader participation in routine health examinations.

Major participants operating in the Global Health Check-up Market include Quest Diagnostics, Labcorp, Eurofins, Sonic Healthcare, SYNLAB, Cerba Healthcare, ARUP Laboratories, Exact Sciences, Natera, Inc., GRAIL, OPKO, Q2 Solutions, INNOVA, Trinity Biotech, and UNILABS. Companies operating in the Global Health Check-up Market are adopting a range of strategic initiatives to strengthen their market presence and expand service capabilities. Leading diagnostic service providers are investing in advanced laboratory technologies and digital healthcare platforms to improve the efficiency and accuracy of medical screening services. Many organizations are expanding preventive healthcare packages and personalized health assessment programs to address growing consumer demand for proactive health management. Strategic collaborations with hospitals, healthcare networks, and corporate organizations are helping companies broaden their customer base and enhance service accessibility. Additionally, firms are strengthening their laboratory infrastructure and geographic presence to support large-scale screening programs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key Market Trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Test type trends

- 2.2.4 Sample type trends

- 2.2.5 Panel type trends

- 2.2.6 Service provider trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging investments in population screening

- 3.2.1.2 Increasing prevalence of diseases

- 3.2.1.3 Rising awareness of preventive healthcare

- 3.2.1.4 Increasing adoption of digital technology/telemedicine & home-care services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with screening

- 3.2.2.2 Lack of awareness and proper infrastructure in underdeveloped regions

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven diagnostic tools and digital health platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Gap analysis (Driven by Primary Research)

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Impact of AI and generative AI on the market

- 3.12 Value chain analysis

- 3.13 Health check-up packages outline (Driven by primary research)

- 3.14 Start-up scenario

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key Developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 General health check-up

- 5.3 Routine and wellness health check-up

- 5.4 Specialized health check-up

- 5.5 Preventive health check-up

Chapter 6 Market Estimates and Forecast, By Test Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Complete blood count test

- 6.3 Blood glucose test

- 6.4 Electrolyte test

- 6.5 Lipid profile test

- 6.6 Hormones & vitamins

- 6.7 Tumor markers

- 6.8 Liver function test

- 6.9 Cardiac biomarkers

- 6.10 Kidney function test

- 6.11 Bone profile test

- 6.12 Other test types

Chapter 7 Market Estimates and Forecast, By Sample Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Blood

- 7.3 Urine

- 7.4 Saliva

- 7.5 Other sample types

Chapter 8 Market Estimates and Forecast, By Panel Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Multi-test panels

- 8.3 Single-test panels

Chapter 9 Market Estimates and Forecast, By Service Provider, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital-based laboratories

- 9.3 Standalone laboratories

- 9.4 Ambulatory care centers

- 9.5 Central laboratories

- 9.6 Other service providers

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ARUP Laboratories

- 11.2 Cerba Healthcare

- 11.3 Eurofins

- 11.4 Exact Sciences

- 11.5 GRAIL

- 11.6 INNOVA

- 11.7 Labcorp

- 11.8 Natera, Inc.

- 11.9 OPKO

- 11.10 Q2 Solutions

- 11.11 Quest Diagnostics

- 11.12 Sonic Healthcare

- 11.13 SYNLAB

- 11.14 Trinity Biotech

- 11.15 UNILABS