|

市場調查報告書

商品編碼

1998761

腸促胰素藥物市場商業機會、成長要素、產業趨勢分析及2026-2035年預測。Incretin-based Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

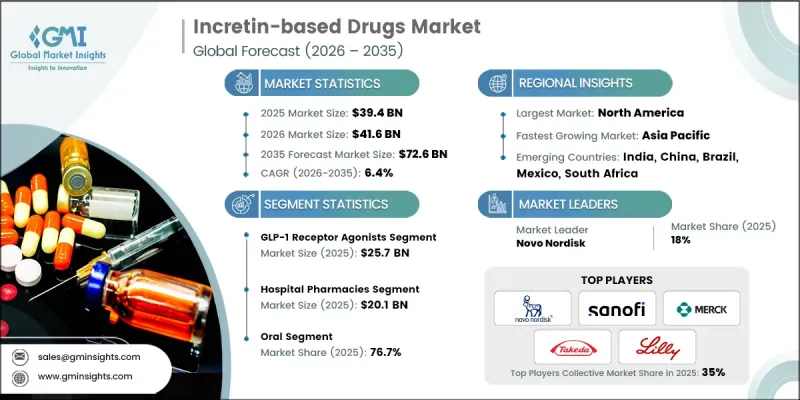

預計到 2025 年,全球腸促胰島素藥物市場價值將達到 394 億美元,並有望以 6.4% 的複合年成長率成長,到 2035 年達到 726 億美元。

腸促胰素類藥物市場的成長與全球第二型糖尿病發生率的加速上升密切相關,而第2型糖尿病的發生率持續推動著對有效長期治療方法的需求。醫療專業人員正逐漸轉向非胰島素療法,除了改善血糖控制外,還能促進更廣泛的心血管代謝健康。這類治療方法,包括GLP-1受體促效劑和DPP-4抑制劑,透過刺激胰島素分泌和抑制升糖素血糖值。此外,這些治療方法還有助於體重管理和改善心血管健康,因此在臨床實踐中的應用日益廣泛。藥物遞送技術的不斷進步,以及人們對先進糖尿病照護意識的不斷提高,進一步加速了已開發國家和新興國家醫療體系對腸促胰素類藥物的採納。隨著醫療專業人員致力於改善治療效果和長期疾病管理,腸促胰素類療法正擴大被納入糖尿病治療通訊協定。預計這種不斷變化的治療模式將在未來十年內維持對腸促胰素類藥物的強勁需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 394億美元 |

| 預計金額 | 726億美元 |

| 複合年成長率 | 6.4% |

腸促胰素類藥物市場也受益於臨床上對這些治療方法(尤其是GLP-1受體促效劑類藥物)相關心血管代謝益處的日益認可。除了血糖控制外,這些治療方法因其能夠支持第2型糖尿病患者更廣泛的心血管健康而備受重視。醫學研究表明,此類治療方法有助於降低高風險患者發生重大心血管併發症的風險,進一步提升了其在糖尿病治療策略中的重要性。其他益處,例如降低血壓、改善脂質代謝和抗發炎作用,也進一步強化了這些藥物在綜合心血管代謝管理中的作用。此外,體重管理仍然是製定治療策略的關鍵因素,因為超重仍然是糖尿病患者普遍關注的問題。

預計到2025年,GLP-1受體促效劑市場規模將達257億美元。由於其穩定的臨床療效以及在代謝性疾病管理中日益重要的地位,該細分市場持續保持較高的市場接受度。此類療法因其能有效控制血糖,同時也能促進心血管健康和體重管理等其他治療效果而廣受認可。製藥公司透過持續的產品研發拓展全球分銷策略,不斷提升GLP-1受體促效劑的市場佔有率。鑑於這些治療方法在慢性代謝性疾病管理中展現出可靠的療效,醫療專業人員正擴大將其納入常規治療方案。在糖尿病治療和體重相關代謝管理領域日益成長的認可度,進一步鞏固了該細分市場在腸促胰素類藥物行業的主導地位。

從給藥途徑來看,預計到2025年,口服給藥途徑將佔76.7%的市佔率。口服腸促胰素療法是注射藥物的便捷替代方案,在提高患者長期治療依從性方面發揮著至關重要的作用。口服製劑技術的進步有助於提高療效、安全性以及病人順從性。此外,這些藥物易於運輸、儲存和在醫療機構之間分發,因此適用於各種醫療環境。與注射藥物不同,口服療法無需患者接受專門的自我給藥培訓,這不僅減輕了醫護人員的負擔,也簡化了患者的治療流程。此外,許多患者傾向於選擇口服藥物,因為它們更方便、創傷更小。

預計到2025年,北美腸促胰素療法市場將佔據45.7%的佔有率。該地區持續展現出巨大的成長潛力,主要驅動力是第2型糖尿病患者數量的不斷增加。患者的成長推動了對先進治療方案的需求,這些方案旨在解決相關的代謝挑戰,同時實現持續的血糖控制。該地區的醫療專業人員正在增加腸促胰素療法的處方量,將其作為綜合糖尿病管理策略的一部分。這些治療方法不僅能夠有效控制長期血糖,還能帶來其他好處,例如體重管理,這對患有慢性代謝性疾病的患者至關重要。隨著醫療系統日益重視改善疾病的長期預後,腸促胰素療法正在北美各地的臨床醫生中得到廣泛認可。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 2型糖尿病盛行率增加

- 過渡到非胰島素療法

- 藥物傳輸技術的進步

- 對心血管系統和體重管理的益處

- 產業潛在風險與挑戰

- 高昂的醫療費用

- 副作用和禁忌症

- 市場機遇

- 病人意識的提高和肥胖管理文化的轉變

- 成長潛力分析

- 監理情勢(基於初步調查)

- 科技趨勢

- 當前技術趨勢

- 新興技術

- 未來市場趨勢(基於初步研究)

- 專利分析(基於初步研究)

- 價格分析(基於初步調查)

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略儀錶板

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依藥物類型分類,2022-2035年

- GLP-1受體促效劑

- DPP-4抑制劑

第6章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 注射藥物

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 2型糖尿病

- 肥胖和體重管理

- 其他代謝性疾病

第8章 市場估算與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 電子商務

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AstraZeneca

- Boehringer Ingelheim

- Eli Lilly and Company

- GlaxoSmithKline

- Merck

- Novo Nordisk

- Pfizer

- Sanofi

- Takeda Pharmaceutical Company

- Teva Pharmaceuticals

The Global Incretin-based Drugs Market was valued at USD 39.4 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 72.6 billion by 2035.

Growth in the incretin-based drugs industry is closely associated with the accelerating incidence of type 2 diabetes mellitus worldwide, which continues to increase demand for effective long-term treatment options. Medical professionals are progressively shifting toward non-insulin therapeutic approaches that offer improved glycemic control while supporting broader cardiometabolic health. Therapies in this category, including GLP-1 receptor agonists and DPP-4 inhibitors, help regulate blood glucose by stimulating insulin secretion and suppressing glucagon production. In addition, these treatments contribute to weight management and improved cardiovascular health, which has strengthened their clinical acceptance. Continuous improvements in drug delivery technologies, combined with rising awareness about advanced diabetes care, are further encouraging adoption across developed and emerging healthcare systems. As healthcare providers focus on improving treatment outcomes and long-term disease management, incretin-based therapies are increasingly being incorporated into diabetes treatment protocols. This evolving therapeutic landscape is expected to sustain strong demand for incretin-based medications over the coming decade.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $39.4 Billion |

| Forecast Value | $72.6 Billion |

| CAGR | 6.4% |

The incretin-based drugs market is also benefiting from growing clinical recognition of the cardiometabolic advantages associated with these therapies, particularly within the GLP-1 receptor agonists category. Beyond glucose regulation, these treatments are increasingly valued for their ability to support broader cardiovascular health in individuals living with type 2 diabetes. Medical studies have shown that therapies in this class can help lower the risk of major cardiovascular complications among high-risk patients, which has elevated their position in diabetes care strategies. Additional benefits such as reductions in blood pressure, improvements in lipid metabolism, and anti-inflammatory effects have further strengthened their role in comprehensive cardiometabolic management. Weight management has also become a significant factor influencing treatment decisions, as excess body weight remains a common concern among individuals with diabetes.

The GLP-1 receptor agonists segment generated USD 25.7 billion in 2025. This segment continues to experience strong adoption due to its consistent clinical performance and expanding relevance in metabolic disease management. Treatments within this category are widely recognized for delivering effective glucose control while supporting additional therapeutic outcomes related to cardiovascular health and body weight management. Pharmaceutical companies have strengthened the market presence of GLP-1 receptor agonists through continued product development and expanded global distribution strategies. As these therapies demonstrate reliable outcomes in managing chronic metabolic conditions, healthcare providers are increasingly integrating them into routine treatment plans. Their growing acceptance in both diabetes care and weight-related metabolic management continues to reinforce the segment's leadership within the incretin-based drugs industry.

Based on route of administration, the oral segment held a 76.7% share in 2025. Oral incretin therapies provide a convenient alternative to injectable formulations, which play an important role in improving patient adherence to long-term treatment. Advancements in oral drug formulation technologies have contributed to improved therapeutic performance, safety profiles, and patient compliance. These medications are also easier to transport, store, and distribute across healthcare facilities, making them suitable for diverse medical environments. Unlike injectable treatments, oral therapies do not require specialized training for self-administration, which helps reduce the burden on healthcare professionals while simplifying treatment routines for patients. In addition, many individuals prefer oral medications because they are more convenient and less invasive.

North America Incretin-based Drugs Market accounted for 45.7% share in 2025. The region continues to demonstrate significant growth potential, primarily due to the increasing number of individuals diagnosed with type 2 diabetes mellitus. The expanding patient population is driving demand for advanced therapeutic solutions capable of delivering sustained blood glucose management while addressing related metabolic challenges. Healthcare providers across the region are increasingly prescribing incretin-based therapies as part of comprehensive diabetes management strategies. These treatments offer effective long-term glycemic control and provide additional benefits such as weight management, which are highly relevant for patients dealing with chronic metabolic conditions. As the healthcare system focuses on improving long-term disease outcomes, incretin-based drugs are gaining broader acceptance among clinicians throughout North America.

Key participants operating in the Global Incretin-based Drugs Market include AstraZeneca, Boehringer Ingelheim, Eli Lilly and Company, Merck, Novo Nordisk, Pfizer, Sanofi, Takeda Pharmaceutical Company, and Teva Pharmaceuticals. Companies active in the Incretin-based Drugs Market are implementing several strategic initiatives to reinforce their competitive position and expand global reach. Major pharmaceutical firms are prioritizing research and development investments to advance innovative formulations and improve therapeutic performance. Strategic partnerships and collaborative agreements with research institutions and biotechnology firms are also becoming common, allowing companies to accelerate drug development and expand product pipelines. Market participants are strengthening their presence in emerging healthcare markets through distribution expansion and localized commercialization strategies. In addition, organizations are focusing on regulatory approvals and clinical trials to support new product introductions and broaden therapeutic indications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.10 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Drug type trends

- 2.2.2 Route of Administration trends

- 2.2.3 Indication trends

- 2.2.4 Distribution channel trends

- 2.2.5 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Rising prevalence of type 2 diabetes mellitus

- 3.2.3 Shift toward non-insulin therapies

- 3.2.4 Advancements in drug delivery technologies

- 3.2.5 Cardiovascular and weight management benefits

- 3.2.6 Industry pitfalls and challenges

- 3.2.7 High treatment costs

- 3.2.8 Adverse effects and contraindications

- 3.2.9 Market opportunities

- 3.2.9.1 Growing patient awareness and cultural shifts in obesity management

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Patent analysis (Driven by Primary Research)

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 GLP-1 receptor agonists

- 5.3 DPP-4 inhibitors

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Injectable

Chapter 7 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Type 2 diabetes mellitus

- 7.3 Obesity and weight management

- 7.4 Other metabolic disorders

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AstraZeneca

- 10.2 Boehringer Ingelheim

- 10.3 Eli Lilly and Company

- 10.4 GlaxoSmithKline

- 10.5 Merck

- 10.6 Novo Nordisk

- 10.7 Pfizer

- 10.8 Sanofi

- 10.9 Takeda Pharmaceutical Company

- 10.10 Teva Pharmaceuticals