|

市場調查報告書

商品編碼

1998750

艦載通訊與控制系統市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測Marine Onboard Communication and Control Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

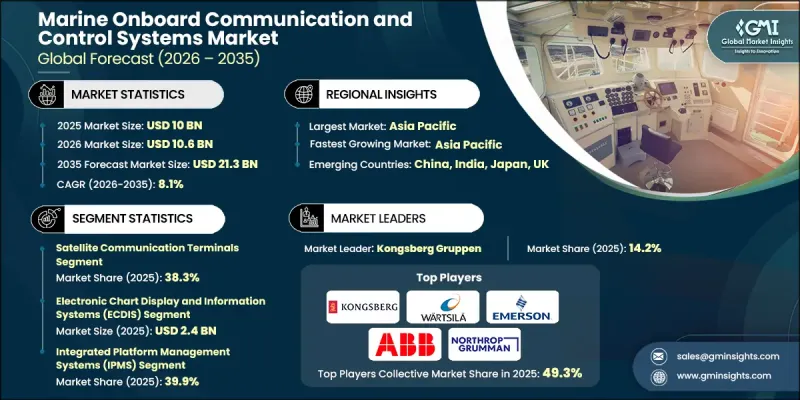

全球船舶通訊和控制系統市場預計到 2025 年將達到 100 億美元,預計到 2035 年將以 8.1% 的複合年成長率成長至 213 億美元。

智慧船舶自動化平台的日益普及、對可靠海事衛星通訊需求的成長以及全球商船隊的持續擴張,共同推動了市場的擴張。數位導航和海事安全框架的進步,以及即時船舶監控和船隊管理系統的整合,進一步促進了市場成長。航運公司越來越依賴整合導航、推進和操作控制的互聯船載系統,從而提高效率、營運安全性和合規性。政府對數位海事基礎設施的投資以及旨在提升船隊監控、海事態態感知和運營安全性的各項舉措,也促進了先進船載通訊和控制解決方案的普及。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 100億美元 |

| 預計金額 | 213億美元 |

| 複合年成長率 | 8.1% |

預計到2025年,衛星通訊終端市佔率將達到38.3%,這主要得益於其能夠提供船舶與陸地基地之間不間斷的遠端通訊。這些系統支援即時航線更新、營運管理以及跨越廣闊海域的船員之間的無縫通訊,從而推動了市場需求的持續成長。

電子海圖顯示與資訊系統(ECDIS)市場預計到2025年將達到24億美元,其在數位導航和海上安全方面發揮的關鍵作用是推動市場成長的主要因素。 ECDIS透過提供即時導航資料、提高情境察覺並確保符合監管要求,正在取代傳統的紙質海圖。 ECDIS與雷達、AIS和GNSS系統的整合進一步提升了其在商業船隊中的重要性和普及性。

到2025年,北美船上通訊和控制系統市場佔有率將達到28.3%。這一區域成長主要得益於海軍現代化、海上作業以及數位化船舶技術的廣泛應用方面的大量投資。商船公司和海軍當局正日益採用船上自動化、整合艦橋系統和衛星通訊解決方案,以提高營運安全性和效率。政府在海上情境察覺、海軍通訊和艦隊監視方面的舉措也持續推動先進船上系統的應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 擴大智慧船舶和互聯船舶的應用。

- 對海上衛星通訊的需求不斷成長

- 全球海運貿易與船隊規模的擴張

- 對即時船舶監控系統的需求日益成長

- 國際海事組織(IMO)的規定促進了數位導航系統的應用。

- 產業潛在風險與挑戰

- 老舊車隊的引進和維修成本高昂

- 車載網路的網路安全風險

- 市場機遇

- 自主和遙控船舶的開發

- 擴大衛星寬頻在海上船舶的應用

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興競爭對手和Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依通訊系統分類,2022-2035年

- 衛星通訊終端

- VSAT終端

- L波段終端

- 船舶無線電系統

- 甚高頻無線電系統

- 中頻/高頻無線系統

- GMDSS設備

- 車上網路基礎設施

- 路由器和交換機

- 車載寬頻骨幹系統

- 艦載通訊系統

- 廣播/通用警報(PA/GA)系統

- 對講系統

第6章 市場估算與預測:依導航與定位系統分類,2022-2035年

- 電子海圖顯示與資訊系統(ECDIS)

- 雷達系統

- X波段雷達

- S臂雷達

- 自動辨識系統(AIS)

- 全球導航衛星系統(GNSS/GPS)

- 導航資料記錄器(VDR)

- 動態定位系統

第7章 市場估算與預測:依控制與自動化系統分類,2022-2035年

- 推進控制系統

- 引擎自動化系統

- 推進器控制系統

- 電源管理系統

- 整合平台管理系統(IPMS)

第8章 市場估算與預測:依監控系統應用領域分類,2022-2035年

- 火災偵測系統

- 氣體檢測系統

- CCTV和車載安全系統

- 船體應力監測系統

- 狀態監控系統

第9章 市場估計與預測:依平台分類,2022-2035年

- 商船

- 客船

- 貨船

- 遠洋船舶和特種船舶

- 防禦艦

- 航空母艦

- 驅逐艦

- 護衛艦

- 克爾維特

- 潛水艇

- 兩棲攻擊艦

第10章 市場估價與預測:依最終用戶分類,2022-2035年

- OEM

- 售後市場

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 主要企業

- ABB Group

- Kongsberg

- Wartsila

- Northrop Grumman Corporation

- Honeywell International Inc.

- 按地區分類的主要企業

- 北美洲

- Emerson Electric Co.

- L3Harris Technologies, Inc.

- Viasat, Inc.

- 亞太地區

- Furuno Electric Co., Ltd.

- Japan Radio Co., Ltd.

- Raymarine

- 歐洲

- Saab AB

- ST Engineering

- 北美洲

- 特殊玩家/干擾者

- Navico Group

The Global Marine Onboard Communication and Control Systems Market was valued at USD 10 billion in 2025 and is estimated to grow at a CAGR of 8.1% to reach USD 21.3 billion by 2035.

The market expansion is driven by the increasing adoption of smart vessel automation platforms, rising demand for reliable maritime satellite connectivity, and the continuous growth of global commercial shipping fleets. The integration of real-time vessel monitoring and fleet management systems, alongside the advancement of digital navigation and maritime safety frameworks, is further supporting market growth. Shipping companies are increasingly relying on connected onboard systems that integrate navigation, propulsion, and operational control, enhancing efficiency, operational safety, and regulatory compliance. Government investments in digital maritime infrastructure and initiatives aimed at improving fleet monitoring, maritime domain awareness, and operational safety are also contributing to the widespread adoption of advanced onboard communication and control solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10 Billion |

| Forecast Value | $21.3 Billion |

| CAGR | 8.1% |

The satellite communication terminals segment held 38.3% share in 2025, owing to their capability to provide uninterrupted long-range communication between ships and shore-based operations. These systems support real-time route updates, operational management, and seamless crew communication across vast maritime distances, driving sustained demand.

The electronic chart display and information systems (ECDIS) segment was valued at USD 2.4 billion in 2025 and dominated the market due to its crucial role in digital navigation and maritime safety. ECDIS replaces traditional paper charts by providing real-time navigational data, enhancing situational awareness, and complying with regulatory mandates. The integration of ECDIS with radar, AIS, and GNSS systems further strengthens its relevance and adoption across commercial fleets.

North America Marine Onboard Communication and Control Systems Market accounted for 28.3% share in 2025. The region's growth is supported by substantial investment in naval modernization, offshore maritime operations, and the deployment of digital vessel technologies. Commercial shipping companies and naval authorities are increasingly implementing onboard automation, integrated bridge systems, and satellite communication solutions to enhance operational safety and efficiency. Government initiatives focused on maritime domain awareness, naval communications, and fleet monitoring continue to encourage the adoption of advanced onboard systems.

Prominent players in the Global Marine Onboard Communication and Control Systems Market include L3Harris Technologies, Inc., Raymarine, Viasat, Inc., Northrop Grumman Corporation, Furuno Electric Co., Ltd., Kongsberg, ABB Group, ST Engineering, Wartsila, Honeywell International Inc., Navico Group, Emerson Electric Co., Saab Ab, and Japan Radio Co., Ltd. Companies in the Global Marine Onboard Communication and Control Systems Market are adopting multiple strategies to solidify their presence and expand market share. They are investing in research and development to deliver advanced, integrated communication, navigation, and control solutions. Strategic collaborations with shipbuilders, naval authorities, and fleet operators enhance technology adoption and service reach. Firms are diversifying product portfolios to include satellite communication terminals, ECDIS, integrated bridge systems, and fleet management solutions, enabling comprehensive offerings. Expanding regional operations, enhancing after-sales support, and ensuring regulatory compliance are also key strategies for strengthening market footholds and building long-term client relationships.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Communication systems trends

- 2.2.2 Navigation & positioning systems trends

- 2.2.3 Control & automation systems trends

- 2.2.4 Monitoring & surveillance systems trends

- 2.2.5 Platform trends

- 2.2.6 End-User trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of smart and connected vessels

- 3.2.1.2 Growing maritime satellite communication demand

- 3.2.1.3 Expansion of global seaborne trade and fleet size

- 3.2.1.4 Rising need for real-time vessel monitoring systems

- 3.2.1.5 IMO regulations driving digital navigation systems adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High installation and retrofitting costs for legacy fleets

- 3.2.2.2 Cybersecurity risks in connected shipboard networks

- 3.2.3 Market opportunities

- 3.2.3.1 Autonomous and remotely operated vessel development

- 3.2.3.2 Expansion of satellite broadband for offshore vessels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Communication Systems, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Satellite communication terminals

- 5.2.1 VSAT terminals

- 5.2.2 L-band terminals

- 5.3 Marine Radio Systems

- 5.3.1 VHF radio systems

- 5.3.2 MF/HF radio systems

- 5.3.3 GMDSS equipment

- 5.4 Onboard network infrastructure

- 5.4.1 Routers & switches

- 5.4.2 Onboard broadband backbone systems

- 5.5 Internal communication systems

- 5.5.1 Public address / general alarm (PA/GA) systems

- 5.5.2 Intercom systems

Chapter 6 Market Estimates and Forecast, By Navigation & Positioning Systems, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Electronic chart display & information systems (ECDIS)

- 6.3 Radar systems

- 6.3.1 X-Band radar

- 6.3.2 S-Band radar

- 6.4 Automatic identification systems (AIS)

- 6.5 Global navigation satellite systems (GNSS/GPS)

- 6.6 Voyage data recorders (VDR)

- 6.7 Dynamic positioning systems

Chapter 7 Market Estimates and Forecast, By Control & Automation Systems, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Propulsion control systems

- 7.3 Engine automation systems

- 7.4 Thruster control systems

- 7.5 Power management systems

- 7.6 Integrated platform management systems (IPMS)

Chapter 8 Market Estimates and Forecast, By Monitoring & Surveillance Systems Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Fire detection systems

- 8.3 Gas detection systems

- 8.4 CCTV & onboard security systems

- 8.5 Hull stress monitoring systems

- 8.6 Condition-based monitoring systems

Chapter 9 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Commercial vessels

- 9.2.1 Passenger vessels

- 9.2.2 Cargo vessels

- 9.2.3 Offshore & specialized vessels

- 9.3 Defense vessels

- 9.3.1 Aircraft carriers

- 9.3.2 Destroyers

- 9.3.3 Frigates

- 9.3.4 Corvettes

- 9.3.5 Submarines

- 9.3.6 Amphibious assault ships

Chapter 10 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 ABB Group

- 12.1.2 Kongsberg

- 12.1.3 Wartsila

- 12.1.4 Northrop Grumman Corporation

- 12.1.5 Honeywell International Inc.

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 Emerson Electric Co.

- 12.2.1.2 L3Harris Technologies, Inc.

- 12.2.1.3 Viasat, Inc.

- 12.2.2 Asia Pacific

- 12.2.2.1 Furuno Electric Co., Ltd.

- 12.2.2.2 Japan Radio Co., Ltd.

- 12.2.2.3 Raymarine

- 12.2.3 Europe

- 12.2.3.1 Saab AB

- 12.2.3.2 ST Engineering

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Navico Group

指揮控制系統市場-2026-2032年全球市場預測

指揮控制系統市場-2026-2032年全球市場預測 2026 年至 2035 年指揮控制系統的市場機會、成長促進因素、產業趨勢分析與預測。

2026 年至 2035 年指揮控制系統的市場機會、成長促進因素、產業趨勢分析與預測。 船上通訊與控制系統市場報告:趨勢、預測及競爭分析(至2035年)

船上通訊與控制系統市場報告:趨勢、預測及競爭分析(至2035年) 2026-2030年全球指揮控制系統市場全球國防前置控制面板(UFC)市場(2026-2036 年)

2026-2030年全球指揮控制系統市場全球國防前置控制面板(UFC)市場(2026-2036 年) 2026年全球太空執法市場報告2026年全球船上通訊與控制系統市場報告艦載通訊與控制系統市場:2026-2032年全球市場預測(依系統類型、組件、通訊介質、安裝配置、船舶類型、應用及最終用戶分類)2026年全球指揮控制系統市場報告全球國防砲手控製手柄(操縱桿):2026-2036 年

2026年全球太空執法市場報告2026年全球船上通訊與控制系統市場報告艦載通訊與控制系統市場:2026-2032年全球市場預測(依系統類型、組件、通訊介質、安裝配置、船舶類型、應用及最終用戶分類)2026年全球指揮控制系統市場報告全球國防砲手控製手柄(操縱桿):2026-2036 年