|

市場調查報告書

商品編碼

1998742

自動配藥器市場機會、成長要素、產業趨勢分析及2026-2035年預測Automatic Pill Dispenser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

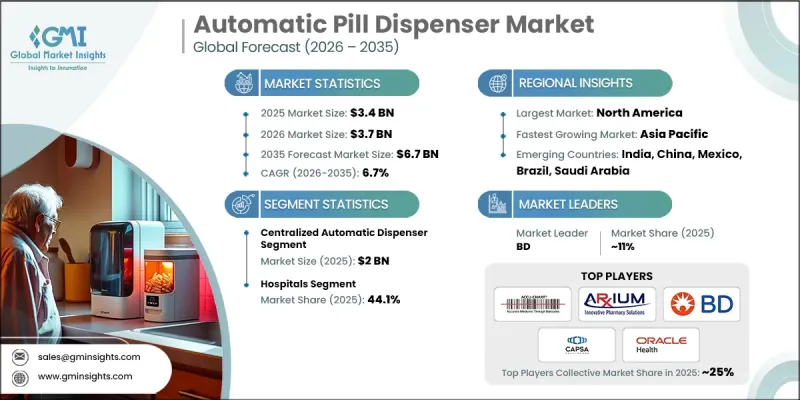

全球自動化藥物管理系統市場預計到 2025 年將達到 34 億美元,預計到 2035 年將以 6.7% 的複合年成長率成長至 67 億美元。

自動化藥物管理設備市場的成長主要受以下因素驅動:失智症和其他神經退化性疾病盛行率的上升、老年人口的快速成長以及全球處方藥需求的不斷增加。自動化藥物管理設備旨在幫助患者整理藥物、按時且準確地服用,並提高對處方治療方案的依從性。這些設備對於服用多種藥物的患者或有認知障礙、難以維持規律用藥習慣的患者尤其重要。人們對藥物依從性重要性的認知不斷提高,促使醫療保健系統和支持機構推廣能夠幫助患者正確執行治療方案的解決方案。自動化藥物管理工具也有利於看護者,因為它們可以簡化日常用藥管理的複雜性。同時,隨著遠端醫療服務和遠端患者監護技術的普及,自動化藥物管理設備在現代醫療保健中的作用日益重要。機構照護成本的上升以及對更舒適照護環境的需求,推動了居家醫療服務需求的成長,進而進一步促進了對使用者友善自動化醫療設備(例如自動藥物分發器)的需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 34億美元 |

| 預計金額 | 67億美元 |

| 複合年成長率 | 6.7% |

預計2025年,集中式自動化配藥系統市場規模將達20億美元。這些系統廣泛應用於大規模醫療機構,高效的藥品儲存、配發和追蹤對於提升營運效率至關重要。集中式配藥技術支援精準的藥品分發,同時也有助於醫護人員更好地管理藥品庫存。藥品分發錯誤仍然是醫療機構面臨的一大難題,但自動化集中管理系統透過確保準確一致的藥品管理,有助於最大限度地降低這些風險。除了提高準確性之外,這些系統還能透過維護詳細的藥品分發電子記錄,幫助醫療機構遵守監管標準,並滿足文件記錄和報告要求。

預計到2025年,醫院市場將佔據44.1%的市場佔有率,並在2026年至2035年間達到28億美元。醫院每天管理大量的藥品,因此對可靠的配藥系統有著日益成長的需求,以降低用藥錯誤的發生機率。自動化配藥技術有助於提高用藥準確性,降低不利事件的風險,最終改善患者的治療效果。人口結構變化和慢性病盛行率上升導致住院患者人數增加,進而推動了醫院環境中對高效藥物管理系統的需求。此外,與醫院庫存管理系統整合的自動藥片分發器使醫護人員能夠更有效地監控藥品庫存。即時追蹤功能有助於防止藥品短缺,並透過改進庫存管理最大限度地減少廢棄物。

預計2025年,美國自動配藥機市場規模將達12億美元。美國居家醫療產業的擴張是推動這一成長的主要動力,因為越來越多的人傾向於居家照護而非機構照護。自動化藥物管理系統使老年人和慢性病患者能夠獨立管理處方藥,從而減少對持續看護者監督的依賴。政府的醫療保健政策也鼓勵採用有助於提高用藥依從性和改善病人安全的技術。此外,保險公司對居家醫療解決方案的報銷支援也進一步促進了自動化藥物管理技術在住宅機構的應用。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策和資料完整性計劃

- 資訊來源一致性通訊協定

- GMI人工智慧政策和資料完整性計劃

- 調查過程和可靠性評分

- 調查過程的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 失智症和神經退化性疾病失智症不斷上升

- 人口老化和吸毒人數增加

- 技術進步

- 引入遠端醫療和遠端患者監護

- 產業潛在風險與挑戰

- 設備高成本

- 市場機遇

- 先進的智慧和人工智慧平板電腦分發器的興起

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 技術趨勢(基於初步調查)

- 當前技術趨勢

- 新興技術

- 未來市場趨勢

- 專利分析

- 2025年價格分析(基於初步調查)

- 客戶洞察(基於初步研究)

- 波特五力分析

- 人工智慧和生成式人工智慧對市場的影響

- PESTEL 分析

- 差距分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品類型發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 集中式自動配藥機

- 機器人

- 旋轉木馬

- 分散式自動配藥機

- 病房自動化配藥系統

- 藥房安裝的自動配藥系統

- 單劑量自動配藥系統

第6章 市場估算與預測:依最終用途分類,2022-2035年

- 醫院

- 老年護理機構

- 藥局

- 其他最終用戶

第7章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- ACCU-CHART

- ARxIUM

- BD

- CAPSA HEALTHCARE

- Hero Health

- InstyMeds

- McKesson

- Medipense

- MedMinder

- Omnicell

- Oracle Health

- PharmaCell

- ScriptPro

- swisslog healthcare

The Global Automatic Pill Dispenser Market was valued at USD 3.4 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 6.7 billion by 2035.

Growth in the automatic pill dispenser market is driven by the increasing prevalence of dementia and other neurodegenerative conditions, a rapidly expanding aging population, and the growing volume of prescription medications worldwide. Automatic pill dispensers are designed to assist individuals in organizing and dispensing medications in a timely and accurate manner, improving adherence to prescribed treatment schedules. These devices are particularly valuable for individuals managing multiple medications or those experiencing cognitive challenges that may affect their ability to maintain consistent medication routines. Rising awareness regarding the importance of medication adherence is encouraging healthcare systems and support organizations to promote solutions that help patients follow treatment plans correctly. Caregivers also benefit from automated medication management tools that reduce the complexity of supervising daily dosing schedules. At the same time, the expanding adoption of telehealth services and remote patient monitoring technologies is strengthening the role of automated medication management devices in modern healthcare. The growing preference for home-based healthcare services, supported by the increasing cost of institutional care and the desire for more comfortable care environments, is further boosting the demand for user-friendly automated medical devices such as automatic pill dispensers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.4 Billion |

| Forecast Value | $6.7 Billion |

| CAGR | 6.7% |

The centralized automatic dispenser segment generated USD 2 billion in 2025. These systems are widely utilized within large healthcare institutions where efficient medication storage, dispensing, and tracking are essential for operational performance. Centralized dispensing technologies support accurate medication distribution while helping healthcare providers maintain better control over pharmaceutical inventories. Medication dispensing errors remain a significant concern within healthcare environments, and automated centralized systems help minimize these risks by delivering precise and consistent medication handling. In addition to improving accuracy, these systems help healthcare institutions comply with regulatory standards by maintaining detailed digital records of medication distribution, which supports documentation and reporting requirements.

The hospitals segment held 44.1% share in 2025 and is projected to reach USD 2.8 billion during 2026-2035. Hospitals manage substantial volumes of medications each day, which increases the need for highly reliable dispensing systems that reduce the likelihood of medication-related errors. Automated dispensing technologies enhance accuracy in medication administration and help reduce the risk of adverse drug events, ultimately supporting improved patient outcomes. The growing number of patient admissions, supported by demographic shifts and the rising prevalence of chronic diseases, is increasing the demand for efficient medication management systems within hospital environments. Additionally, automatic pill dispensers connected with hospital inventory management systems allow healthcare providers to monitor pharmaceutical supplies more effectively. Real-time tracking capabilities help prevent medication shortages while minimizing waste through improved stock management.

United States Automatic Pill Dispenser Market reached USD 1.2 billion in 2025. Expansion of the home healthcare sector in the United States is a major factor supporting this growth, as many individuals increasingly prefer receiving care within their homes rather than in institutional settings. Automated medication dispensing systems allow elderly individuals and patients with chronic conditions to manage prescriptions independently while reducing reliance on continuous caregiver supervision. Government healthcare policies are also supporting the adoption of technologies that promote medication adherence and improve patient safety. Reimbursement support for home healthcare solutions further strengthens the adoption of automated medication management technologies within residential care environments.

Key companies participating in the Global Automatic Pill Dispenser Market include Omnicell, MedMinder, ARxIUM, BD, ScriptPro, CAPSA HEALTHCARE, McKesson, InstyMeds, swisslog healthcare, Medipense, Hero Health, ACCU-CHART, PharmaCell, and Oracle Health. Companies operating in the Automatic Pill Dispenser Market are implementing several strategic initiatives to strengthen their competitive positioning and expand market reach. Product innovation remains a major focus, with manufacturers investing in advanced dispensing technologies that integrate digital monitoring, connectivity, and smart alerts to improve medication adherence. Many companies are also forming strategic partnerships with healthcare providers, pharmacies, and technology firms to enhance product integration within healthcare systems. Expansion of distribution networks and manufacturing capacity is helping companies meet growing global demand for automated medication management devices. Additionally, organizations are increasingly incorporating remote monitoring features and telehealth compatibility into their products to support evolving healthcare delivery models.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising dementia & neurodegenerative disorders

- 3.2.1.2 Surging aging population & higher medication usage

- 3.2.1.3 Technological advancements

- 3.2.1.4 Adoption of telehealth & remote patient monitoring

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of the device

- 3.2.3 Market opportunities

- 3.2.3.1 Rise of advanced smart & AI-enabled pill dispensers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Pricing analysis, 2025 (Driven by Primary Research)

- 3.9 Customer insights (Driven by Primary Research)

- 3.10 Porter's analysis

- 3.11 Impact of AI and generative AI on the market

- 3.12 PESTEL analysis

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Centralized automatic dispenser

- 5.2.1 Robotic

- 5.2.2 Carousels

- 5.3 Decentralized automatic dispenser

- 5.3.1 Ward based automated dispensing system

- 5.3.2 Pharmacy based automated dispensing system

- 5.3.3 Automatic unit dose dispensing system

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Senior care facilities

- 6.4 Pharmacies

- 6.5 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 ACCU-CHART

- 8.2 ARxIUM

- 8.3 BD

- 8.4 CAPSA HEALTHCARE

- 8.5 Hero Health

- 8.6 InstyMeds

- 8.7 McKesson

- 8.8 Medipense

- 8.9 MedMinder

- 8.10 Omnicell

- 8.11 Oracle Health

- 8.12 PharmaCell

- 8.13 ScriptPro

- 8.14 swisslog healthcare

自動配藥器市場:依連接方式、配藥室數量、定時方式、機制、最終用戶和通路分類-2026-2032年全球市場預測

自動配藥器市場:依連接方式、配藥室數量、定時方式、機制、最終用戶和通路分類-2026-2032年全球市場預測 自動藥品分發器市場報告:按類型、應用和地區分類(2026-2034 年)

自動藥品分發器市場報告:按類型、應用和地區分類(2026-2034 年) 全球自動化藥品分發器市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球自動化藥品分發器市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球智慧藥丸分發器市場報告2026年全球自動藥片分發器市場報告

2026年全球智慧藥丸分發器市場報告2026年全球自動藥片分發器市場報告 藥片定時器市場按類型、產品類型、最終用戶、技術、分銷管道和地區分類

藥片定時器市場按類型、產品類型、最終用戶、技術、分銷管道和地區分類 全球藥物分配器市場全球自動錠劑分配器市場

全球藥物分配器市場全球自動錠劑分配器市場 自動錠劑分配器市場分析及預測(至2034年):類型、產品、技術、組件、應用、最終用戶、功能、安裝類型、模式

自動錠劑分配器市場分析及預測(至2034年):類型、產品、技術、組件、應用、最終用戶、功能、安裝類型、模式 自動錠劑分配器市場規模、佔有率和成長分析(按類型、最終用戶和地區)- 產業預測,2025 年至 2032 年

自動錠劑分配器市場規模、佔有率和成長分析(按類型、最終用戶和地區)- 產業預測,2025 年至 2032 年