|

市場調查報告書

商品編碼

1998738

電動商用車驅動馬達市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Electric Commercial Vehicle Traction Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

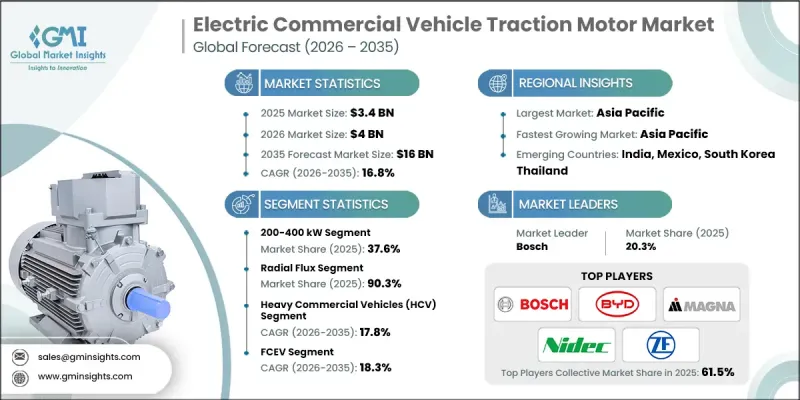

2025 年全球電動商用車驅動馬達市場價值為 34 億美元,預計到 2035 年將達到 160 億美元,年複合成長率為 16.8%。

驅動馬達將電能轉化為機械能,驅動卡車、廂型車、巴士和其他重型車輛,在電動商用車中發揮至關重要的作用。隨著商務傳輸車輛電氣化程度的不斷提高,這些馬達正成為實現車輛高效性能的最重要部件之一。營運商用車的公司越來越意識到電動推進系統帶來的經濟效益。與傳統動力傳動系統技術相比,電動驅動馬達具有更高的能源效率和更低的營運成本。此外,由於活動部件更少,電動車通常需要的維護也更少,從而降低了維修成本和車輛運作。這些成本優勢使得電動商用車成為尋求長期營運效率的車隊營運商的理想選擇。隨著全球交通運輸系統不斷向低排放量出行方式轉型,對先進驅動馬達技術的需求預計將顯著成長,從而推動全球電動商用車驅動馬達市場的持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 34億美元 |

| 預計金額 | 160億美元 |

| 複合年成長率 | 16.8% |

旨在減少交通運輸領域排放氣體的政府措施和法規結構正在進一步加速電動商用車及其相關零件的普及。許多地方政府在實施更嚴格的環保標準的同時,也推出了稅收減免和財政補貼等獎勵,鼓勵企業轉型使用電動車。這些政策措施為高性能驅動馬達的研發創造了有利環境。同時,技術創新也不斷提升馬達的效率、耐久性和熱性能。現代馬達設計正朝著更最佳化的方向發展,以更低的電力消耗實現更高的功率輸出。馬達架構和先進材料的持續改進,使得車輛能夠實現更長的續航里程、更快的加速性能和更高的可靠性。

功率範圍為200-400千瓦的驅動馬達佔據37.6%的市場佔有率,預計到2025年市場規模將達到13億美元。此功率範圍的驅動馬達通常用於中型和重型電動卡車和巴士,這些車輛需要強大的動力來長途運輸重物。這些馬達能夠提供足夠的動力來滿足嚴苛的商業應用需求,同時保持高效能和耐用性。雖然該功率範圍的馬達製造成本通常高於低功率型號,但它們採用了先進技術,旨在承受惡劣的運作條件。隨著商務傳輸車輛加速採用電動動力傳動系統以滿足法規和環保目標,預計全球市場對能夠驅動重型車輛的高功率驅動馬達的需求將穩步成長。

徑向磁通馬達目前佔據90.3%的市場佔有率,預計到2035年將達到142億美元。由於其可靠性和穩定性,徑向磁通馬達長期以來被廣泛應用於電動車驅動系統。其相對簡單的設計便於大規模生產,有助於在確保高機械耐久性的同時,維持成本效益。這些馬達尤其適用於需要在長途運輸重物的同時保持穩定性能的商用車輛。車隊營運商和製造商青睞徑向磁通電機,因為它能夠在提供高扭矩和高功率的同時,保持高效的能源消耗。隨著全球商用電動車產量的不斷成長,徑向磁通馬達技術預計將繼續成為許多重型車輛應用領域的首選解決方案。

美國電動商用車驅動馬達市場預計到2025年將達到3.954億美元,並在2026年至2035年間以15.6%的複合年成長率成長。旨在減少交通運輸領域排放氣體並支持電動出行的政府政策在加速全國市場成長方面發揮著重要作用。各州的法規結構正在影響車輛製造標準,並促進更清潔交通技術的應用。這些政策為企業創造了專門為電動商用車設計製造驅動馬達的機會。隨著環境法規的不斷收緊以及電氣化成為交通運輸領域的戰略重點,預計美國仍將是支持電動商用車驅動馬達技術創新和投資的領先市場。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 成長促進因素

- 嚴格的排放氣體法規和強制性零排放

- 與內燃機車相比,總擁有成本 (TCO) 的優勢

- 政府對商用電動車隊的獎勵與補貼

- 快速的都市化和對最後一公里配送的需求

- 產業潛在風險與挑戰

- 在長途運輸領域與氫燃料電池動力傳動系統競爭

- 馬達在惡劣運轉條件下的過熱和耐久性

- 市場機遇

- 物流與電子商務公司車輛的電氣化

- 政府投資公共交通電氣化

- 電池更換和超快速充電網路的擴展

- 馬達效率和功率密度方面的技術突破

- 成長促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國環保署(EPA)

- 美國國家公路交通安全管理局(NHTSA)

- 加拿大運輸部(TC)

- 歐洲

- 歐盟委員會(EC)

- 歐盟103年第168號條例

- 國際標準化組織(ISO)

- 亞太地區

- 中國國家標準化管理委員會(SAC)

- 日本汽車標準國際化中心(JASIC)

- 拉丁美洲

- 國家計量院(INMETRO)

- 墨西哥通訊與運輸部部 (SCT)

- 中東和非洲

- 南非標準局(SABS)

- 沙烏地阿拉伯標準、計量和品質組織(SASO)

- 北美洲

- 投資與資金籌措分析

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 目前技術

- 永磁同步馬達(PMSM)

- 感應電動機(非同步電動機)

- 開關式磁阻電動機(SRM)

- 新興技術

- 固態馬達

- 高溫超導性馬達(HTS)

- 目前技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按球員類型分類的定價策略(高階/超值/成本加成)

- 專利趨勢(基於初步調查)

- 貿易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 生產能力和生產趨勢(基於初步調查)

- 區域部署能力和主要製造商

- 運轉率和擴張計劃

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- GenAI 各細分市場的應用案例與實施藍圖

- 風險、限制和監管考量

- 電池技術與驅動馬達之間的關係

- 電池化學的演變及其與馬達的兼容性

- 電壓架構發展趨勢(400V 系統與 800V 系統)

- 電池和電機溫度控管的整合

- 荷電狀態 (SOC) 對馬達性能的影響

- 驅動馬達壽命週期和永續性

- 對稀土元素材料的依賴與供應鏈風險

- 邁向循環經濟和再製造的舉措

- 廢舊產品的回收和材料再利用

- 碳足跡分析

- 案例研究

- 未來前景與機遇

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估算與預測:依馬達類型分類,2022-2035年

- 永磁同步馬達(PMSM)

- 開關式磁阻電動機(SRM)

- 感應電動機

- 直流牽引電機

- 勵磁式同步馬達

第6章 市場估計與預測:依產量分類,2022-2035年

- 小於100千瓦

- 100~200 kW

- 200~400 kW

- 超過400千瓦

第7章 市場估價與預測:依馬達設計分類,2022-2035年

- 徑向通量

- 軸流式

第8章 市場估算與預測:依車軸結構分類,2022-2035年

- 一體式車軸

- 中央驅動單元

第9章 市場估計與預測:依輸電類型分類,2022-2035年

- 單速驅動

- 多速驅動

第10章 市場估價與預測:依車輛類型分類,2022-2035年

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第11章 市場估計與預測:依動力傳動系統,2022-2035年

- BEV

- PHEV

- FCEV

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 比利時

- 瑞典

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- 世界公司

- BYD

- ZF Friedrichshafen

- Dana

- Robert Bosch

- Magna

- Allison

- ABB

- BorgWarner

- Valeo

- Nidec

- 當地公司

- TECO Electric & Machinery

- Brogen

- Broad-Ocean Motor

- WEG

- American Axle & Manufacturing

- Mahle

- 新興企業

- Equipmake

- YASA

- Saietta

- Protean Electric

The Global Electric Commercial Vehicle Traction Motor Market was valued at USD 3.4 billion in 2025 and is estimated to grow at a CAGR of 16.8% to reach USD 16 billion by 2035.

Traction motors play a crucial role in electric commercial vehicles by converting electrical energy into mechanical power that drives trucks, vans, buses, and other heavy-duty vehicles. As electrification spreads across commercial transportation fleets, these motors are becoming one of the most important components enabling efficient vehicle performance. Businesses operating commercial vehicles are increasingly recognizing the economic advantages associated with electric propulsion systems. Electric traction motors offer improved energy efficiency and lower operational costs compared with conventional powertrain technologies. In addition, electric vehicles typically require less maintenance because they contain fewer moving components, which reduces repair expenses and vehicle downtime. These cost savings make electric commercial vehicles an attractive solution for fleet operators seeking long-term operational efficiency. As global transportation systems continue transitioning toward low-emission mobility, the demand for advanced traction motor technologies is expected to rise significantly, supporting sustained growth in the global electric commercial vehicle traction motor market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.4 Billion |

| Forecast Value | $16 Billion |

| CAGR | 16.8% |

Government initiatives and regulatory frameworks designed to reduce transportation emissions are further accelerating the adoption of electric commercial vehicles and their associated components. Authorities in many regions are implementing stricter environmental standards while introducing incentives such as tax benefits and financial subsidies to encourage businesses to transition toward electric fleets. These policy measures are creating a favorable environment for manufacturers developing high-performance traction motors. At the same time, technological innovation is improving motor efficiency, durability, and thermal performance. Modern motor designs are increasingly optimized to deliver higher power output while consuming less electrical energy. Continuous improvements in motor architecture and advanced materials are enabling vehicles to achieve greater operational range, faster acceleration, and improved reliability.

The 200-400 kW power segment held a 37.6% share, generating USD 1.3 billion in 2025. Traction motors within this power range are commonly used in medium-duty and heavy-duty electric trucks and buses that require strong propulsion capabilities to transport substantial loads across extended distances. These motors deliver sufficient power to support demanding commercial applications while maintaining efficiency and durability. Although motors in this category typically involve higher production costs than lower-power alternatives, they incorporate advanced engineering designed to handle intensive operational conditions. As commercial transportation fleets increasingly adopt electric powertrains to meet regulatory and environmental objectives, the demand for high-capacity traction motors capable of supporting large vehicles is expected to grow steadily across global markets.

The radial flux motor segment held 90.3% share and is projected to reach USD 14.2 billion by 2035. Radial flux motors have been widely utilized in electric vehicle traction systems for many years due to their proven reliability and consistent operational performance. Their relatively simple design structure makes them easier to manufacture at scale, which helps maintain cost efficiency while ensuring strong mechanical durability. These motors are particularly suitable for commercial vehicles that must transport heavy loads over long distances while maintaining stable performance levels. Fleet operators and manufacturers value radial flux motors for their ability to deliver high torque and power output while maintaining efficient energy consumption. As commercial electric vehicle production expands globally, radial flux motor technology is expected to remain a preferred solution for many heavy-duty vehicle applications.

United States Electric Commercial Vehicle Traction Motor Market generated USD 395.4 million in 2025 and is expected to grow at a CAGR of 15.6% between 2026 and 2035. Government policies aimed at reducing transportation emissions and supporting electric mobility are playing a major role in accelerating market growth across the country. Regulatory frameworks across various states are influencing vehicle manufacturing standards and encouraging the adoption of cleaner transportation technologies. These policies are creating opportunities for companies to produce traction motors specifically designed for electric commercial vehicles. As environmental regulations continue to tighten and electrification becomes a strategic priority for the transportation sector, the United States is expected to remain a key market supporting innovation and investment in electric commercial vehicle traction motor technologies.

Major companies operating in the Global Electric Commercial Vehicle Traction Motor Market include ABB, Allison, BorgWarner, BYD, Dana, Magna, Nidec, Robert Bosch, Valeo, and ZF Friedrichshafen. Companies participating in the Global Electric Commercial Vehicle Traction Motor Market are implementing several strategies to strengthen their competitive positioning and expand their global presence. Manufacturers are investing heavily in research and development to improve motor efficiency, thermal management, and power density in order to meet the performance requirements of next-generation electric commercial vehicles. Many firms are also forming strategic partnerships with vehicle manufacturers to integrate traction motor systems into new electric truck and bus platforms. Expansion of manufacturing facilities and supply chain capabilities is another key focus area as companies aim to support growing demand for electrified transportation solutions. Additionally, businesses are developing modular motor architectures and advanced control technologies to improve product versatility, reduce production costs, and enhance long-term reliability for commercial fleet applications.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Motor

- 2.2.3 Power Output

- 2.2.4 Motor Design

- 2.2.5 Axle Architecture

- 2.2.6 Transmission

- 2.2.7 Vehicle

- 2.2.8 Powertrain

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent emission regulations & zero-emission mandates

- 3.2.1.2 Total cost of ownership (TCO) advantages over ICE vehicles

- 3.2.1.3 Government incentives & subsidies for electric commercial fleets

- 3.2.1.4 Rapid urbanization & last-mile delivery demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Competition from hydrogen fuel cell powertrains in long-haul segments

- 3.2.2.2 Motor overheating & durability in extreme operating conditions

- 3.2.3 Market opportunities

- 3.2.3.1 Fleet electrification by logistics & e-commerce companies

- 3.2.3.2 Government investments in public transit electrification

- 3.2.3.3 Expansion of battery swapping & ultra-fast charging networks

- 3.2.3.4 Technological breakthroughs in motor efficiency & power density

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.3 Transportation Canada (TC)

- 3.4.2 Europe

- 3.4.2.1 European Commission (EC)

- 3.4.2.2 European Union Regulation (EU) No 168/2013

- 3.4.2.3 International Organization for Standardization (ISO)

- 3.4.3 Asia Pacific

- 3.4.3.1 China National Standardization Administration (SAC)

- 3.4.3.2 Japan Automobile Standards Internationalization Center (JASIC)

- 3.4.4 Latin America

- 3.4.4.1 Instituto Nacional de Metrologia (INMETRO)

- 3.4.4.2 Mexico's Secretaria de Comunicaciones y Transportes (SCT)

- 3.4.5 Middle East & Africa

- 3.4.5.1 South African Bureau of Standards (SABS)

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.1 North America

- 3.5 Investment & Funding Analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 Permanent Magnet Synchronous Motors (PMSM)

- 3.8.1.2 Induction Motors (Asynchronous Motors)

- 3.8.1.3 Switched Reluctance Motors (SRM)

- 3.8.2 Emerging technologies

- 3.8.2.1 Solid-State Motors

- 3.8.2.2 High-Temperature Superconducting Motors (HTS)

- 3.8.1 Current technologies

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Trade data analysis (Driven by Paid Database)

- 3.11.1 Import/export volume & value trends

- 3.11.2 Key trade corridors & tariff impact

- 3.12 Capacity & production landscape (driven by primary research)

- 3.12.1 Installed capacity by region & key producer

- 3.12.2 Capacity utilization rates & expansion pipelines

- 3.13 Impact of AI & Generative AI on the Market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Battery technology and its interplay with traction motors

- 3.14.1 Battery chemistry evolution & motor compatibility

- 3.14.2 Voltage architecture trends (400V vs 800V systems)

- 3.14.3 Battery-motor thermal management integration

- 3.14.4 State of charge (SOC) impact on motor performance

- 3.15 Lifecycle and sustainability of traction motors

- 3.15.1 Rare earth material dependency & supply chain risks

- 3.15.2 Circular economy approaches & remanufacturing

- 3.15.3 End-of-life recycling & material recovery

- 3.15.4 Carbon footprint analysis

- 3.16 Case studies

- 3.17 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Motor, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Permanent Magnet Synchronous Motor (PMSM)

- 5.3 Switched Reluctance Motor (SRM)

- 5.4 AC Induction Motor

- 5.5 DC Traction Motor

- 5.6 Electrically Excited Synchronous Motor

Chapter 6 Market Estimates & Forecast, By Power Output, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Less than 100 kW

- 6.3 100-200 kW

- 6.4 200-400 kW

- 6.5 Above 400 kW

Chapter 7 Market Estimates & Forecast, By Motor Design, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Radial Flux

- 7.3 Axial Flux

Chapter 8 Market Estimates & Forecast, By Axle Architecture, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Integrated Axle

- 8.3 Central Drive Unit

Chapter 9 Market Estimates & Forecast, By Transmission, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 Single-Speed Drive

- 9.3 Multi-Speed Drive

Chapter 10 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 Light commercial vehicles (LCV)

- 10.3 Medium commercial vehicles (MCV)

- 10.4 Heavy commercial vehicles (HCV)

Chapter 11 Market Estimates & Forecast, By Powertrain, 2022 - 2035 ($Mn, Thousand Units)

- 11.1 Key trends

- 11.2 BEV

- 11.3 PHEV

- 11.4 FCEV

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Belgium

- 12.3.7 Sweden

- 12.3.8 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Chile

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 BYD

- 13.1.2 ZF Friedrichshafen

- 13.1.3 Dana

- 13.1.4 Robert Bosch

- 13.1.5 Magna

- 13.1.6 Allison

- 13.1.7 ABB

- 13.1.8 BorgWarner

- 13.1.9 Valeo

- 13.1.10 Nidec

- 13.2 Regional players

- 13.2.1 TECO Electric & Machinery

- 13.2.2 Brogen

- 13.2.3 Broad-Ocean Motor

- 13.2.4 WEG

- 13.2.5 American Axle & Manufacturing

- 13.2.6 Mahle

- 13.3 Emerging players

- 13.3.1 Equipmake

- 13.3.2 YASA

- 13.3.3 Saietta

- 13.3.4 Protean Electric