|

市場調查報告書

商品編碼

1998735

食品級抗菌劑市場機會、成長要素、產業趨勢分析及2026-2035年預測。Food Antimicrobials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

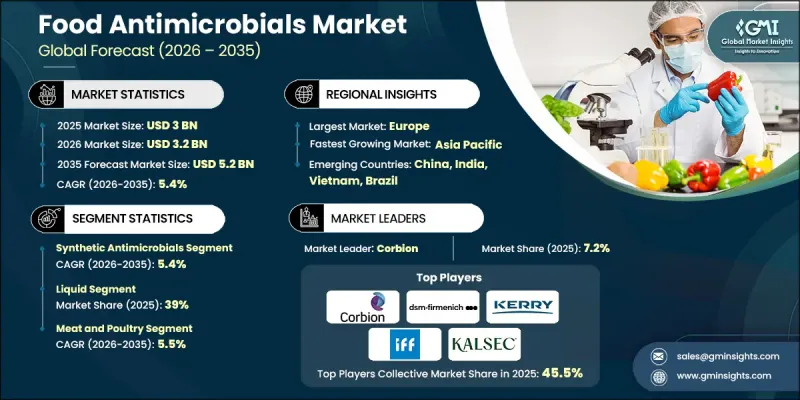

預計到 2025 年,全球食品級抗菌劑市場價值將達到 30 億美元,並預計以 5.4% 的複合年成長率成長,到 2035 年達到 52 億美元。

食品級抗菌劑涵蓋多種天然和合成化合物,旨在抑制可能危害食品品質和安全的微生物的生長。隨著食品生產和分銷系統日益複雜化和全球化,它們的角色也越來越重要。製造商尋求能夠延長保存期限、同時保持產品新鮮度、安全性和一致性的解決方案,因此對食品級抗菌劑的需求不斷成長。同時,消費者越來越關注那些被認為更健康、更透明的成分,這推動了潔淨標示抗菌配方的發展。食品級抗菌劑廣泛應用於眾多食品類別,在這些食品中,微生物穩定性在儲存、運輸和零售分銷過程中至關重要。包裝食品和簡便食品食品消費量的不斷成長進一步加速了食品級抗菌劑的應用,因為生產商需要可靠的保藏技術,既能保護產品質量,又不會對風味、質地或營養價值產生負面影響。對保藏技術的持續研究正在提高抗菌劑的功效,並擴大其與各種食品配方的兼容性,從而進一步提升其在現代食品製造中的重要性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 30億美元 |

| 預測金額 | 52億美元 |

| 複合年成長率 | 5.4% |

合成抗菌劑市佔率佔39.7%,預計到2035年將以5.4%的複合年成長率成長。由於其價格實惠、功能可靠且在各種生產條件下均能保持穩定的抗菌性能,這些解決方案在食品加工領域中廣泛應用。合成化合物已在許多國際市場獲得監管部門的核准,這為其在商業性食品生產中的大規模應用提供了支持。其可預測的活性和穩定性使生產商能夠在適當濃度下使用時,保持穩定的防腐效果,同時最大限度地減少對產品特性的影響。

預計到2025年,液體抗菌劑市佔率將達到39%,並在2035年之前以5.6%的複合年成長率成長。這些解決方案之所以備受青睞,是因為它們易於整合到食品加工系統中,並能均勻分散在整個產品配方中。其高溶解度和分散效率可實現精確計量和充分混合,有助於在整個生產批次中保持一致的抗菌效果。此外,液體抗菌劑還能有效融入液態或半液態食品基質,進而提高製作流程效率。

預計2035年,美國食品抗菌劑市場規模將達13億美元,2025年市佔率將達84.8%。這一成長得益於美國嚴格的食品安全監管框架以及消費者對產品品質和衛生標準的高度重視。美國高度發展的食品製造業持續推動對抗菌解決方案的需求,以確保產品在生產、包裝和分銷過程中的穩定性和安全性。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

(註:貿易統計數據僅涵蓋主要國家。)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 天然抗菌劑

- 有機酸

- 細菌素

- 精油和活性成分

- 植物萃取物和多酚

- 酵素

- 幾丁聚醣及其衍生物

- 抗菌胜肽

- 微生物防腐劑

- 其他

- 天然來源的抗菌劑

- 香草醛

- 芳樟醇

- 香豆素

- 其他

- 合成抗菌劑

- 苯甲酸

- 山梨酸鉀

- 亞硝酸鹽和硝酸鹽

- 亞硫酸鹽

- 丙酸酯

- 合成抗氧化劑(BHA、BHT、TBHQ、沒食子酸丙酯)

- 其他

第6章 市場估計與預測:依類型分類,2022-2035年

- 液體

- 粉末

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 肉類/雞肉

- 生鮮肉肉製品

- 加工肉品和醃製肉類

- 家禽產品

- 即食(RTE)肉品

- 其他

- 麵包糖果甜點

- 麵包和烘焙點心

- 蛋糕和酥皮點心

- 糖果甜點

- 其他

- 乳製品和冷凍甜點

- 生牛奶

- 乳酪製品

- 優格和發酵乳製品

- 冰淇淋和冷凍甜點

- 奶油

- 其他

- 飲料

- 果汁/果漿

- 軟性飲料和碳酸飲料

- 酒精飲料

- 其他

- 小吃

- 鹹味零食

- 烤堅果和花生醬

- 其他

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Celanese

- Corbion

- DSM-Firmenich

- Eastman

- Galactic

- International Flavors &Fragrances

- Jungbunzlauer

- Kalsec

- Kerry Group

- Mitsubishi Chemical

- Novonesis

The Global Food Antimicrobials Market was valued at USD 3 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 5.2 billion by 2035.

Food antimicrobials include a broad range of natural and synthetic compounds designed to suppress the growth of microorganisms that can compromise food quality and safety. Their role has become increasingly important as food production and distribution systems grow more sophisticated and globalized. Demand is rising as manufacturers seek solutions that support longer shelf life while maintaining freshness, safety, and consistent product quality. At the same time, consumers are showing greater interest in ingredients perceived as healthier and more transparent, which is encouraging the development of clean-label antimicrobial formulations. Food antimicrobials are widely incorporated into numerous food categories where microbial stability is critical throughout storage, transportation, and retail distribution. Growing consumption of packaged and convenience foods is further accelerating adoption, as producers require reliable preservation technologies that protect product integrity without negatively affecting flavor, texture, or nutritional value. Continuous research in preservation technologies is also improving antimicrobial effectiveness and expanding their compatibility with diverse food formulations, strengthening their importance in modern food manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 5.4% |

The synthetic antimicrobials segment held 39.7% share and is projected to grow at a CAGR of 5.4% through 2035. These solutions remain widely used in food processing due to their affordability, reliable functionality, and consistent antimicrobial performance under various production conditions. Synthetic compounds have established regulatory acceptance across many international markets, which supports their large-scale use in commercial food production. Their predictable activity and stability help manufacturers maintain consistent preservation outcomes while ensuring minimal influence on product characteristics when applied at appropriate levels.

The liquid antimicrobials segment held 39% share in 2025 and is anticipated to grow at a CAGR of 5.6% through 2035. These solutions are favored because they integrate easily into food processing systems and allow uniform distribution throughout product formulations. Their high solubility and dispersion efficiency enable accurate dosing and thorough blending, which helps maintain consistent antimicrobial effectiveness across entire production batches. Liquid antimicrobials also support streamlined processing operations because they can be incorporated efficiently into liquid or semi-liquid food matrices.

United States Food Antimicrobials Market held 84.8% share in 2025 and is projected to reach USD 1.3 billion by 2035, supported by strict regulatory frameworks governing food safety as well as strong consumer awareness regarding product quality and hygiene standards. The highly developed food manufacturing sector in the United States creates sustained demand for antimicrobial solutions that ensure stability and safety throughout production, packaging, and distribution stages.

Key companies operating in the Global Food Antimicrobials Market include Celanese, Corbion, DSM-Firmenich, Eastman, Galactic, International Flavors & Fragrances, Jungbunzlauer, Kalsec, Kerry Group, Mitsubishi Chemical, and Novonesis. Companies active in the Global Food Antimicrobials Market are strengthening their competitive position through several strategic initiatives focused on innovation, partnerships, and global expansion. Many manufacturers are increasing investments in research and development to create advanced antimicrobial formulations that align with evolving consumer preferences and regulatory standards. Businesses are also prioritizing the development of clean-label and naturally derived preservation solutions to address growing demand for transparent ingredient profiles. Strategic collaborations with food manufacturers and ingredient suppliers are helping companies expand product adoption and strengthen distribution networks. In addition, firms are enhancing production capabilities and optimizing supply chains to support rising global demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Form

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Natural antimicrobials

- 5.2.1 Organic acids

- 5.2.2 Bacteriocins

- 5.2.3 Essential oils & active compounds

- 5.2.4 Plant extracts & polyphenols

- 5.2.5 Enzymes

- 5.2.6 Chitosan & derivatives

- 5.2.7 Antimicrobial peptides

- 5.2.8 Microbial biopreservatives

- 5.2.9 Others

- 5.3 Nature-identical antimicrobials

- 5.3.1 Vanillin

- 5.3.2 Linalool

- 5.3.3 Coumarin

- 5.3.4 Others

- 5.4 Synthetic antimicrobials

- 5.4.1 Benzoates

- 5.4.2 Sorbates

- 5.4.3 Nitrites & nitrates

- 5.4.4 Sulfites

- 5.4.5 Propionates

- 5.4.6 Synthetic antioxidants (BHA, BHT, TBHQ, Propyl Gallate)

- 5.4.7 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Liquid

- 6.3 Powder

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Meat & poultry

- 7.2.1 Fresh meat products

- 7.2.2 Processed & cured meat

- 7.2.3 Poultry products

- 7.2.4 Ready-to-eat (RTE) meat products

- 7.2.5 Others

- 7.3 Bakery & confectionery

- 7.3.1 Bread & baked goods

- 7.3.2 Cakes & pastries

- 7.3.3 Confectionery products

- 7.3.4 Others

- 7.4 Dairy & frozen desserts

- 7.4.1 Fluid milk

- 7.4.2 Cheese products

- 7.4.3 Yogurt & fermented dairy

- 7.4.4 Ice cream & frozen desserts

- 7.4.5 Butter & cream

- 7.4.6 Others

- 7.5 Beverages

- 7.5.1 Fruit juices & nectars

- 7.5.2 Soft drinks & carbonated beverages

- 7.5.3 Alcoholic beverages

- 7.5.4 Others

- 7.6 Snacks

- 7.6.1 Savory snacks

- 7.6.2 Roasted nuts & peanut butter

- 7.6.3 Others

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Celanese

- 9.2 Corbion

- 9.3 DSM-Firmenich

- 9.4 Eastman

- 9.5 Galactic

- 9.6 International Flavors & Fragrances

- 9.7 Jungbunzlauer

- 9.8 Kalsec

- 9.9 Kerry Group

- 9.10 Mitsubishi Chemical

- 9.11 Novonesis