|

市場調查報告書

商品編碼

1998728

三相家用緊急發電機市場機會、成長要素、產業趨勢及預測(2026-2035 年)。Three Phase Home Standby Gensets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

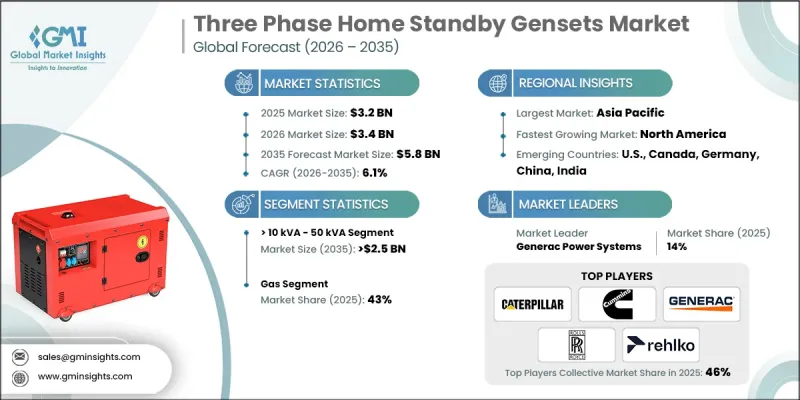

全球三相家用緊急發電機市場預計到 2025 年將價值 32 億美元,預計到 2035 年將以 6.1% 的複合年成長率成長至 58 億美元。

市場成長的促進因素包括:天氣相關災害的發生頻率和嚴重程度不斷增加、電力基礎設施老化以及電網日益脆弱。住宅和企業越來越重視可靠的緊急電源解決方案,以維持業務連續性並降低停電風險。快速的都市化、大規模房地產投資以及對不斷電系統)在基本家用電器、醫療設備和智慧家居技術方面的日益依賴,進一步推動了市場需求。地下電力系統在暴風雨和強降雨期間極易遭受洪水侵襲,凸顯了家用緊急發電機的重要性。極端天氣、氣候變遷相關的災害以及智慧家庭的日益普及,共同推動了該領域的持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 32億美元 |

| 預計金額 | 58億美元 |

| 複合年成長率 | 6.1% |

預計到2035年,功率範圍在10千伏安至50千伏安之間的三相家用緊急發電機市場規模將達到25億美元。這些發電機擴大用於為水泵、廚房電器和熱水系統等關鍵家用系統供電,在其他備用電源技術不足的情況下提供可靠的解決方案。該系列產品實用的容量和可靠的性能使其成為尋求應對頻繁停電的住宅的首選。

預計到2025年,燃氣動力設備市佔率將達到43%。這一成長主要得益於監管趨勢對設備使用壽命長、操作簡單和低碳排放的重視。天然氣供應充足以及燃氣發電機的環保優勢也進一步鞏固了市場前景。

預計2025年,美國三相家用緊急發電機市場規模將達9.776億美元。這一成長主要得益於家用電器使用量的增加、政府主導的住宅開發促進計劃以及智慧家居技術的日益普及。房地產市場的強勁成長以及消費者對無停電電力解決方案的偏好,正在推動該產品在全部區域的滲透率。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 原物料供應及採購分析

- 生產能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 監理情勢

- 成長潛力分析

- 價格趨勢分析(單位:美元)

- 按地區

- 額定功率

- 波特五力分析

- PESTEL 分析

- 三相家用緊急發電機的成本結構分析

- 新機會和趨勢

- 數位化和物聯網整合

- 未開發市場和應用領域的成長

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東

- 非洲

- 拉丁美洲

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依產量分類,2022-2035年

- 10千伏安或以下

- 10千伏安至50千伏安

- >50 kVA~100 kVA

- 超過100千伏安

第6章 市場規模與預測:依燃料類型分類,2022-2035年

- 柴油引擎

- 氣體

- 其他

第7章 市場規模及預測:依產品分類,2022-2035年

- 空冷式

- 水冷

第8章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 俄羅斯

- 英國

- 德國

- 法國

- 西班牙

- 奧地利

- 義大利

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 印尼

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 土耳其

- 伊朗

- 阿曼

- 非洲

- 埃及

- 奈及利亞

- 阿爾及利亞

- 南非

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

第9章:公司簡介

- Ashok Leyland

- Briggs and Stratton

- Caterpillar

- Champion Power Equipment

- Cummins

- Duromax Power Equipment

- Eaton

- Echo Group

- Generac Power Systems

- Gillette Generators

- HIMOINSA

- HIPOWER

- Kirloskar

- Mahindra Powerol

- Pinnacle Generators

- Powerica

- PR Industrial

- Rehlko

- Rolls-Royce

- Yamaha Motor

The Global Three Phase Home Standby Gensets Market was valued at USD 3.2 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 5.8 billion by 2035.

Market growth is driven by the rising frequency and severity of weather-related disruptions, aging power infrastructure, and the growing vulnerability of electricity grids. Homeowners and businesses are increasingly prioritizing reliable backup power solutions to maintain continuous operations and reduce risk during outages. Rapid urbanization, large-scale real estate investments, and the rising reliance on uninterrupted power for essential household appliances, medical devices, and smart home technologies are further intensifying market demand. Subterranean power systems, prone to flooding during storms and heavy rainfall, highlight the critical need for home standby generators. The combination of extreme weather events, climate-related disruptions, and the increasing adoption of connected homes is driving sustained growth in this segment.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.8 Billion |

| CAGR | 6.1% |

The >10 kVA to 50 kVA three-phase home standby gensets segment is expected to reach USD 2.5 billion by 2035. These units are increasingly used to power essential household systems such as well pumps, kitchen appliances, and hot water systems, providing a reliable solution where other backup technologies may fall short. The segment's practical capacity and dependable performance make it a preferred choice for homeowners seeking resilience against frequent power interruptions.

The gas-fueled segment accounted for 43% share in 2025. Its growth is supported by the long lifespan, ease of operation, and regulatory emphasis on lower carbon emissions. Widespread natural gas availability and the environmental advantages of gas-fueled gensets further strengthen the market outlook.

U.S. Three Phase Home Standby Gensets Market was valued at USD 977.6 million in 2025. Expansion is fueled by rising dependence on electrical appliances, government-backed initiatives promoting residential development, and increasing adoption of smart home technologies. Active growth in real estate and consumer preference for uninterrupted power solutions reinforce product penetration across the region.

Key players operating in the Global Three Phase Home Standby Gensets Market include Generac Power Systems, Caterpillar, Cummins, Rolls-Royce, Briggs and Stratton, Ashok Leyland, Pinnacle Generators, Powerica, Yamaha Motor, Mahindra Powerol, Kirloskar, Duromax Power Equipment, Rehlko, HIPOWER, HIMOINSA, Gillette Generators, Echo Group, PR Industrial, and Eaton. Companies in the Global Three Phase Home Standby Gensets Market employ several strategies to expand their market footprint. They invest in advanced, energy-efficient, and low-emission genset technologies to meet regulatory and consumer expectations. Manufacturers form strategic alliances with real estate developers and residential service providers to broaden distribution channels. Companies also focus on enhancing after-sales service, extended warranties, and digital monitoring features to improve customer satisfaction. Geographic expansion into high-growth urban and flood-prone areas, coupled with targeted marketing campaigns highlighting reliability, efficiency, and environmental benefits, strengthens their market positioning. Product portfolio diversification, including multiple fuel types and capacity options, ensures appeal across residential and commercial segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Power rating trends

- 2.1.3 Fuel trends

- 2.1.4 Product trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Price trend analysis (USD/Unit)

- 3.5.1 By region

- 3.5.2 By power rating

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Cost structure analysis of three phase home standby gensets

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.2.5 Africa

- 4.2.6 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 ≤ 10 kVA

- 5.3 > 10 kVA - 50 kVA

- 5.4 > 50 kVA - 100 kVA

- 5.5 > 100 kVA

Chapter 6 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Gas

- 6.4 Others

Chapter 7 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 Air cooled

- 7.3 Liquid cooled

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & '000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Russia

- 8.3.2 UK

- 8.3.3 Germany

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Austria

- 8.3.7 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Turkey

- 8.5.5 Iran

- 8.5.6 Oman

- 8.6 Africa

- 8.6.1 Egypt

- 8.6.2 Nigeria

- 8.6.3 Algeria

- 8.6.4 South Africa

- 8.7 Latin America

- 8.7.1 Brazil

- 8.7.2 Mexico

- 8.7.3 Argentina

Chapter 9 Company Profiles

- 9.1 Ashok Leyland

- 9.2 Briggs and Stratton

- 9.3 Caterpillar

- 9.4 Champion Power Equipment

- 9.5 Cummins

- 9.6 Duromax Power Equipment

- 9.7 Eaton

- 9.8 Echo Group

- 9.9 Generac Power Systems

- 9.10 Gillette Generators

- 9.11 HIMOINSA

- 9.12 HIPOWER

- 9.13 Kirloskar

- 9.14 Mahindra Powerol

- 9.15 Pinnacle Generators

- 9.16 Powerica

- 9.17 PR Industrial

- 9.18 Rehlko

- 9.19 Rolls-Royce

- 9.20 Yamaha Motor