|

市場調查報告書

商品編碼

1998726

汽車活塞銷市場機會、成長要素、產業趨勢分析及2026-2035年預測Automotive Piston Pin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

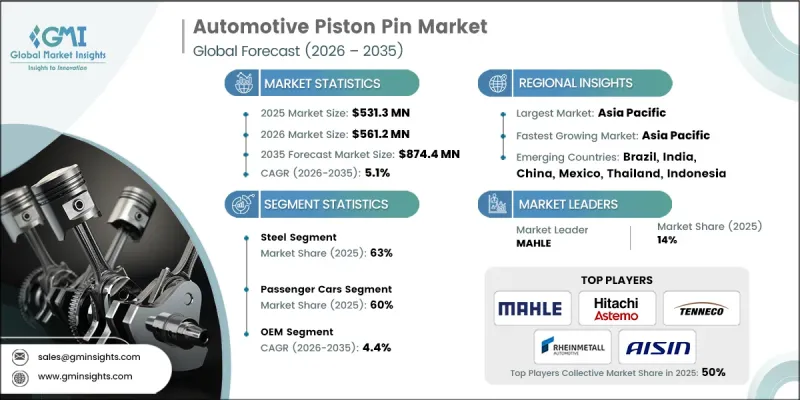

預計到 2025 年,全球汽車活塞銷市場價值將達到 5.313 億美元,年複合成長率為 5.1%,到 2035 年將達到 8.744 億美元。

活塞銷(也稱為活塞銷)是連接活塞和連桿的關鍵引擎零件,負責將燃燒動力傳遞至曲軸。受乘用車和商用車對引擎耐久性、燃油效率和性能提升的需求驅動,活塞銷市場持續擴張。現代活塞銷設計採用高性能合金鋼、類金剛石碳(DLC)塗層和精密加工技術,以承受高機械和熱負荷。冶金製程、表面處理和輕量化設計的創新已將傳統的實心活塞銷轉變為中空、塗層和超高強度類型,從而降低摩擦、提高耐磨性並支援更高的引擎轉速。全球汽車產量的成長、燃油效率高的引擎的普及、日益嚴格的排放氣體法規以及混合動力渦輪增壓動力傳動系統的發展是推動市場持續擴張的關鍵因素。商用車零件市場也為高品質活塞銷提供了穩定的需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 5.313億美元 |

| 預計金額 | 8.744億美元 |

| 複合年成長率 | 5.1% |

該市場涵蓋實心和空心活塞銷、塗層產品、輕質高強度鋼材以及精密加工的活塞銷,主要供應給原始設備製造商 (OEM) 和一級引擎零件供應商。技術進步正推動市場朝向中空和中空處理設計發展,以最大限度地減少摩擦、延長引擎壽命並承受高燃燒壓力。這些創新對於小型化和渦輪增壓引擎尤其重要,因為這些引擎的活塞銷必須承受更高的機械應力和熱應力。

預計到2025年,鋼鐵市場佔有率將達到63%,並預計在2026年至2035年間以4.5%的複合年成長率成長。鋼鐵憑藉其強度高、耐久性好、成本效益高以及成熟的製造程序,保持著市場主導地位。高碳鋼合金,例如SAE 8620和SAE 52100,經熱處理後抗張強度可超過1000兆帕,硬度可達58-62 HRC,從而確保了內燃機的可靠性。在商用車領域,由於耐久性和成本因素比輕量化更為重要,鋼製活塞銷仍然是首選。

預計到2025年,乘用車市佔率將達到60%,並在2035年之前以4.2%的複合年成長率成長。該細分市場包括總重低於6000磅的轎車、掀背車、SUV和跨界車。乘用車活塞銷的設計優先考慮輕量化材料、降低摩擦和性能最佳化,而非極致的耐久性,這反映了其15萬至20萬英里的典型使用壽命。鋁合金和先進塗層,特別是類鑽石碳(DLC)塗層,正被擴大採用,其中DLC塗層在高階市場的滲透率已超過50%,從而提高了耐磨性和性能。

預計到2025年,中國汽車活塞銷市場規模將達到375億美元,並在2026年至2035年間維持4.3%的複合年成長率。中國強大的汽車製造業基礎、完善的供應鏈管理以及電池生產和原料採購的垂直整合,正在推動成本降低並減少對海外供應商的依賴。乘用車和商用車產量的成長,以及對高性能內燃機和混合動力傳動系統零件的需求,正在推動該地區市場的持續成長。中國商用車產業,特別是支撐基礎設施建設和貨運物流的重型卡車,確保了對柴油引擎零件和活塞銷的持續需求。此外,區域製造商正在拓展細分市場,從而推動市場競爭和創新。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球汽車產量擴張和汽車保有量增加

- 節能輕量化引擎零件的需求日益成長。

- 汽車售後市場需求的成長是由車輛老化及其保養週期所驅動的。

- 塗佈技術(類鑽碳、物理氣相沉積)的進步

- 嚴格的排放法規正在推動引擎效率的提高。

- 產業潛在風險與挑戰

- 原物料成本上漲和特殊合金價格波動

- 向電動車的轉變正在降低對內燃機(ICE)零件的需求。

- 複雜的製造要求和品管挑戰

- 高性能應用中的設計約束和引腳畸變問題

- 市場機遇

- 先進複合材料及特殊合金材料的開發

- 在汽車生產不斷擴張的新興市場拓展業務。

- 混合動力傳動系統的日益普及推高了對內燃機(ICE)零件的需求。

- 業績成長和競爭激烈的細分市場對高級產品的需求。

- 透過數位化和智慧製造降低生產成本

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國環保署(EPA)溫室氣體法規第三階段與CAFE標準

- 加拿大—基於排放的法規結構

- 歐洲

- 德國—歐7排放氣體標準

- 英國-脫歐後的車輛類型認證

- 法國——脫碳藍圖

- 義大利-遵守低排放區規定

- 亞太地區

- 中國 - 中國 VI-b 和新興中國 VII 標準

- 印度BS-VI第二階段和Bharat第七階段過渡

- 日本 - 燃油效率標準(2030 年目標)

- 澳洲 - 燃油品質和 ADR 79/05 標準

- 拉丁美洲

- 墨西哥-NOM-194-SE-2021 和美墨加協定原產地規則

- 阿根廷-第24.449號法律及環境修正案

- 中東和非洲(MEA)

- 南非 - 道路交通法(1996 年)

- 沙烏地阿拉伯—2030願景下的交通運輸法律與交通運輸舉措

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢(基於初步調查)

- 價格分析

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 總擁有成本 (TCO) 分析

- 貿易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易走廊和關稅的影響

- 使用案例和成功案例

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- GenAI 各細分市場的應用案例與部署藍圖

- 風險、局限性和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能

- 運轉率和擴張計劃

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 關於碳足跡的考量

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依材料分類,2022-2035年

- 鋼

- 鋁合金

- 鈦合金

第6章 市場估算與預測:依塗料產業分類,2022-2035年

- 類金剛石碳(DLC)

- 物理氣相沉積(PVD)

- 其他

第7章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第8章 市場估算與預測:依燃料類型分類,2022-2035年

- 汽油引擎

- 柴油引擎

- 替代燃料引擎

第9章 市場估價與預測:依銷售管道分類,2022-2035年

- OEM

- 售後市場

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 瑞典

- 丹麥

- 波蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 以色列

第11章:公司簡介

- 世界公司

- Aisin Seiki

- Art Metal

- Burgess-Norton

- Elgin Industries

- Hitachi Astemo

- MAHLE

- Tenneco

- 當地公司

- Arias Pistons

- Bohai Piston

- Chuxiong Piston Pin

- CP-Carrillo

- JE Pistons

- Kolbenschmidt Pistons(Comitans Capital)

- Ming Shun Industrial

- Ross Racing Pistons

- Shriram Pistons &Rings

- 新興企業

- Art-Serina Piston

- Garima Global

- Hai Yen Industrial

- Power Industries

The Global Automotive Piston Pin Market was valued at USD 531.3 million in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 874.4 million by 2035.

Piston pins, also referred to as gudgeon pins, are critical engine components that link pistons to connecting rods, transferring combustion forces to the crankshaft. The market is increasingly driven by demand for higher engine durability, improved fuel efficiency, and enhanced performance in both passenger and commercial vehicles. Modern piston pin designs leverage high-performance alloy steels, diamond-like carbon (DLC) coatings, and precision machining to withstand high mechanical and thermal loads. Innovations in metallurgical processes, surface treatments, and lightweight design have transformed conventional solid pins into hollow, coated, and ultra-strong variants, reducing friction, boosting wear resistance, and supporting higher engine speeds. Rising global vehicle production, adoption of fuel-efficient engines, stringent emission standards, and growth in hybrid and turbocharged powertrains are major factors driving sustained market expansion. The commercial vehicle replacement segment also contributes to consistent demand for high-quality piston pins.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $531.3 Million |

| Forecast Value | $874.4 Million |

| CAGR | 5.1% |

The market comprises solid and hollow piston pins, coated variants, lightweight high-strength steel grades, and precision-finished pins supplied to OEMs and Tier 1 engine component manufacturers. Technological advances are shifting the market toward hollow and surface-treated designs, which minimize friction, extend engine life, and handle elevated combustion pressures. These innovations are especially relevant for downsized and turbocharged engines, where piston pins must sustain higher mechanical and thermal stresses.

The steel segment held a 63% share in 2025 and is expected to grow at a CAGR of 4.5% from 2026 to 2035. Steel retains market leadership due to its combination of strength, durability, cost efficiency, and established manufacturing processes. High-carbon steel alloys such as SAE 8620 and SAE 52100, after heat treatment, achieve tensile strengths exceeding 1,000 MPa and hardness levels of 58-62 HRC, ensuring reliability in internal combustion engines. Steel piston pins remain the preferred choice for commercial vehicles where durability and cost considerations outweigh weight reduction imperatives.

The passenger cars segment accounted for 60% share in 2025, growing at a CAGR of 4.2% through 2035. These vehicles include sedans, hatchbacks, SUVs, and crossovers under 6,000 pounds gross vehicle weight. Piston pins for passenger cars prioritize lightweight materials, friction reduction, and refinement rather than ultimate durability, reflecting typical service cycles of 150,000-200,000 miles. Aluminum alloys and advanced coatings, particularly DLC, are increasingly used, with DLC penetration exceeding 50% in premium segments, offering enhanced wear resistance and performance.

China Automotive Piston Pin Market accounted for USD 37.5 billion in 2025 and is forecasted to maintain a CAGR of 4.3% from 2026 to 2035. Its robust automotive manufacturing base, extensive supply chain control, and vertical integration of battery production and raw material sourcing reduce costs and reliance on international suppliers. Rising production of both passenger and commercial vehicles, combined with demand for high-performance internal combustion and hybrid powertrain components, fuels sustained growth in the region. China's commercial vehicle sector, particularly heavy-duty trucks supporting infrastructure development and freight logistics, ensures continuous demand for diesel engine components and piston pins. Regional manufacturers are also expanding into niche segments, increasing competition and innovation in the market.

Major players operating in the Global Automotive Piston Pin Market include Hitachi Astemo, Burgess-Norton, Kolbenschmidt Pistons, Aisin Seiki, Shriram Pistons & Rings, Art Metal, MAHLE, Elgin Industries, Bohai Piston, and Tenneco. Companies in the Global Automotive Piston Pin Market focus on strategies such as research and development of lightweight, hollow, and coated pins, integration of advanced alloy steels, and development of DLC and other surface treatments to enhance performance. Expanding production capacity and establishing localized manufacturing hubs in high-growth regions, particularly Asia-Pacific, helps reduce costs and improve supply chain reliability. Strategic collaborations with OEMs and Tier 1 engine manufacturers allow firms to integrate their components into new vehicle models early in the design process. Mergers, acquisitions, and partnerships also help companies expand technological capabilities and product portfolios, while aftermarket and replacement-focused strategies ensure recurring revenue streams. Additionally, marketing initiatives highlighting enhanced fuel efficiency, reduced wear, and engine longevity help strengthen brand recognition and market penetration.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Coating

- 2.2.4 Vehicle

- 2.2.5 Fuel

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing global automotive production and vehicle parc expansion

- 3.2.1.2 Increasing demand for fuel-efficient and lightweight engine components

- 3.2.1.3 Rising aftermarket demand driven by vehicle aging and maintenance cycles

- 3.2.1.4 Technological advancements in coating technologies (DLC, PVD)

- 3.2.1.5 Stringent emission regulations driving engine efficiency improvements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High raw material costs and price volatility of specialty alloys

- 3.2.2.2 Shift toward electric vehicles reducing ICE component demand

- 3.2.2.3 Complex manufacturing requirements and quality control challenges

- 3.2.2.4 Design constraints and pin distortion issues in high-performance applications

- 3.2.3 Market opportunities

- 3.2.3.1 Development of advanced composite and exotic alloy materials

- 3.2.3.2 Expansion in emerging markets with growing vehicle production

- 3.2.3.3 Increasing adoption of hybrid powertrains extending ICE component demand

- 3.2.3.4 Growing performance and racing segment requiring premium products

- 3.2.3.5 Digitalization and smart manufacturing reducing production costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- EPA GHG phase 3 & CAFE standards

- 3.4.1.2 Canada - Emissions-based regulatory framework

- 3.4.2 Europe

- 3.4.2.1 Germany- Euro 7 Emission Standards

- 3.4.2.2 UK- Post-brexit vehicle type approval

- 3.4.2.3 France- Decarbonization roadmap

- 3.4.2.4 Italy- Low-Emission zone compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China- China VI-b & Emerging China VII standards

- 3.4.3.2 India- BS-VI Stage II & bharat stage VII transition

- 3.4.3.3 Japan- Fuel efficiency standards (2030 Targets)

- 3.4.3.4 Australia- Fuel quality & ADR 79/05 standards

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM-194-SE-2021 & USMCA rules of origin

- 3.4.4.2 Argentina- Law 24.449 & environmental amendments

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent landscape (Driven by Primary Research)

- 3.9 Pricing analysis

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9.3 Total cost of ownership (TCO) analysis

- 3.10 Trade data analysis (Driven by Paid Database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Use cases & success stories

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Steel

- 5.3 Aluminum alloy

- 5.4 Titanium alloy

Chapter 6 Market Estimates & Forecast, By Coating, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Diamond-Like Carbon (DLC)

- 6.3 Physical Vapor Deposition (PVD)

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Medium commercial vehicles (MCVs)

- 7.3.3 Heavy commercial vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Gasoline engines

- 8.3 Diesel engines

- 8.4 Alternative fuel engines

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aisin Seiki

- 11.1.2 Art Metal

- 11.1.3 Burgess-Norton

- 11.1.4 Elgin Industries

- 11.1.5 Hitachi Astemo

- 11.1.6 MAHLE

- 11.1.7 Tenneco

- 11.2 Regional Players

- 11.2.1 Arias Pistons

- 11.2.2 Bohai Piston

- 11.2.3 Chuxiong Piston Pin

- 11.2.4 CP-Carrillo

- 11.2.5 JE Pistons

- 11.2.6 Kolbenschmidt Pistons (Comitans Capital)

- 11.2.7 Ming Shun Industrial

- 11.2.8 Ross Racing Pistons

- 11.2.9 Shriram Pistons & Rings

- 11.3 Emerging Players

- 11.3.1 Art-Serina Piston

- 11.3.2 Garima Global

- 11.3.3 Hai Yen Industrial

- 11.3.4 Power Industries

2026年全球汽車活塞市場報告2026年全球活塞市場報告

2026年全球汽車活塞市場報告2026年全球活塞市場報告 汽車活塞系統市場:按引擎類型、材質、活塞設計、車輛類型和分銷管道分類-2026-2032年全球預測

汽車活塞系統市場:按引擎類型、材質、活塞設計、車輛類型和分銷管道分類-2026-2032年全球預測 汽車活塞市場報告:按材料類型、車輛類型、活塞塗層類型、活塞類型、分銷管道和地區分類,2026-2034年2026年全球鋼活塞市場報告

汽車活塞市場報告:按材料類型、車輛類型、活塞塗層類型、活塞類型、分銷管道和地區分類,2026-2034年2026年全球鋼活塞市場報告 活塞閥市場-2026年至2031年預測

活塞閥市場-2026年至2031年預測 氣動活塞振動器市場規模、佔有率、成長分析(按產品類型、安裝類型、工作壓力、尺寸、功能、應用、最終用戶產業和地區分類)-2026-2033年產業預測

氣動活塞振動器市場規模、佔有率、成長分析(按產品類型、安裝類型、工作壓力、尺寸、功能、應用、最終用戶產業和地區分類)-2026-2033年產業預測 汽車活塞市場規模、佔有率和成長分析(按組件、車輛類型、材料、塗層、燃料類型和地區分類)—產業預測,2026-2033年

汽車活塞市場規模、佔有率和成長分析(按組件、車輛類型、材料、塗層、燃料類型和地區分類)—產業預測,2026-2033年 汽車活塞引擎系統市場預測至2032年:按組件、引擎類型、車輛類型、燃料類型、銷售管道和地區進行的全球分析

汽車活塞引擎系統市場預測至2032年:按組件、引擎類型、車輛類型、燃料類型、銷售管道和地區進行的全球分析 全球汽車活塞市場(至 2035 年)按形狀(平頂、碗狀、圓頂)、材質(鋼、鋁)、塗層(隔熱層、乾膜、脫油)、零件(銷、環、頭)、燃料類型、車輛類型、售後零件和地區分類

全球汽車活塞市場(至 2035 年)按形狀(平頂、碗狀、圓頂)、材質(鋼、鋁)、塗層(隔熱層、乾膜、脫油)、零件(銷、環、頭)、燃料類型、車輛類型、售後零件和地區分類