|

市場調查報告書

商品編碼

1998718

BTK抑制劑市場機會、成長要素、產業趨勢分析及2026-2035年預測BTK Inhibitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

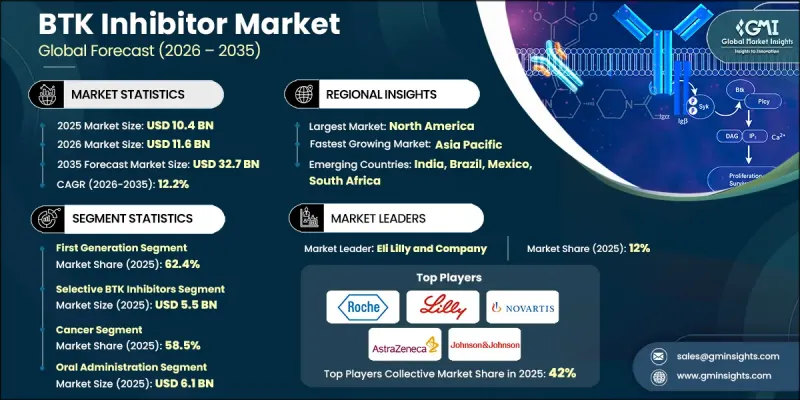

全球 BTK 抑制劑市場預計到 2025 年將價值 104 億美元,預計到 2035 年將達到 327 億美元,年複合成長率為 12.2%。

癌症和自體免疫疾病在全球日益加重,以及標靶治療研發的顯著進展,都推動了BTK抑制劑的持續成長。藥物研發正日益轉向精準標靶疾病進展相關分子路徑的治療方法,進而提升了BTK抑制劑的臨床意義。個人化醫療方法的日益普及,進一步推動了針對特定基因突變、基於生物標記的治療方法以及最佳化給藥策略的研發。此外,藥物研發領域的持續創新,也使得能夠開發出可克服抗藥性並改善治療效果的新一代BTK抑制劑。 BTK抑制劑透過抑制布魯頓蛋白酪氨酸激酶( BTK)發揮作用,BTK是一種在調節免疫系統中B細胞存活和活性方面起著核心作用的酵素。透過抑制異常的B細胞訊號傳導,這些治療方法有助於延緩多種血液系統疾病和免疫相關疾病的進展。隨著時間的推移,BTK抑制劑已成為現代標標靶治療策略的關鍵組成部分,顯著影響多種惡性腫瘤和免疫系統疾病的治療通訊協定。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 104億美元 |

| 預測金額 | 327億美元 |

| 複合年成長率 | 12.2% |

第一代BTK抑制劑市場預計到2025年將達到65億美元,佔市場佔有率的62.4%。早期BTK抑制劑療法在治療多種B細胞相關疾病方面展現出顯著的臨床療效。它們的引入顯著改善了治療效果,延緩了疾病進展,延長了患者的存活期。第一代BTK抑制劑得以廣泛應用的另一個原因是其便捷的口服給藥方式,與傳統的靜脈注射療法相比,這種方式創傷較小。口服治療方案提高了患者的舒適度,簡化了長期疾病管理,從而提高了患者的治療遵從率。此外,這些治療方法透過特異性靶向布魯頓蛋白酪氨酸激酶(B細胞受體訊號通路中的關鍵酶)發揮作用,有助於減輕傳統化療常見的許多副作用。

預計到2025年,選擇性BTK抑制劑市佔率將達到52.5%,市場規模將達55億美元。與傳統治療方法相比,這些治療方法旨在更精準地靶向布魯頓蛋白酪氨酸激酶。這種更高的特異性使藥物能夠更有效地作用於目標分子通路,同時減少與無關激酶的相互作用。因此,脫靶效應的風險得以降低。選擇性BTK抑制劑的另一個優點在於其良好的安全性,這對於需要長期治療的患者或有需要更謹慎管理的既往疾病的患者尤其重要。高選擇性治療方法的開發反映了整個行業向精準醫療和更精細化治療策略發展的趨勢。

預計到2025年,美國BTK抑制劑市場規模將達到38億美元,這得益於成熟的藥物研發生態系統和對先進標靶治療的強勁需求。美國癌症發生率的持續上升,使得能夠改善治療效果的標靶治療方案的需求顯著成長。美國食品藥物管理局(FDA)的法律規範也對BTK抑制劑市場的發展起到了至關重要的作用,其對藥物的安全性、有效性和品質制定了嚴格的核准標準。這些監管要求激勵製藥公司開發更先進的治療方法,以滿足不斷變化的臨床需求,同時確保病患安全。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 癌症和自體免疫疾病發生率增加

- 標靶治療的進展

- 持續的研究與開發

- 人們越來越關注個人化醫療

- 產業潛在風險與挑戰

- BTK抑制劑高成本

- 嚴格的法規環境

- 市場機遇

- 新興市場正在發展醫療衛生基礎設施。

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 未來市場趨勢

- 管道分析(基於初步調查)

- 2025年價格分析

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 第一代

- 第二代

第6章 市場估計與預測:依藥物類型分類,2022-2035年

- 選擇性BTK抑制劑

- 非選擇性BTK抑制劑

- 雙重BTK抑制劑

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 癌症

- 慢性淋巴性白血病(CLL)

- 濾泡性淋巴瘤

- 套細胞淋巴瘤

- 周邊區域淋巴瘤

- 小淋巴球淋巴瘤(SLL)

- 華氏巨球蛋白血症

- 其他選擇性B細胞惡性腫瘤

- 自體免疫疾病

- 全身性紅斑性狼瘡(SLE)

- 類風濕性關節炎(RA)

- 多發性硬化症(MS)

- 免疫性血小板減少性疾病(ITP)

- 發炎性疾病

- 發炎性腸道疾病(IBD)

- 氣喘和過敏性疾病

- IgG4相關疾病

- 血管炎

- 其他用途

第8章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 靜脈注射

- 皮下注射

第9章 市場估價與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第11章:公司簡介

- Amgen

- AstraZeneca

- Agilent Technologies

- BristolMyers Squibb

- Celgene

- Biogen

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd

- Gilead Sciences

- Johnson and Johnson

- Incyte

- Merck and Co

- Novartis

- Sanofi

- Takeda Pharmaceutical

The Global BTK Inhibitor Market was valued at USD 10.4 billion in 2025 and is estimated to grow at a CAGR of 12.2% to reach USD 32.7 billion by 2035.

The consistent growth is supported by the increasing burden of cancer and autoimmune disorders worldwide, along with notable progress in targeted drug development. Pharmaceutical research has increasingly shifted toward therapies designed to precisely target molecular pathways associated with disease progression, which has elevated the clinical relevance of BTK inhibitors. The rising adoption of personalized medicine approaches is further encouraging the development of therapies tailored to specific genetic mutations, biomarker-guided treatment methods, and optimized dosing strategies. In addition, continued innovation in drug discovery is enabling the development of next-generation BTK inhibitors capable of addressing treatment resistance and improving therapeutic outcomes. BTK inhibitors function by blocking Bruton's tyrosine kinase, an enzyme that plays a central role in regulating the survival and activity of B-cells within the immune system. By suppressing abnormal B-cell signaling, these therapies help control disease progression in several hematological conditions and immune-related disorders. Over time, BTK inhibitors have become an important component of modern targeted therapy strategies, significantly influencing treatment protocols for multiple malignancies and immune system disorders.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.4 Billion |

| Forecast Value | $32.7 Billion |

| CAGR | 12.2% |

The first-generation segment reached USD 6.5 billion in 2025 and held 62.4% share. Early BTK inhibitor therapies demonstrated substantial clinical effectiveness in treating several B-cell-related conditions. Their adoption significantly improved treatment outcomes by slowing disease progression and extending patient survival. Another factor supporting the widespread use of first-generation BTK inhibitors is their convenient oral administration, which offers a less invasive alternative to traditional intravenous therapies. Oral treatment options improve patient comfort and simplify long-term disease management, leading to better treatment adherence and higher compliance rates. These therapies also work by specifically targeting Bruton's tyrosine kinase, an essential enzyme involved in B-cell receptor signaling pathways, which helps reduce many of the adverse effects often associated with conventional chemotherapy approaches.

The selective BTK inhibitors segment accounted for 52.5% share and generated USD 5.5 billion in 2025. These therapies are designed to target Bruton's tyrosine kinase with a higher degree of precision compared with earlier treatment approaches. Their improved specificity allows the drugs to focus more effectively on the intended molecular pathway while limiting interaction with unrelated kinases. As a result, the risk of off-target biological effects is reduced. Another advantage of selective BTK inhibitors is their favorable safety profile, particularly for patients who require long-term therapy or have existing health conditions that demand more carefully managed treatment options. The development of highly selective therapies reflects the broader industry trend toward precision medicine and more refined therapeutic strategies.

United States BTK Inhibitor Market was valued at USD 3.8 billion in 2025, supported by a well-established pharmaceutical research ecosystem and a strong demand for advanced targeted therapies. Increasing cancer prevalence in the United States continues to generate significant demand for targeted therapeutic solutions capable of improving treatment effectiveness. Regulatory oversight from the U.S. Food and Drug Administration has also played an important role in shaping the BTK inhibitor landscape by maintaining strict approval standards for safety, performance, and drug quality. These regulatory requirements encourage pharmaceutical companies to develop more advanced therapies that meet evolving clinical expectations while ensuring patient safety.

Key participants active in the Global BTK Inhibitor Market include Novartis, Bristol Myers Squibb, Johnson & Johnson, Amgen, AstraZeneca, Merck & Co., Sanofi, Takeda Pharmaceutical, F. Hoffmann-La Roche Ltd, Gilead Sciences, Eli Lilly and Company, Incyte, Biogen, Celgene, and Agilent Technologies. Companies operating in the BTK Inhibitor Market are implementing multiple strategic initiatives to strengthen their competitive positioning. Leading pharmaceutical firms are prioritizing extensive research and development investments to discover improved BTK inhibitor formulations with greater selectivity and enhanced therapeutic performance. Strategic collaborations with biotechnology companies, academic institutions, and clinical research organizations are also being pursued to accelerate drug development and clinical trial programs. Many companies are expanding their oncology and immunology pipelines through acquisitions, licensing agreements, and technology partnerships that support innovation in targeted therapies. In addition, firms are strengthening regulatory approval strategies and increasing global commercialization capabilities to broaden their geographic reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.2 Research transparency addendum

- 1.7.3 Source attribution framework

- 1.7.4 Quality assurance metrics

- 1.7.1 Quantified market impact analysis

- 1.8 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Drug type trends

- 2.2.4 Application trends

- 2.2.5 Route of administration trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancers and autoimmune diseases

- 3.2.1.2 Advancements in targeted therapies

- 3.2.1.3 Ongoing research and development

- 3.2.1.4 Increasing focus on personalized medicine

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of BTK inhibitors

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Rising healthcare infrastructure in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Pipeline analysis (Driven by Primary Research)

- 3.7 Pricing analysis, 2025

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 First generation

- 5.3 Second generation

Chapter 6 Market Estimates and Forecast, By Drug Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Selective BTK inhibitors

- 6.3 Non-selective BTK inhibitors

- 6.4 Dual BTK inhibitors

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Cancer

- 7.2.1 Chronic lymphocytic leukemia (CLL)

- 7.2.2 Follicular lymphoma

- 7.2.3 Mantle cell lymphoma

- 7.2.4 Marginal zone lymphoma

- 7.2.5 Small lymphocytic lymphoma (SLL)

- 7.2.6 Waldenstrom macroglobulinemia

- 7.2.7 Other selective B cell malignancies

- 7.3 Autoimmune diseases

- 7.3.1 Systemic lupus erythematosus (SLE)

- 7.3.2 Rheumatoid arthritis (RA)

- 7.3.3 Multiple sclerosis (MS)

- 7.3.4 Immune thrombocytopenia (ITP)

- 7.4 Inflammatory disorders

- 7.4.1 Inflammatory bowel disease (IBD)

- 7.4.2 Asthma and allergic diseases

- 7.4.3 IgG4-Related diseases

- 7.4.4 Vasculitis

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Oral administration

- 8.3 Intravenous administration

- 8.4 Subcutaneous administration

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacy

- 9.3 Retail pharmacy

- 9.4 Online pharmacy

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amgen

- 11.2 AstraZeneca

- 11.3 Agilent Technologies

- 11.4 BristolMyers Squibb

- 11.5 Celgene

- 11.6 Biogen

- 11.7 Eli Lilly and Company

- 11.8 F. Hoffmann-La Roche Ltd

- 11.9 Gilead Sciences

- 11.10 Johnson and Johnson

- 11.11 Incyte

- 11.12 Merck and Co

- 11.13 Novartis

- 11.14 Sanofi

- 11.15 Takeda Pharmaceutical