|

市場調查報告書

商品編碼

1998714

法蘭市場機會、成長要素、產業趨勢分析及2026-2035年預測。Flanges Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

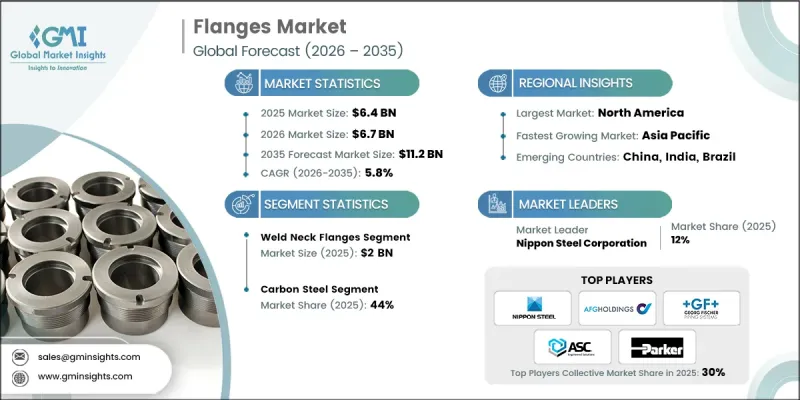

預計到 2025 年,全球法蘭市場價值將達到 64 億美元,並預計以 5.8% 的複合年成長率成長,到 2035 年達到 112 億美元。

法蘭在工業基礎設施中扮演著至關重要的角色,它們是連接流體和氣體輸送系統中的管道、閥門、泵浦和其他設備的關鍵機械部件。儘管結構簡單,法蘭卻發揮著至關重要的作用,例如保持管道對齊、確保結構強度以及方便維護。在依賴管道的行業中,能夠在各種壓力、溫度和環境條件下可靠運作的連接系統至關重要,這使得法蘭的需求與全球工業活動趨勢密切相關。終端用戶通常優先考慮能夠提供耐用、高性能法蘭的製造商,這些法蘭即使在惡劣環境下也能可靠運作。為了滿足不斷變化的行業需求,製造商正不斷改進生產技術、提高材料品質並擴展產品線。他們也致力於透過採用永續的生產方式和實現原料來源多元化來加強供應鏈。此外,新興經濟體工業活動的擴張也為法蘭製造商創造了新的機遇,並促進了全球市場的整體成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 64億美元 |

| 預測金額 | 112億美元 |

| 複合年成長率 | 5.8% |

預計到2025年,焊接頸法蘭市場規模將達20億美元。其優點在於卓越的機械強度、耐高壓性和高抗疲勞性。長錐形輪轂設計確保管道與法蘭之間應力分佈均勻,最大限度地減少焊接接頭處的應力集中。這種結構優勢使得焊接頸法蘭適用於在高壓、高溫或波動載荷下運作的嚴苛管道系統。由於其可靠性和耐久性,這些法蘭廣泛應用於對接頭完整性和運行安全性要求極高的關鍵工業管道網路。與其他類型的法蘭相比,焊接頸法蘭能夠提供更牢固、更可靠的連接,尤其適用於大直徑或厚壁管道。

截至2025年,碳鋼法蘭佔了44%的市場。其強大的市場地位主要歸功於成本績效和均衡的機械性能。與不銹鋼和鎳合金法蘭相比,碳鋼兼具耐用性、強度和經濟性。由於成本低廉,碳鋼仍然是需要大量法蘭的大規模工業計劃在預算控制方面的首選材料。在工業領域,碳鋼法蘭通常用於低至中等壓力和溫度條件下運作的管道系統,因此在多個工業領域中廣泛應用。

美國法蘭市場佔83%的市場佔有率,預計2025年市場規模將達到14億美元。該地區市場受益於成熟的工業基礎、嚴格的監管標準以及對流程工業和能源基礎設施的持續投資。與能源生產、管道擴建和設施現代化相關的持續活動,都推動了對法蘭的持續需求。此外,工業和市政系統中老化的基礎設施也帶來了對維護、維修和更換的穩定需求。嚴格遵守技術標準,促進了高品質鍛造法蘭和合金法蘭的使用,這些法蘭即使在嚴苛的運作條件下也能可靠運作。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 能源和流程工業的擴張

- 基礎設施和工業建設的成長

- 老舊資產的更新與維護

- 產業潛在風險與挑戰

- 原物料價格波動

- 嚴格的規章制度和品質合規性

- 機會

- 能源轉型和氫能基礎設施的成長

- 對高規格和客製化法蘭的需求不斷成長

- 促進因素

- 成長潛力分析

- 關鍵市場趨勢與顛覆性因素

- 未來市場趨勢

- 風險及風險緩解分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監理情勢

- 標準和合規要求

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 焊接頸法蘭

- 滑套式法蘭

- 盲板

- 承插焊法蘭

- 搭接法蘭

- 螺紋法蘭

- 其他

第6章 市場估計與預測:依壓力與溫度分類,2022-2035年

- 低的

- 中等的

- 高的

- 極端

第7章 市場估計與預測:依材料分類,2022-2035年

- 不銹鋼

- 合金鋼

- 鎳合金

- 碳鋼

- 其他

第8章 市場估算與預測:依製造流程分類,2022-2035年

- 鍛造

- 鑄件

- 加工產品

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 石油和天然氣

- 化學/石油化學加工

- 發電

- 用水和污水處理

- 紙漿和造紙

- 製藥

- 食品/飲料加工

- 採礦和金屬

- 一般製造業

- 其他

第10章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- Nippon Steel Corporation

- Georg Fischer(GF Piping Systems)

- Parker Hannifin

- AFG Holdings(Ameriforge)

- ASC Engineered Solutions

- Alleima

- Viraj Profiles Pvt. Ltd.

- Texas Flange

- Bonney Forge

- Metalfar SpA

- Flanschenwerk Bebitz GmbH

- Victaulic

- General Flange &Forge LLC

- Coastal Flange

- JFE STEEL CORPORATION

The Global Flanges Market was valued at USD 6.4 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 11.2 billion by 2035.

Flanges play a critical role in industrial infrastructure as essential mechanical components used to connect pipes, valves, pumps, and other equipment within fluid and gas transport systems. Although simple in structure, they provide vital functions such as maintaining pipeline alignment, ensuring structural strength, and enabling easy maintenance access. The demand for flanges closely follows the pace of industrial activity worldwide, as sectors relying on pipelines require reliable connection systems capable of operating under varying pressure, temperature, and environmental conditions. End users often prioritize suppliers that can deliver durable, high-performance flanges capable of functioning consistently in demanding environments. In response, manufacturers are increasingly refining production techniques, improving material quality, and expanding product portfolios to meet evolving industry requirements. Efforts are also being made to incorporate sustainable manufacturing practices and diversify raw material sourcing to strengthen supply chains. In addition, expanding industrial activity in emerging economies is creating new opportunities for flange manufacturers, contributing to the overall expansion of the global market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.4 Billion |

| Forecast Value | $11.2 Billion |

| CAGR | 5.8% |

The weld neck flanges segment accounted for USD 2 billion in 2025. Their dominance is attributed to their superior mechanical strength, ability to handle high pressure, and strong resistance to fatigue. The long tapered hub design distributes stress evenly between the pipe and the flange, minimizing stress concentration at welded joints. This structural advantage makes weld neck flanges suitable for demanding pipeline systems that operate under high pressure, high temperature, or fluctuating loads. Because of their reliability and durability, these flanges are widely used in critical industrial pipeline networks where joint integrity and operational safety are essential. Compared with other flange types, weld neck variants deliver stronger and more dependable connections, particularly in pipelines with large diameters or thicker pipe walls.

The carbon steel flanges segment held 44% share in 2025. Their strong presence is mainly due to their cost-effectiveness and balanced mechanical properties. Carbon steel offers a practical combination of durability, strength, and affordability compared to stainless steel or nickel alloy alternatives. Because of its lower cost, carbon steel remains the preferred material for large-scale industrial projects that require high volumes of flanges while maintaining budget efficiency. Industries commonly rely on carbon steel flanges for piping systems operating under low to moderate pressure and temperature conditions, making them widely used across multiple industrial sectors.

United States Flanges Market held 83% share, generating USD 1.4 billion in 2025. The regional market benefits from a well-established industrial base, strict regulatory standards, and continuous investments in process industries and energy infrastructure. Ongoing activity related to energy production, pipeline expansion, and facility modernization contributes to sustained demand for flanges. Additionally, aging infrastructure across industrial and municipal systems creates steady maintenance, repair, and replacement requirements. Compliance with stringent technical standards encourages the use of high-quality forged and alloy flanges capable of performing reliably in demanding operational environments.

Prominent companies operating in the Global Flanges Market include Nippon Steel Corporation, Parker Hannifin, Georg Fischer (GF Piping Systems), Alleima, AFG Holdings (Ameriforge), ASC Engineered Solutions, Viraj Profiles Pvt. Ltd., Texas Flange, Bonney Forge, Metalfar S.p.A., Flanschenwerk Bebitz GmbH, Victaulic, General Flange & Forge LLC, Coastal Flange, and JFE Steel Corporation. Companies in the Flanges Market strengthen their competitive position through continuous investment in advanced manufacturing technologies and material innovation. Many manufacturers focus on improving product durability, corrosion resistance, and pressure tolerance to meet strict industrial requirements. Strategic partnerships with engineering contractors, industrial operators, and distributors help expand market reach and secure long-term supply agreements. Firms also enhance their supply chains to ensure consistent raw material availability and efficient production. Geographic expansion into emerging industrial markets further supports revenue growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 regional

- 2.2.2 product type

- 2.2.3 pressure temperature

- 2.2.4 material

- 2.2.5 manufacturing process

- 2.2.6 end use sector

- 2.2.7 distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of energy and process industries

- 3.2.1.2 Growth in infrastructure and industrial construction

- 3.2.1.3 Replacement and maintenance of aging assets

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Volatility in raw material prices

- 3.2.2.2 Stringent regulatory and quality compliance

- 3.2.3 Opportunities

- 3.2.3.1 Growth of energy transition and hydrogen infrastructure

- 3.2.3.2 Increasing demand for high-specification and custom flanges

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and Disruptions

- 3.5 Future market trends

- 3.6 Risk and mitigation Analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 by product type

- 3.9 Regulatory landscape

- 3.9.1 Standards and compliance requirement

- 3.9.2 Certification standards

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Weld neck flanges

- 5.3 Slip-on flanges

- 5.4 Blind flanges

- 5.5 Socket weld flanges

- 5.6 Lap joint flanges

- 5.7 Threaded flanges

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Pressure Temperature, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

- 6.5 Extreme

Chapter 7 Market Estimates & Forecast, By Material, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Stainless steel

- 7.3 Alloy steel

- 7.4 Nickel alloy

- 7.5 Carbon steel

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Manufacturing Process, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Forged

- 8.3 Cast

- 8.4 Fabricated

Chapter 9 Market Estimates & Forecast, By End User, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Oil & gas

- 9.3 Chemical & petrochemical processing

- 9.4 Power generation

- 9.5 Water & wastewater treatment

- 9.6 Pulp & paper

- 9.7 Pharmaceuticals

- 9.8 Food & beverage processing

- 9.9 Mining & metals

- 9.10 General manufacturing

- 9.11 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Argentina

- 11.5.3 Mexico

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Nippon Steel Corporation

- 12.2 Georg Fischer (GF Piping Systems)

- 12.3 Parker Hannifin

- 12.4 AFG Holdings (Ameriforge)

- 12.5 ASC Engineered Solutions

- 12.6 Alleima

- 12.7 Viraj Profiles Pvt. Ltd.

- 12.8 Texas Flange

- 12.9 Bonney Forge

- 12.10 Metalfar S.p.A.

- 12.11 Flanschenwerk Bebitz GmbH

- 12.12 Victaulic

- 12.13 General Flange & Forge LLC

- 12.14 Coastal Flange

- 12.15 JFE STEEL CORPORATION

眼鏡法蘭市場 - 全球預測,2026-2032年

眼鏡法蘭市場 - 全球預測,2026-2032年 法蘭市場規模及預測(2021-2034年),全球及區域佔有率、趨勢及成長機會分析報告:按類型、材料、產業及地區分類

法蘭市場規模及預測(2021-2034年),全球及區域佔有率、趨勢及成長機會分析報告:按類型、材料、產業及地區分類 盲板法蘭市場規模及預測(2021-2034年),全球及區域佔有率、趨勢及成長機會分析報告:按材料、產業及地區分類

盲板法蘭市場規模及預測(2021-2034年),全球及區域佔有率、趨勢及成長機會分析報告:按材料、產業及地區分類 眼鏡法蘭市場規模、佔有率和成長分析:按材料、尺寸、應用、最終用途、通路和地區分類-2026-2033年產業預測

眼鏡法蘭市場規模、佔有率和成長分析:按材料、尺寸、應用、最終用途、通路和地區分類-2026-2033年產業預測 滑套法蘭市場規模及預測(2021-2034 年)、全球及區域市場佔有率、趨勢及成長機會分析報告:依材料、產業及地區分類。法蘭市場:按類型、材質、製造流程、尺寸和最終用戶分類-2026-2032年全球市場預測

滑套法蘭市場規模及預測(2021-2034 年)、全球及區域市場佔有率、趨勢及成長機會分析報告:依材料、產業及地區分類。法蘭市場:按類型、材質、製造流程、尺寸和最終用戶分類-2026-2032年全球市場預測 法蘭市場:按類型、材質、最終用途行業和地區分類風力渦輪機法蘭市場:按產品類型、渦輪機容量、材料、連接方式、塗層、設計、應用、終端用戶分類,全球預測,2026-2032年

法蘭市場:按類型、材質、最終用途行業和地區分類風力渦輪機法蘭市場:按產品類型、渦輪機容量、材料、連接方式、塗層、設計、應用、終端用戶分類,全球預測,2026-2032年 2026年全球法蘭市場報告

2026年全球法蘭市場報告 法蘭市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、材料、最終用戶、地區和競爭格局分類),2021-2031年

法蘭市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、材料、最終用戶、地區和競爭格局分類),2021-2031年