|

市場調查報告書

商品編碼

1998712

獸醫心電圖系統市場機會、成長要素、產業趨勢分析及2026-2035年預測。Veterinary ECG Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

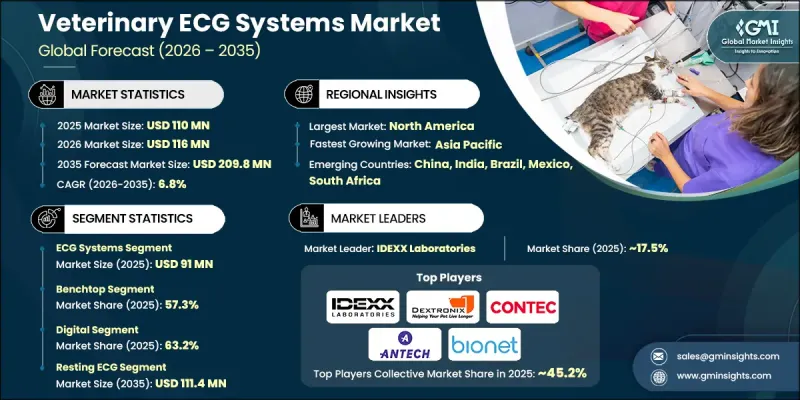

全球獸醫心電圖系統市場預計到 2025 年將達到 1.1 億美元,預計到 2035 年將以 6.8% 的複合年成長率成長至 2.098 億美元。

人們對動物健康的日益關注以及獸醫護理支出的不斷成長是推動市場成長的主要因素。獸用心電圖系統是一種非侵入性診斷設備,旨在記錄和分析心臟的電活動,使獸醫能夠評估心臟功能並識別異常情況。隨著獸醫基礎設施的擴展以及專科診所和醫院數量的持續成長,對先進診斷技術的需求顯著增加。獸醫技術的進步也提高了心電圖監測設備的準確性和易用性。數位平台、無線連接和小型診斷工具的引入正在改變獸醫實踐中評估心臟功能的方式。同時,寵物保險的普及和獲得專業獸醫服務的便利性也促進了最新診斷設備的應用。這些協同發展為全球獸用心電圖系統市場的持續擴張創造了有利條件。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1.1億美元 |

| 預計金額 | 2.098億美元 |

| 複合年成長率 | 6.8% |

推動獸用心電圖系統市場成長的另一個關鍵因素是動物心臟病發生率的不斷上升。影響動物的各種心臟相關疾病需要及時診斷和持續監測,以確保有效治療和長期管理。獸醫專業人員越來越依賴心電圖監測技術,因為它提供了一種準確且非侵入性的方法來評估心率和電活動。隨著獸醫院和診所越來越重視預防醫學和疾病早期檢測,對可靠的心臟診斷設備的需求也穩定成長。獸用心電圖系統在識別心臟功能異常方面發揮著至關重要的作用,並使臨床醫生能夠長期監測患者的病情。

預計2025年,心電圖(ECG)系統市場規模將達到9,100萬美元。這些系統是監測動物心率模式和檢測心律不整的基礎診斷解決方案。由於其在識別心血管疾病方面發揮重要作用,這些系統已成為獸醫診斷程序的重要組成部分。老年寵物複雜心臟併發症的檢出率不斷提高,推動了這些系統在動物醫院和專科診所的廣泛應用。此外,飼主對潛在心臟健康問題的日益關注也促進了對先進診斷檢測的需求。攜帶式和無線心電圖解決方案的日益普及,使獸醫能夠在臨床環境和獸醫護理領域進行即時心臟監測,進一步推動了該細分市場的擴張。

根據產品組成,預計到2025年,桌上型心電圖儀將佔據57.3%的市場。由於其可靠且精細的心電圖監測功能,桌上型心電圖儀在獸醫領域持續廣泛應用。這些系統能夠同時記錄多個心電圖通道,使獸醫能夠對各種動物進行全面的心臟評估。它們提供極其精準的診斷數據的能力,對於需要進行詳細心臟分析的動物醫院和診斷中心而言尤其重要。桌上型心電圖儀通常與其他診斷技術和資訊管理系統整合,從而簡化臨床工作流程並改善資料管理。這種整合提高了動物醫療機構的效率,支持更精準的醫療決策,最終改善患者預後並維持對這些系統的持續需求。

預計2025年,北美獸用心電圖(ECG)系統市佔率將達到37.9%。該地區的主導地位得益於其完善的獸醫基礎設施和高水準的動物保健服務支出。人們對動物健康的日益重視以及先進獸醫診斷技術的廣泛應用,進一步推動了市場成長。此外,專業獸醫服務和先進治療設施的普及也帶動了對先進心電圖監測解決方案的需求。同時,該地區眾多行業相關人員的存在以及持續的技術創新,也促進了市場發展,使獸醫醫院和診所能夠採用最先進的心電圖系統,從而支持高效、精準的心臟診斷。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 寵物數量的增加和寵物的人性化

- 動物心臟病發生率上升

- 獸醫心電圖系統的技術進步

- 獸醫保健基礎設施的發展

- 產業潛在風險與挑戰

- 獸用心電圖系統高成本

- 開發中國家的意識程度較低

- 市場機遇

- 攜帶式和無線心電圖技術的擴展

- 遠距心臟病學服務的擴展

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 北美洲

- 科技與創新趨勢

- 目前技術

- 新興科技及其影響

- 各國寵物數量

- 專利分析

- 價格分析(基於初步調查)

- 未來市場趨勢(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 心電圖(ECG)系統

- 配件和耗材

第6章 市場估計與預測:依治療方式分類,2022-2035年

- 手持式

- 桌面型

第7章 市場估計與預測:依技術分類,2022-2035年

- 數位的

- 模擬

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 靜態心電圖

- 動態心電圖

第9章 市場估計與預測:依動物種類分類,2022-2035年

- 小型伴侶動物

- 狗

- 貓

- 其他小型伴侶動物

- 大型動物

- 馬

- 牛

- 豬

- 綿羊/山羊

- 其他大型動物

第10章 市場估價與預測:依最終用途分類,2022-2035年

- 獸醫醫院和診所

- 學術和研究機構

- 其他最終用戶

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- Antech Diagnostics

- Aspel

- Bionet America

- Contec Medical Systems

- Dextronix

- Dawei Veterinary Medical(Jiangsu)

- Eickemeyer Veterinary Equipment

- IDEXX Laboratories

- Narang Medical Limited

- New Gen Medical Systems

- Shenzhen Comen Medical Instruments

- Technocare Medisystems

- Vmed Technology

- VectraCor

The Global Veterinary ECG Systems Market was valued at USD 110 million in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 209.8 million by 2035.

Rising awareness regarding animal health and increasing spending on veterinary care are major factors contributing to market growth. Veterinary electrocardiogram systems are non-invasive diagnostic devices designed to record and analyze the electrical activity of the heart, enabling veterinarians to evaluate cardiac performance and identify abnormalities. As veterinary infrastructure expands and the number of specialized clinics and hospitals continues to grow, demand for advanced diagnostic technologies is increasing significantly. Improvements in veterinary medical technology are also enhancing the accuracy and usability of cardiac monitoring equipment. The introduction of digital platforms, wireless connectivity, and compact diagnostic tools is transforming how cardiac assessments are performed in veterinary practice. At the same time, the growing availability of pet insurance and improved access to professional veterinary services are supporting greater adoption of modern diagnostic equipment. These combined developments are creating favorable conditions for the continued expansion of the veterinary ECG systems market worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $110 Million |

| Forecast Value | $209.8 Million |

| CAGR | 6.8% |

Another important factor supporting the growth of the veterinary ECG systems market is the increasing occurrence of cardiac disorders in animals. Various heart-related conditions affecting animals require timely diagnosis and consistent monitoring to ensure effective treatment and long-term management. Veterinary professionals increasingly rely on ECG monitoring technologies because they provide precise and non-invasive methods for evaluating heart rhythm and electrical activity. As veterinary clinics and hospitals focus more on preventive care and early disease detection, the demand for reliable cardiac diagnostic equipment is rising steadily. Veterinary ECG systems play a crucial role in identifying abnormalities in heart function and enabling clinicians to monitor patient conditions over time.

The ECG systems segment accounted for USD 91 million in 2025. These systems serve as a fundamental diagnostic solution for monitoring heart rate patterns and detecting irregular cardiac activity in animals. Their role in identifying cardiovascular conditions has made them an essential component of veterinary diagnostic procedures. The increasing detection of complex cardiac complications among aging pets has contributed to the rising use of these systems across veterinary hospitals and specialized clinics. Additionally, heightened awareness among animal owners regarding potential heart-related health issues has increased the demand for advanced diagnostic testing. The growing popularity of portable and wireless ECG solutions has further supported segment expansion by enabling veterinarians to conduct real-time cardiac monitoring in both clinical environments and field-based veterinary practices.

Based on product configuration, the benchtop segment held a share of 57.3% in 2025. Benchtop systems remain widely used within veterinary practices because they provide reliable and detailed cardiac monitoring capabilities. These systems can record multiple ECG channels simultaneously, which allows veterinarians to conduct comprehensive cardiac assessments across a variety of animal species. Their ability to deliver highly accurate diagnostic data makes them particularly valuable in veterinary hospitals and diagnostic centers where detailed cardiac analysis is required. Benchtop ECG devices are often integrated with other diagnostic technologies and information management systems, which helps streamline clinical workflows and improve data management. Such integration enhances efficiency within veterinary facilities and supports more informed medical decision-making, ultimately contributing to better patient outcomes and sustained demand for these systems.

North America Veterinary ECG Systems Market held a 37.9% share in 2025. The region's leadership position is supported by a well-developed veterinary healthcare infrastructure and a high level of spending on animal healthcare services. Strong awareness regarding animal health and the widespread adoption of advanced veterinary diagnostic technologies are further contributing to market growth. In addition, the availability of specialized veterinary medical services and advanced treatment facilities is driving demand for sophisticated cardiac monitoring solutions. The presence of numerous industry participants and continuous technological innovation within the region is also helping strengthen market development, enabling veterinary clinics and hospitals to adopt modern ECG systems designed to support efficient and accurate cardiac diagnostics.

Prominent companies operating in the Global Veterinary ECG Systems Market include Antech Diagnostics (Mars Petcare), Aspel, Bionet America, Contec Medical Systems, Dextronix, Dawei Veterinary Medical (Jiangsu), Eickemeyer Veterinary Equipment, IDEXX Laboratories, Narang Medical Limited, New Gen Medical Systems, Shenzhen Comen Medical Instruments, Technocare Medisystems, Vmed Technology, and VectraCor. Companies competing in the Global Veterinary ECG Systems Market are implementing a variety of strategic initiatives to strengthen their market presence and expand their customer base. Manufacturers are increasingly focusing on product innovation by developing compact, wireless, and technologically advanced ECG solutions that improve diagnostic accuracy and ease of use. Many organizations are also investing in research and development to enhance device functionality, connectivity, and data analysis capabilities. Strategic collaborations with veterinary hospitals, diagnostic laboratories, and research institutions are helping companies expand their distribution networks and improve product accessibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Modality trends

- 2.2.4 Technology trends

- 2.2.5 Usage trends

- 2.2.6 Animal type trends

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership and pet humanization

- 3.2.1.2 Increase in cardiac disorders among animals

- 3.2.1.3 Technological advancements in veterinary ECG systems

- 3.2.1.4 Growth in veterinary healthcare infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of veterinary ECG systems

- 3.2.2.2 Limited awareness in developing economies

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of portable and wireless ECG technologies

- 3.2.3.2 Increasing adoption of telecardiology services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology and innovation landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies and their impact

- 3.6 Pet population, by country

- 3.7 Patent analysis

- 3.8 Pricing analysis (Driven by primary research)

- 3.9 Future market trends (Driven by primary research)

- 3.10 Impact of AI and generative AI on the market

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 -2035 ($ Mn)

- 5.1 Key trends

- 5.2 ECG systems

- 5.3 Accessories and consumables

Chapter 6 Market Estimates and Forecast, By Modality, 2022 -2035 ($ Mn)

- 6.1 Key trends

- 6.2 Handheld

- 6.3 Benchtop

Chapter 7 Market Estimates and Forecast, By Technology, 2022 -2035 ($ Mn)

- 7.1 Key trends

- 7.2 Digital

- 7.3 Analog

Chapter 8 Market Estimates and Forecast, By Usage, 2022 -2035 ($ Mn)

- 8.1 Key trends

- 8.2 Resting ECG

- 8.3 Holter ECG

Chapter 9 Market Estimates and Forecast, By Animal Type, 2022 -2035 ($ Mn)

- 9.1 Key trends

- 9.2 Small companion animals

- 9.2.1 Dogs

- 9.2.2 Cats

- 9.2.3 Other small companion animals

- 9.3 Large animals

- 9.3.1 Horses

- 9.3.2 Cattle

- 9.3.3 Swine

- 9.3.4 Sheep & goats

- 9.3.5 Other large animals

Chapter 10 Market Estimates and Forecast, By End Use, 2022 -2035 ($ Mn)

- 10.1 Key trends

- 10.2 Veterinary hospitals and clinics

- 10.3 Academic and research institutions

- 10.4 Other end users

Chapter 11 Market Estimates and Forecast, By Region, 2022 -2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Antech Diagnostics

- 12.2 Aspel

- 12.3 Bionet America

- 12.4 Contec Medical Systems

- 12.5 Dextronix

- 12.6 Dawei Veterinary Medical (Jiangsu)

- 12.7 Eickemeyer Veterinary Equipment

- 12.8 IDEXX Laboratories

- 12.9 Narang Medical Limited

- 12.10 New Gen Medical Systems

- 12.11 Shenzhen Comen Medical Instruments

- 12.12 Technocare Medisystems

- 12.13 Vmed Technology

- 12.14 VectraCor

全球心電圖貼片和心電圖監測市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球心電圖貼片和心電圖監測市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 心電圖貼片與心電圖監測市場-2026-2032年全球市場預測

心電圖貼片與心電圖監測市場-2026-2032年全球市場預測 穿戴式心電圖監測設備市場預測至2034年-全球產品類型、導線類型、監測類型、技術、應用、最終用戶和地區分析

穿戴式心電圖監測設備市場預測至2034年-全球產品類型、導線類型、監測類型、技術、應用、最終用戶和地區分析 心電圖耗材市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、病患群體、應用、最終用戶、地區和競爭格局分類,2021-2031年

心電圖耗材市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、病患群體、應用、最終用戶、地區和競爭格局分類,2021-2031年 全球人工智慧(AI)心電圖(ECG)市場分析:機會與策略展望至2035年

全球人工智慧(AI)心電圖(ECG)市場分析:機會與策略展望至2035年 心電圖(ECG)設備市場:依產品類型、技術、導極類型、最終用戶和地區分類術中監測電極市場:依手術、使用方法、電極類型、最終使用者和地區分類。心電圖監測系統市場:按設備類型、最終用戶和地區分類穿戴式心電圖監測儀市場預測至2034年-按類型、銷售管道、應用、最終用戶和地區分類的全球分析

心電圖(ECG)設備市場:依產品類型、技術、導極類型、最終用戶和地區分類術中監測電極市場:依手術、使用方法、電極類型、最終使用者和地區分類。心電圖監測系統市場:按設備類型、最終用戶和地區分類穿戴式心電圖監測儀市場預測至2034年-按類型、銷售管道、應用、最終用戶和地區分類的全球分析 心電圖設備市場機會、成長要素、產業趨勢分析及2026-2035年預測。

心電圖設備市場機會、成長要素、產業趨勢分析及2026-2035年預測。