|

市場調查報告書

商品編碼

1998711

磺達肝癸鈉市場機會、成長要素、產業趨勢分析及2026-2035年預測。Fondaparinux Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

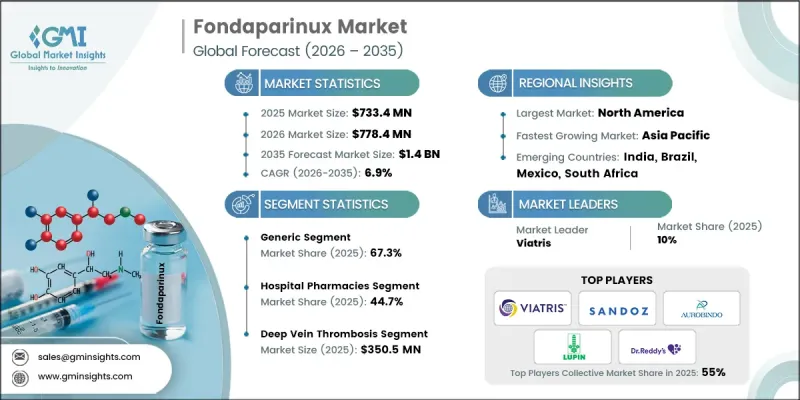

預計到 2025 年,全球磺達肝癸鈉市場價值將達到 7.334 億美元,並以 6.9% 的複合年成長率成長,到 2035 年將達到 14 億美元。

磺達肝癸鈉市場的穩定擴張主要受血栓性栓塞症發病率上升、整形外科手術數量增加以及全球人口快速老化等因素驅動。隨著凝血相關疾病發生率的持續上升,醫療專業人員越來越重視安全可靠且療效顯著的抗凝血治療。磺達肝癸鈉是一種合成抗凝血劑,它透過抑制特定的凝血途徑來幫助控制和預防血栓相關併發症。其穩定的藥理特性、較低的肝素相關副作用風險以及適用於大型手術後使用等特點,促使其在臨床實踐中得到更廣泛的應用。此外,醫療基礎設施的改善和經濟實惠的製劑的日益普及,也使更多患者能夠接受抗凝血治療。人們對早期診斷和治療凝血障礙重要性的認知不斷提高,進一步增強了對可靠治療方案的需求。這些因素共同支撐著全球磺達肝癸鈉市場的長期成長。全球人口結構變化導致血栓性栓塞症負擔加重、外科手術量增加以及抗凝血治療需求成長,這些因素進一步推動了該市場的發展。隨著醫療系統診斷能力的不斷提升,越來越多的凝血相關疾病患者需要接受預防性或治療性抗凝血治療,這些患者也因此被辨識出來。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 7.334億美元 |

| 預測金額 | 14億美元 |

| 複合年成長率 | 6.9% |

到2025年,學名藥市佔率將達到67.3%。非專利藥磺達肝癸鈉與磺達肝癸鈉具有生物等效性,在提供與品牌藥相當的療效的同時,價格更為親民。這些製劑廣泛用於靜脈血栓栓塞症的治療和預防。學名藥佔主導地位的主要原因是其成本優勢,使其在經濟高效的醫療保健體系中更容易獲得。此外,磺達肝癸鈉的臨床安全性和有效性已得到充分驗證,學名藥的推出顯著擴大了患者獲得該治療方法的機會。

預計到2025年,深層靜脈栓塞症(深層靜脈栓塞症)市場規模將達到3.505億美元。 DVT是指深層靜脈形成血栓,通常發生於下肢,是磺達肝癸鈉治療的主要適應症之一。由於其可靠的抗凝血效果和便捷的給藥方案,該藥物被廣泛用於血栓的預防和治療。隨著全球靜脈血栓栓塞症發病率的上升,醫療專業人員擴大對高風險患者實施藥物預防策略,因此該細分市場繼續保持強勁的市場地位。磺達肝癸鈉因其卓越的臨床療效、可靠的安全性以及抑制血栓進展和復發的確切療效,仍然是首選的治療方案。

預計2025年,北美磺達肝癸鈉市佔率將達39%。該地區的主導地位主要歸功於其醫療體系中靜脈血栓栓塞症的沉重臨床負擔。由於磺達肝癸鈉具有可預測的藥理作用和較低的特定藥物相關併發症風險,該地區的醫療機構持續採用這種可靠的抗凝血劑。此外,人口結構變化,包括人口老化,預計將在整個預測期內增加對抗凝血治療的需求。完善的醫療基礎設施和先進的醫療服務也促進了磺達肝癸鈉在北美醫院和專科治療中心的廣泛應用。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策和資料完整性計劃

- 資訊來源一致性通訊協定

- GMI人工智慧政策和資料完整性計劃

- 調查過程和可靠性評分

- 調查過程的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 血栓栓塞性疾病發生率增加

- 髖關節和膝關節關節重建手術數量增加

- 世界人口快速老化

- 提高對凝血障礙的認知和早期診斷

- 產業潛在風險與挑戰

- 與磺達肝癸鈉相關的副作用

- 醫療成本不斷上漲

- 市場機遇

- 新興市場的擴張

- 整形外科和創傷治療領域的機會不斷擴大

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術格局

- 目前技術

- 新興技術

- 價格分析(2025 年)(基於初步調查)

- 專利分析

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 品牌商品

- 非專利的

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 深層靜脈栓塞症

- 肺動脈栓塞

- 急性冠狀動脈症候群

- 其他用途

第7章 市場估價與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Abbott Laboratories

- Aspen Pharmacare Holdings

- Aurobindo

- BrightGene Health

- Dr. Reddy's Laboratories

- Jiangsu Hengrui Medicine

- Lupin Pharmaceuticals

- Sandoz

- ScinoPharm Taiwan

- Shanghai Minbiotech

- Viatris

The Global Fondaparinux Market was valued at USD 733.4 million in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 1.4 billion by 2035.

The steady expansion of the fondaparinux market is primarily supported by the increasing prevalence of thromboembolic conditions, rising number of orthopedic surgical procedures, and the rapidly aging global population. As the incidence of clotting related disorders continues to increase, healthcare providers are focusing more on effective anticoagulation therapies that offer reliable safety and therapeutic outcomes. Fondaparinux, a synthetic anticoagulant, helps in managing and preventing blood clot-related complications by inhibiting specific coagulation pathways. Its consistent pharmacological profile, reduced likelihood of heparin-related adverse reactions, and suitability for use following major surgical procedures have contributed to its growing acceptance in clinical practice. Additionally, improvements in healthcare infrastructure and the expanding availability of cost-effective drug formulations are supporting wider patient access to anticoagulant treatments. Increased awareness regarding the early diagnosis and management of clotting disorders is further strengthening demand for reliable therapeutic options. These combined factors continue to support the long-term growth of the global fondaparinux market. The market is further supported by the rising burden of thromboembolic disorders, increasing surgical interventions, and global demographic changes that contribute to a higher demand for anticoagulant therapy. As healthcare systems continue to improve diagnostic capabilities, more patients are being identified with clotting related conditions that require preventive or therapeutic anticoagulation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $733.4 Million |

| Forecast Value | $1.4 Billion |

| CAGR | 6.9% |

The generic segment accounted for 67.3% share in 2025. Generic fondaparinux consists of bioequivalent formulations of fondaparinux sodium that deliver the same therapeutic benefits as branded products while offering improved affordability. These formulations are widely used for the management and prevention of venous thromboembolism conditions. The dominance of this segment is primarily driven by the cost advantages associated with generic medications, which make them more accessible within healthcare systems that prioritize cost efficiency. In addition, fondaparinux has an established record of clinical safety and effectiveness, and the availability of generic versions has significantly expanded patient access to this treatment option.

The deep vein thrombosis segment generated USD 350.5 million in 2025. Deep vein thrombosis refers to the formation of blood clots within deep veins, typically affecting the lower extremities, and represents one of the primary medical conditions treated with fondaparinux therapy. The medication is widely utilized for both the prevention and treatment of clot formation due to its reliable anticoagulant action and convenient dosing schedule. This segment continues to maintain a strong market position as the global incidence of venous thromboembolism rises and healthcare providers increasingly implement pharmacological prevention strategies for at-risk patients. Fondaparinux remains a preferred therapeutic option because of its strong clinical performance, dependable safety characteristics, and proven ability to reduce clot progression and recurrence.

North America Fondaparinux Market held a 39% share in 2025. The region's leading position is largely attributed to the significant clinical burden of venous thromboembolism within its healthcare system. Medical facilities across the region continue to adopt fondaparinux as a reliable anticoagulant therapy due to its predictable pharmacological activity and reduced likelihood of certain drug-related complications. Furthermore, demographic changes, including an aging population, are expected to contribute to increasing demand for anticoagulant treatments throughout the forecast period. Strong healthcare infrastructure and access to advanced medical therapies also support the widespread use of fondaparinux across hospitals and specialized treatment centers in North America.

Key companies operating in the Global Fondaparinux Market include Viatris, Sandoz, Abbott Laboratories, Dr. Reddy's Laboratories, Lupin Pharmaceuticals, Aurobindo, Aspen Pharmacare Holdings, Jiangsu Hengrui Medicine, ScinoPharm Taiwan, BrightGene Health, and Shanghai Minbiotech. Companies participating in the Global Fondaparinux Market are implementing various strategic initiatives to strengthen their competitive presence and expand their global market reach. Leading pharmaceutical manufacturers are focusing on the development and distribution of cost-effective generic formulations to increase accessibility and capture a larger share of the anticoagulant therapy market. Many companies are also investing in research and development activities aimed at improving manufacturing processes and ensuring consistent product quality. Strategic collaborations with healthcare providers, distributors, and pharmaceutical partners are helping companies expand their geographic presence and strengthen supply chain capabilities. Additionally, firms are emphasizing regulatory approvals, portfolio diversification, and production capacity expansion to support growing global demand while maintaining strong competitiveness within the evolving fondaparinux market.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 Distribution channel trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of thromboembolic diseases

- 3.2.1.2 Increase in hip and knee transplant surgeries

- 3.2.1.3 Surge in aging population worldwide

- 3.2.1.4 Greater awareness and early diagnosis of clotting disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects associated with fondaparinux

- 3.2.2.2 High cost of treatment

- 3.2.3 Market opportunity

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Increasing opportunities in orthopedic and trauma care

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2025 (Driven by Primary Research)

- 3.7 Patent analysis

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Branded

- 5.3 Generic

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Deep vein thrombosis

- 6.3 Pulmonary embolism

- 6.4 Acute coronary syndrome

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Aspen Pharmacare Holdings

- 9.3 Aurobindo

- 9.4 BrightGene Health

- 9.5 Dr. Reddy's Laboratories

- 9.6 Jiangsu Hengrui Medicine

- 9.7 Lupin Pharmaceuticals

- 9.8 Sandoz

- 9.9 ScinoPharm Taiwan

- 9.10 Shanghai Minbiotech

- 9.11 Viatris