|

市場調查報告書

商品編碼

1998709

淬火液及鹽市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Quenching Fluids and Salts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球淬火液和鹽市場預計到 2025 年價值 21 億美元,預計到 2035 年將以 5.2% 的複合年成長率成長至 36 億美元。

淬火液和淬火鹽在熱處理製程中發揮核心作用,它們能夠快速冷卻加熱後的金屬,並賦予其所需的機械性能,例如更高的硬度和結構強度。這些材料能夠實現可控冷卻,從而直接影響處理後金屬的微觀結構、耐久性和尺寸穩定性。多年來,熱處理流程已轉向採用技術先進的淬火系統,旨在提高工業生產的效率和一致性。現代淬火技術強調改進冷卻控制、操作安全性和製程可靠性。製造商正在推出創新配方,以實現更精確的溫度控管,並最大限度地減少與快速冷卻過程相關的操作挑戰。市場上也正在開發旨在滿足不斷發展的永續發展標準的環保淬火解決方案。此外,將自動化和數位化製程監控整合到熱處理系統中,使工廠能夠實現更精確的溫度控制、更高的重複性和生產效率。所有這些進步共同強化了淬火液和淬火鹽在支援各種製造環境中使用的熱處理零件的性能和可靠性方面所發揮的作用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 21億美元 |

| 預測金額 | 36億美元 |

| 複合年成長率 | 5.2% |

預計2025年,淬火油市場規模將達12億美元。由於其可靠的冷卻性能和穩定的冶金性能,淬火油在熱處理過程中已廣泛應用。其可控的冷卻能力使其適用於各種熱處理系統和冶金要求。產業趨勢表明,人們越來越關注最佳化後的油品配方,以期在大規模生產環境中實現更快或更均衡的冷卻效果。製造商正日益關注能夠提高熱穩定性、減少蒸發和降低運作中排放的先進配方。這些發展有助於創造更安全的工業環境,同時延長油品壽命並保持製程的一致性。

預計到2025年,批量爐市場規模將達到6.166億美元。這些爐系統因其操作柔軟性、能夠適應不同尺寸的零件和生產規模而被廣泛應用於熱處理廠。製造商依靠這些系統實現高效的熱處理,同時精確控制淬火過程。隨著工業領域優先考慮提高生產效率、最佳化能源利用以及與多種淬火介質的兼容性,設備領域也不斷發展。爐體設計的技術進步提高了熱量分佈的均勻性、增強了自動化能力並提高了製程可靠性。設備供應商也致力於提供能夠簡化生產流程和確保加工結果一致性的解決方案。隨著工業設施對其熱處理基礎設施進行現代化改造,對能夠提供操作柔軟性和穩定淬火性能的爐體技術的需求預計將保持強勁。

預計2025年,美國淬火液和淬火鹽市場規模將達到4.596億美元。這一市場成長主要得益於成熟的製造業生態系統,該生態系統對高性能應用領域所需的高品質熱處理零件有著極高的需求。該地區的產業部門持續投資於先進的材料加工技術,以提高產品的可靠性和耐久性。同時,在加拿大,最新的淬火技術正作為更廣泛的工業現代化舉措的一部分得到穩步應用。該地區的製造商優先考慮提高生產效率和加強製作流程中的品管。數位化製造方法和自動化熱處理系統的日益普及,使企業能夠最佳化淬火工藝,減少操作失誤,並更有效地控制生產成本。這些因素共同推動了北美地區淬火液和淬火鹽市場的持續擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 成長促進因素

- 汽車和製造業的成長

- 對高性能材料的需求日益成長

- 熱處理製程的技術進步

- 產業潛在風險與挑戰

- 環境和監管方面的挑戰

- 冶金缺陷風險

- 市場機遇

- 擴大聚合物基淬滅劑的使用

- 基礎設施和能源計劃需求不斷成長

- 對客製化和特定應用解決方案的需求

- 成長促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 淬火油

- 快速/加速淬火油

- 中速淬火油

- 低速淬火油

- 馬奎恩奇/馬滕珀

- 真空淬火油

- 合成淬火油

- 其他

- 鹽用來淬火

- 硝酸鹽

- 亞硝酸鹽

- 氯化物

- 氰化物鹽

- 氟化物鹽

- 其他

- 聚合物基熱處理劑

- 基於聚亞烷基二醇(PAG)

- 基於聚乙烯吡咯烷酮(PVP)

- 其他

第6章 市場估算與預測:依反應器/設備類型分類,2022-2035年

- 批次爐

- 連續式爐

- 真空爐

- 感應加熱系統

- 鹽浴

- 閉式淬火爐

- 其他

第7章 市場估計與預測:依最終用戶產業分類,2022-2035年

- 車

- 航太/國防

- 施工機械和重型設備

- 模具製造

- 軸承製造

- 能源和發電

- 醫療設備

- 石油和天然氣

- 鐵路和交通運輸

- 礦業

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- BP Castrol

- Chemtool Incorporated

- Chevron Corporation

- CONDAT

- Croda International Plc

- Exxon Mobil Corporation

- FUCHS Petrolub SE

- Hubbard-Hall

- Idemitsu Kosan Co., Ltd.

- Metal Heat Treatment Solutions

- Park Thermal International

- Petrofer Chemie

- Quaker Houghton

- Savannah River Nuclear Solutions

- TotalEnergies SE

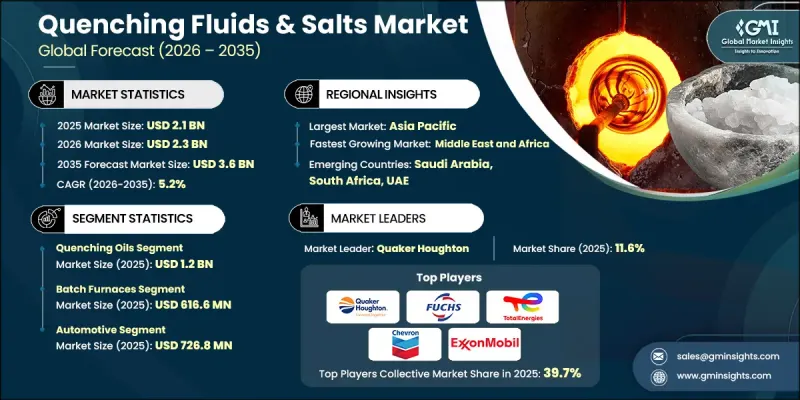

The Global Quenching Fluids & Salts Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 3.6 billion by 2035.

Quenching fluids and salts play a central role in heat treatment processes by rapidly cooling heated metals so that they achieve desired mechanical characteristics such as improved hardness and structural strength. These materials enable controlled cooling that directly influences the microstructure, durability, and dimensional stability of treated metals. Over time, heat treatment operations have increasingly transitioned toward technologically advanced quenching systems designed to improve efficiency and consistency in industrial production. Modern quenching technologies emphasize improved cooling control, operational safety, and enhanced process reliability. Manufacturers are introducing innovative formulations that support more precise thermal management and minimize operational challenges associated with rapid cooling processes. The market is also witnessing the development of environmentally considerate quenching solutions designed to meet evolving sustainability standards. In addition, growing integration of automation and digital process monitoring within heat treatment systems is helping facilities achieve better temperature regulation, repeatability, and productivity. These developments collectively strengthen the role of quenching fluids and salts in supporting the performance and reliability of heat-treated components used across multiple manufacturing environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 5.2% |

The quenching oils segment generated USD 1.2 billion in 2025. Quenching oils remain widely used in heat treatment operations because they provide reliable cooling characteristics and consistent metallurgical performance. Their ability to deliver controlled cooling makes them suitable for a wide range of heat treatment systems and metallurgical requirements. Industry trends indicate rising interest in optimized oil formulations designed to provide faster or more balanced cooling behavior for large-scale manufacturing environments. Manufacturers are increasingly focusing on advanced formulations that offer improved thermal stability, reduced evaporation, and lower emissions during operation. These developments are supporting safer industrial environments while also extending fluid life and maintaining process consistency.

The batch furnaces segment accounted for USD 616.6 million in 2025. These furnace systems are widely utilized in heat treatment facilities due to their operational flexibility and ability to process varied component sizes and production volumes. Manufacturers rely on these systems for efficient thermal processing while maintaining precise control over quenching operations. The equipment segment is evolving as industries prioritize improved production efficiency, optimized energy utilization, and compatibility with multiple quenching media. Technological advancements in furnace design are enabling better thermal uniformity, improved automation capabilities, and enhanced process reliability. Equipment suppliers are also focusing on solutions that support streamlined production workflows and consistent processing outcomes. As industrial facilities continue to modernize their heat treatment infrastructure, furnace technologies that deliver operational flexibility and stable quenching performance are expected to maintain strong demand.

United States Quenching Fluids & Salts Market reached USD 459.6 million in 2025. Market growth in the country is supported by the presence of a well-established manufacturing ecosystem that requires high-quality heat-treated components for demanding performance applications. Industrial sectors across the region continue to invest in advanced materials processing technologies to improve product reliability and durability. Meanwhile, Canada is steadily adopting modern quenching technologies as part of broader industrial modernization initiatives. Manufacturers across the region are emphasizing improved production efficiency and enhanced quality control in metal processing operations. Increasing adoption of digital manufacturing practices and automated heat treatment systems is helping companies optimize quenching processes, reduce operational errors, and control production costs more effectively. These factors collectively contribute to the continued expansion of the quenching fluids & salts market across North America.

Major companies operating in the Global Quenching Fluids & Salts Market include BP Castrol, Croda International Plc, CONDAT, Idemitsu Kosan Co., Ltd., Exxon Mobil Corporation, Petrofer Chemie, Chemtool Incorporated, FUCHS Petrolub SE, Quaker Houghton, TotalEnergies SE, Chevron Corporation, Hubbard-Hall, Park Thermal International, Metal Heat Treatment Solutions, and Savannah River Nuclear Solutions. Companies in the quenching fluids & salts market are focusing on multiple strategic initiatives to strengthen their competitive position and expand their global presence. Product innovation remains a key priority, with manufacturers investing in research and development to create advanced quenching solutions that deliver improved thermal performance, longer service life, and enhanced environmental compatibility. Strategic collaborations with equipment manufacturers and heat treatment service providers are also helping companies integrate their fluids into advanced thermal processing systems. In addition, firms are expanding production capabilities and distribution networks to serve growing industrial demand across emerging manufacturing regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Furnace/Equipment Type

- 2.2.3 End User Industry

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of automotive and manufacturing industries

- 3.2.1.2 Rising demand for high-performance materials

- 3.2.1.3 Technological advancements in heat treatment processes

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental and regulatory challenges

- 3.2.2.2 Risk of metallurgical defects

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of polymer-based quenchants

- 3.2.3.2 Rising demand from infrastructure and energy projects

- 3.2.3.3 Demand for customized and application-specific solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Quenching oils

- 5.2.1 Fast/accelerated quenching oils

- 5.2.2 Medium-speed quenching oils

- 5.2.3 Slow-speed quenching oils

- 5.2.4 Marquench/martempering

- 5.2.5 Vacuum quenching oils

- 5.2.6 Synthetic quenching oils

- 5.2.7 Others

- 5.3 Quenching salts

- 5.3.1 Nitrate-based salts

- 5.3.2 Nitrite-based salts

- 5.3.3 Chloride-based salts

- 5.3.4 Cyanide-based salts

- 5.3.5 Fluoride-based salts

- 5.3.6 Others

- 5.4 Polymer quenchants

- 5.4.1 PAG-based (polyalkylene glycol)

- 5.4.2 PVP-based (polyvinylpyrrolidone)

- 5.4.3 Others

Chapter 6 Market Estimates and Forecast, By Furnace/Equipment Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Batch furnaces

- 6.3 Continuous furnaces

- 6.4 Vacuum furnaces

- 6.5 Induction heating systems

- 6.6 Salt bath furnaces

- 6.7 Sealed quench furnaces

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By End User Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Aerospace and defense

- 7.4 Construction equipment and heavy machinery

- 7.5 Tool and die manufacturing

- 7.6 Bearing manufacturing

- 7.7 Energy and power generation

- 7.8 Medical devices

- 7.9 Oil and gas

- 7.10 Rail and transportation

- 7.11 Mining

- 7.12 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BP Castrol

- 9.2 Chemtool Incorporated

- 9.3 Chevron Corporation

- 9.4 CONDAT

- 9.5 Croda International Plc

- 9.6 Exxon Mobil Corporation

- 9.7 FUCHS Petrolub SE

- 9.8 Hubbard-Hall

- 9.9 Idemitsu Kosan Co., Ltd.

- 9.10 Metal Heat Treatment Solutions

- 9.11 Park Thermal International

- 9.12 Petrofer Chemie

- 9.13 Quaker Houghton

- 9.14 Savannah River Nuclear Solutions

- 9.15 TotalEnergies SE

工業用鹽市場:依產品類型、形態、等級和應用分類-2026-2032年全球市場預測

工業用鹽市場:依產品類型、形態、等級和應用分類-2026-2032年全球市場預測 2026年全球工業用鹽市場報告

2026年全球工業用鹽市場報告 工業鹽市場規模、佔有率及成長分析(依原料、製造流程、應用及地區分類)-2026-2033年產業預測

工業鹽市場規模、佔有率及成長分析(依原料、製造流程、應用及地區分類)-2026-2033年產業預測 袋裝鹽:全球市佔率及排名、總收入及需求預測(2025-2031年)

袋裝鹽:全球市佔率及排名、總收入及需求預測(2025-2031年) 2025-2033年工業鹽市場報告,依來源(鹽水、鹽礦)、產品(岩鹽、鹽水鹽、曬鹽、真空鍋鹽)、應用(化學加工、除冰、石油及天然氣、水處理、農業等)及地區分類

2025-2033年工業鹽市場報告,依來源(鹽水、鹽礦)、產品(岩鹽、鹽水鹽、曬鹽、真空鍋鹽)、應用(化學加工、除冰、石油及天然氣、水處理、農業等)及地區分類 全球工業鹽市場規模依來源、製造流程、應用、區域範圍、預測

全球工業鹽市場規模依來源、製造流程、應用、區域範圍、預測 全球袋裝工業用鹽市場(2025-2029)

全球袋裝工業用鹽市場(2025-2029) 2024-2028年全球工業用鹽市場

2024-2028年全球工業用鹽市場