|

市場調查報告書

商品編碼

1998702

2026 年至 2035 年太陽能電池用矽晶圓市場的機會、成長要素、產業趨勢分析與預測。Solar Silicon Wafer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

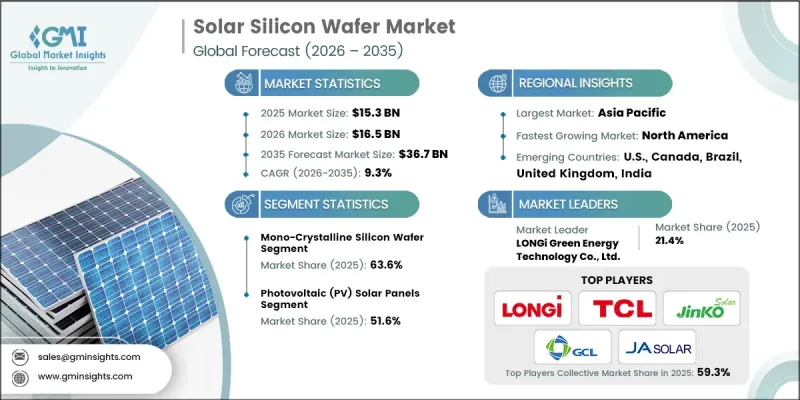

預計到 2025 年,全球太陽能電池用矽晶圓市場價值將達到 153 億美元,並有望以 9.3% 的複合年成長率成長,到 2035 年達到 367 億美元。

隨著各國政府、企業和能源開發商持續優先發展可再生能源發電,太陽能電池用矽晶圓產業正經歷穩定成長。全球範圍內為減少碳排放和向更清潔能源轉型所做的努力日益增多,顯著推動了光伏技術的需求。隨著大型發電工程、商業建築和住宅物業中太陽能發電系統的應用不斷增加,對高品質矽晶圓的需求也持續上升。太陽能電池用矽晶圓是太陽能電池的基本組成部分,也是光伏價值鏈的關鍵環節。此外,矽晶圓製造技術的進步,以及生產效率和材料利用率的提高,也為市場擴張提供了支持。人們對永續能源解決方案的日益關注,以及促進可再生能源應用的法規結構,持續推動對太陽能基礎設施的投資。這些因素共同加速了太陽能電池用矽晶圓市場的成長,同時也增強了全球光電生態系統。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 153億美元 |

| 預計金額 | 367億美元 |

| 複合年成長率 | 9.3% |

隨著全球向清潔永續能源系統轉型以及太陽能發電部署的不斷擴大,太陽能電池用矽晶圓市場持續成長。各行各業太陽能發電設施的日益普及,直接推動了對支援高效能太陽能轉換的先進矽晶圓技術的需求。各國在追求雄心勃勃的能源轉型目標並加強可再生能源發電能力的同時,製造商也在擴大產能並投資改善矽晶圓加工技術。太陽能製造供應鏈的持續發展,有助於提高產品效率、最佳化生產流程並增強系統整體可靠性。此外,支持可再生能源應用的政策架構和促進太陽能發電系統部署的金融機制,也強化了市場的長期需求。這些趨勢正在鞏固太陽能電池用矽晶圓作為現代太陽能基礎設施關鍵材料的地位。

預計到2035年,多晶晶片市場將以8.2%的複合年成長率成長。與其他晶片技術相比,多晶晶片被廣泛應用於此類計劃。隨著市場對經濟型太陽光電技術的需求不斷成長,尤其是在大規模太陽能發電裝置中成本最佳化至關重要的市場,多晶矽晶片也從中受益。隨著太陽能發電產能的持續提升以及製程改進帶來的晶片性能的提高,預計多晶晶片將在更廣泛的太陽能生態系統中廣泛應用。其在保持成本競爭力的同時實現大規模生產的能力,使其成為擴大太陽能發電產能的可靠選擇。

預計到2025年,太陽能板市佔率將達到51.6%。矽晶圓是太陽能組件的核心材料,用於將太陽光轉化為可用電能。這些矽晶圓對於建造分散式太陽能發電系統和大型太陽能發電設施中部署的光學模組至關重要。整合到現代太陽能發電技術中,可以實現高效發電,並支持全球太陽能發電裝置容量的持續成長。隨著全球太陽能產業的擴張,對太陽能組件的需求不斷成長,進而增加了對高品質矽晶圓的需求。隨著太陽能發電裝置容量的穩定成長,未來太陽能板的製造無疑仍將是矽晶圓在太陽能電池領域的主要應用之一。

預計2026年至2035年,北美太陽能電池用矽晶圓市場將以10.6%的複合年成長率成長。該地區住宅、商業和大型發電工程的太陽能發電裝置量正在快速成長。對可再生能源基礎設施投資的增加推動了先進矽晶圓製造能力的發展和太陽光電技術的進步。美國和加拿大太陽能發電裝置容量的擴張增強了對高性能單晶矽晶圓的需求,這些矽晶圓能夠實現更高的能量轉換效率。可再生能源基礎設施的持續發展和對太陽光電技術創新的持續投資正推動北美成為全球太陽能矽晶圓市場的高成長地區。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球太陽能發電裝置容量的成長是由向可再生能源轉型所驅動的。

- 政府獎勵和補貼旨在加速太陽能的普及

- 透過製程最佳化和規模化降低晶圓製造成本。

- 提高矽晶圓效率和產量比率的技術進步

- 企業永續發展措施正在推動大規模太陽能發電工程。

- 產業潛在風險與挑戰

- 先進的晶圓製造設施需要大量的資金投入。

- 多晶矽價格的波動正在影響太陽能發電矽晶圓的整體盈利。

- 市場機遇

- 對高效能單晶和大尺寸尺寸晶圓的需求不斷成長

- 政府本土化政策支持國內太陽能發電製造業擴張

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興競爭對手和Start-Ups競爭對手的發展趨勢

第5章 市場估計與預測:依類型分類,2022-2035年

- 單晶矽晶片

- 多晶晶片

- 多晶晶片

第6章 市場規模估算與預測(2022-2035年)

- 小晶圓(小於 200 毫米)

- 標準晶圓(200毫米至300毫米)

- 大尺寸晶圓(超過 300 毫米)

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 太陽能發電(PV)面板

- 太陽能電池

- 聚光型太陽光電(CSP)系統

- 其他

第8章 市場估算與預測:依最終用途產業分類,2022-2035年

- 住宅

- 商業的

- 工業的

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- LONGi Green Energy Technology Co., Ltd.

- TCL Zhonghuan Renewable Energy Technology Co. Ltd.

- GCL-Poly Energy Holdings Limited(GCL Group)

- JinkoSolar Holding Co., Ltd.

- JA Solar Holdings Co., Ltd

- 按地區分類的主要企業

- 北美洲

- Canadian Solar Inc.

- 亞太地區

- China Silicon Corporation Ltd.

- Risen Energy Co., Ltd.

- Runergy New Energy Co., Ltd.

- Solargiga Energy Holding Co., Ltd.

- Trina Solar Co., Ltd.

- Xinjiang Daqo New Energy Corporation

- 北美洲

- 特殊玩家/干擾者

- Atecom Technology

- Danen Technology Co., Ltd.

- Gokin Solar Co., Ltd.

- Huita Optoelectronic Material Co., Ltd.

- JYT Corporation

- Leshan Jingyuntong New Materials Technology Co., Ltd.

- Solartec Corporation

- Suntro Corporation

The Global Solar Silicon Wafer Market was valued at USD 15.3 billion in 2025 and is estimated to grow at a CAGR of 9.3% to reach USD 36.7 billion by 2035.

The solar silicon wafer industry is witnessing steady expansion as governments, businesses, and energy developers continue prioritizing renewable energy generation. Growing global commitment to reducing carbon emissions and transitioning toward cleaner power sources is significantly strengthening the demand for solar power technologies. As solar power installations increase across utility-scale projects, commercial buildings, and residential properties, the requirement for high-quality silicon wafers continues to rise. Solar silicon wafers serve as the fundamental building blocks of photovoltaic cells, making them essential components within the solar energy value chain. In addition, technological advancements in wafer manufacturing, along with improvements in production efficiency and material utilization, are supporting the expansion of the market. Rising awareness of sustainable energy solutions, combined with supportive regulatory frameworks that promote renewable energy adoption, continues to encourage investments in solar infrastructure. These factors are collectively accelerating the growth of the solar silicon wafer market while strengthening the global solar power ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.3 Billion |

| Forecast Value | $36.7 Billion |

| CAGR | 9.3% |

The solar silicon wafer market continues to gain momentum as solar power deployment expands globally in response to the growing shift toward clean and sustainable energy systems. Increasing installation of solar power capacity across multiple sectors is directly driving the demand for advanced wafer technologies capable of supporting efficient photovoltaic energy conversion. As countries pursue ambitious energy transition targets and strengthen renewable power capacity, manufacturers are expanding production capabilities and investing in improved wafer processing technologies. Continuous developments across the solar manufacturing supply chain are helping improve product efficiency, optimize production processes, and enhance overall system reliability. In addition, policy frameworks supporting renewable power adoption, along with financial mechanisms that encourage solar system deployment, are strengthening long-term market demand. These developments are positioning solar silicon wafers as a critical material within modern solar energy infrastructure.

The poly-crystalline silicon wafer segment is expected to grow at a CAGR of 8.2% throughout 2035. The segment continues to attract demand because of its relatively lower production costs and simplified manufacturing processes compared with other wafer technologies. Poly-crystalline wafers are widely utilized in projects where cost efficiency plays an important role in system design and investment planning. The segment benefits from increasing demand for affordable solar technologies, particularly in markets where large-scale solar installations prioritize cost optimization. As solar manufacturing capacity continues to increase and process improvements enhance wafer performance, poly-crystalline wafers are expected to maintain strong adoption within the broader solar ecosystem. Their ability to support large-volume production while maintaining competitive cost structures makes them a reliable option for expanding solar energy capacity.

The photovoltaic solar panels segment accounted for 51.6% share in 2025. Silicon wafers form the core material used in photovoltaic modules, which convert sunlight into usable electricity. These wafers are essential for the construction of solar modules deployed across distributed solar systems and large-scale solar energy facilities. Their integration into modern photovoltaic technologies enables efficient power generation and supports the continued growth of solar power installations worldwide. As the global solar energy industry expands, the demand for photovoltaic modules continues to strengthen, thereby increasing the requirement for high-quality silicon wafers. The consistent growth of solar power generation capacity ensures that photovoltaic panel manufacturing will remain the primary application for solar silicon wafers.

North America Solar Silicon Wafer Market will grow at a CAGR of 10.6% during 2026 to 2035. The region is witnessing rapid expansion in solar power installations across residential, commercial, and large-scale power generation projects. Increasing investment in renewable energy infrastructure is encouraging the development of advanced wafer manufacturing capabilities and improved solar technologies. The expansion of solar capacity in both the United States and Canada is strengthening demand for high-performance mono-crystalline silicon wafers, which support higher energy conversion efficiency. Continued development of renewable energy infrastructure and sustained investment in solar technology innovation are contributing to North America's emergence as a high-growth region within the global solar silicon wafer market.

Key players operating in the Global Solar Silicon Wafer Market include Atecom Technology, Canadian Solar Inc., China Silicon Corporation Ltd., Danen Technology Co., Ltd., GCL-Poly Energy Holdings Limited (GCL Group), Gokin Solar Co., Ltd., Huita Optoelectronic Material Co., Ltd., JYT Corporation, JA Solar Holdings Co., Ltd., JinkoSolar Holding Co., Ltd., Leshan Jingyuntong New Materials Technology Co. Ltd., LONGi Green Energy Technology Co., Ltd., Risen Energy Co., Ltd., Runergy New Energy Co., Ltd., Solargiga Energy Holding Co., Ltd., Solartec Corporation, Suntro Corporation, TCL Zhonghuan Renewable Energy Technology Co., and Trina Solar Co., Ltd. Companies operating in the solar silicon wafer market are focusing on multiple strategic initiatives to reinforce their competitive position and expand their global presence. Industry participants are prioritizing research and development to enhance wafer efficiency, improve manufacturing yield, and reduce material wastage during production. Many companies are also investing in capacity expansion to meet the rising demand from the global solar photovoltaic industry. Strategic partnerships with solar module manufacturers and renewable energy developers are helping firms strengthen supply chain integration and secure long-term contracts. In addition, organizations are emphasizing vertical integration across the solar value chain, enabling greater control over raw materials, production processes, and distribution networks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Size trends

- 2.2.3 Application trends

- 2.2.4 End-use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global solar installations driven by renewable energy transition

- 3.2.1.2 Government incentives and subsidies accelerating solar photovoltaic adoption

- 3.2.1.3 Declining wafer manufacturing costs through process optimization and scaling

- 3.2.1.4 Technological advancements improving silicon wafer efficiency and yield rates

- 3.2.1.5 Corporate sustainability commitments boosting large-scale solar power projects

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital expenditure required for advanced wafer manufacturing facilities

- 3.2.2.2 Volatile polysilicon prices impacting overall solar silicon wafer profitability

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for high-efficiency monocrystalline and larger-format wafers

- 3.2.3.2 Expansion of domestic solar manufacturing supported by government localization policies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Mono-crystalline silicon wafer

- 5.3 Poly-crystalline silicon wafer

- 5.4 Multi-crystalline silicon wafer

Chapter 6 Market Estimates and Forecast, By Size, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Small wafer (less than 200 mm)

- 6.3 Standard wafer (200 mm to 300 mm)

- 6.4 Large wafer (greater than 300 mm)

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Photovoltaic (PV) solar panels

- 7.3 Solar cells

- 7.4 Concentrated solar power (CSP) systems

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 LONGi Green Energy Technology Co., Ltd.

- 10.1.2 TCL Zhonghuan Renewable Energy Technology Co. Ltd.

- 10.1.3 GCL-Poly Energy Holdings Limited (GCL Group)

- 10.1.4 JinkoSolar Holding Co., Ltd.

- 10.1.5 JA Solar Holdings Co., Ltd

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Canadian Solar Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 China Silicon Corporation Ltd.

- 10.2.2.2 Risen Energy Co., Ltd.

- 10.2.2.3 Runergy New Energy Co., Ltd.

- 10.2.2.4 Solargiga Energy Holding Co., Ltd.

- 10.2.2.5 Trina Solar Co., Ltd.

- 10.2.2.6 Xinjiang Daqo New Energy Corporation

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Atecom Technology

- 10.3.2 Danen Technology Co., Ltd.

- 10.3.3 Gokin Solar Co., Ltd.

- 10.3.4 Huita Optoelectronic Material Co., Ltd.

- 10.3.5 JYT Corporation

- 10.3.6 Leshan Jingyuntong New Materials Technology Co., Ltd.

- 10.3.7 Solartec Corporation

- 10.3.8 Suntro Corporation

半導體矽晶圓回收市場:依回收製程、晶圓類型、晶圓尺寸、應用領域、產業及最終用戶分類-2026-2032年全球市場預測單晶矽晶片市場:2026年至2032年全球預測(按晶片直徑、摻雜類型、拋光處理、厚度、應用和最終用戶分類)雙通道電阻率儀市場:依產品類型、應用、最終用戶和銷售管道,全球預測,2026-2032年

半導體矽晶圓回收市場:依回收製程、晶圓類型、晶圓尺寸、應用領域、產業及最終用戶分類-2026-2032年全球市場預測單晶矽晶片市場:2026年至2032年全球預測(按晶片直徑、摻雜類型、拋光處理、厚度、應用和最終用戶分類)雙通道電阻率儀市場:依產品類型、應用、最終用戶和銷售管道,全球預測,2026-2032年 半導體矽晶圓市場:依類型、尺寸、應用、最終用途、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測

半導體矽晶圓市場:依類型、尺寸、應用、最終用途、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測 2026年全球矽晶圓市場報告

2026年全球矽晶圓市場報告 日本矽晶圓市場報告(依晶圓尺寸、類型、應用、最終用途和地區分類,2026-2034年)

日本矽晶圓市場報告(依晶圓尺寸、類型、應用、最終用途和地區分類,2026-2034年) 單晶矽晶片市場規模、佔有率和成長分析(按直徑、製造流程、純度、應用類型、終端用戶產業和地區分類)-2026-2033年產業預測

單晶矽晶片市場規模、佔有率和成長分析(按直徑、製造流程、純度、應用類型、終端用戶產業和地區分類)-2026-2033年產業預測 太陽能矽晶圓市場規模、佔有率和成長分析(按純度等級、尺寸、技術、應用和地區分類)—產業預測(2026-2033 年)

太陽能矽晶圓市場規模、佔有率和成長分析(按純度等級、尺寸、技術、應用和地區分類)—產業預測(2026-2033 年) 全球半導體矽晶圓市場

全球半導體矽晶圓市場 用於晶圓的高純度碳化矽粉末:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

用於晶圓的高純度碳化矽粉末:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)