|

市場調查報告書

商品編碼

1998691

鐵路物流市場機會、成長要素、產業趨勢分析及2026-2035年預測。Rail Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

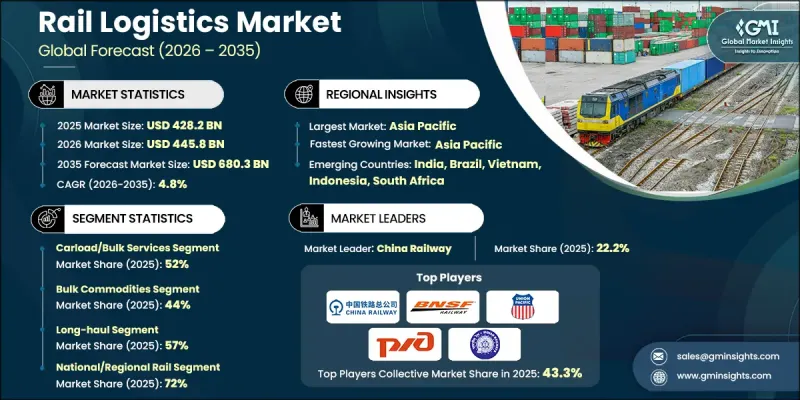

2025年全球鐵路物流市場價值4,282億美元,預計2035年將以4.8%的複合年成長率成長至6,803億美元。

鐵路貨運業者正日益將鐵路運輸與公路和海運物流結合,建構能夠滿足多樣化運輸需求的綜合供應鏈解決方案。這種多模態方式增強了營運柔軟性,並實現了區域和國際貿易走廊間貨物的高效運輸。跨境鐵路網路的擴張透過增加可用貨運路線的數量和改善生產基地與消費市場之間的連結性,正在強化全球供應鏈。隨著鐵路走廊的擴展和運營網路的日益互聯互通,貨運運營商能夠以更高的可靠性進行更遠距離的貨物運輸。旨在改善鐵路基礎設施、擴大貨運能力和提高運輸效率的投資進一步推動了鐵路在全球物流網路中日益重要的角色。這些趨勢正在強化鐵路貨運作為主要全球貿易路線上長途貨運的一種經濟高效且環境永續的解決方案的重要性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 4282億美元 |

| 預測金額 | 6803億美元 |

| 複合年成長率 | 4.8% |

數位轉型在鐵路物流市場的重組中也發揮著至關重要的作用。先進技術的應用使營運商能夠提高營運可視性、最佳化線路規劃並加強維護管理。鐵路公司正在投資建造支援即時貨物追蹤、自動調度和預測性維護的數位化系統。人工智慧、物聯網 (IoT) 連接和高級分析工具等技術正在幫助營運商更有效地監控貨物運輸,同時提高網路可靠性和營運效率。同時,對鐵路貨運基礎設施的大規模投資正在擴大網路運力並提高貨運速度。

預計到2025年,貨車和散裝運輸服務市場佔有率將達到52%,並在2026年至2035年間以3.8%的複合年成長率成長。這些運輸服務對於長途運輸大批量貨物至關重要。鐵路營運商經常採用這種貨運模式,使用專用貨車運輸大批量貨物,尤其適用於工業貨物和大規模製造供應鏈。需要大批量運輸的行業通常依賴鐵路貨運,透過廣泛的物流網路有效運輸貨物。對散裝運輸服務的穩定需求支撐著穩定的貨運量,使鐵路公司能夠維持高運轉率,並提供經濟高效的長途物流解決方案。

預計到2025年,散裝貨物運輸市場佔有率將達到44%,並在2026年至2035年間以3.1%的複合年成長率成長。由於其成本效益和高運力,鐵路運輸仍然是長途運輸大量工業材料和原料的首選方式。散裝貨物的運輸通常涉及重型或特殊貨物,因此需要能夠處理大量貨物的專用運輸基礎設施。鐵路營運商不斷致力於透過延長列車長度、最佳化裝載能力和引入自動化裝載系統來提高營運效率。這些營運改善縮短了周轉時間,使物流業者更有效地處理不斷成長的貨運量。在工業生產和能源產業活動持續推動下,對大規模原料運輸的需求保持穩定,預計鐵路貨運服務將在全球物流網路中保持強大的地位。

美國鐵路物流市場預計到2025年將達到9,15億美元,並在2026年至2035年間以4.7%的複合年成長率成長。多式聯運正成為國內鐵路物流業的主要驅動力。零售貨運量和電商配送量的不斷成長促使物流公司將鐵路運輸整合到更廣泛的供應鏈營運中。多式聯運使貨物能夠在港口、鐵路貨運站和最後一公里配送網路之間高效流動,從而建立一個能夠處理大量貨櫃的無縫配送系統。鐵路營運商也在投資先進技術,以支援即時貨物追蹤、智慧調度系統和預測分析,從而提高營運效率。這些技術能力有助於減少運輸延誤,最佳化複雜物流網路中的貨物運輸,從而強化鐵路運輸在國家不斷發展的貨運基礎設施中的作用。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 鐵路基礎設施營運商

- 鐵路車輛製造商

- 服務提供者

- 碼頭和轉運設施

- 技術和軟體供應商

- 最終用戶

- 影響產業的因素

- 促進因素

- 多式聯運的需求日益成長

- 電子商務和零售出貨量增加

- 政府對貨運走廊的投資

- 對經濟高效且永續的運輸方式的需求日益成長。

- 產業潛在風險與挑戰

- 基礎設施維修成本成本高昂

- 法規和跨境挑戰

- 市場機遇

- 利用數位化和物聯網的鐵路解決方案

- 新興市場(印度、非洲)擴張

- 引進環保電力機車

- 與第三方物流和多模態物流網路合作

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 聯邦鐵路管理局 (FRA)

- 美國鐵路協會(AAR)

- 歐洲

- 歐洲鐵路管理局(ERA)

- 國際鐵路聯盟(UIC)

- 亞太地區

- 印度鐵道部

- 日本運輸安全委員會/JR標準

- 拉丁美洲

- 巴西陸路運輸管理局(ANTT)

- 墨西哥國家鐵路運輸委員會(Comision Nacional de Transporte Ferroviario)

- 中東和非洲

- 阿拉伯聯合大公國聯邦交通管理局 - 鐵路

- 沙烏地阿拉伯鐵路公司/標準化機構

- 北美洲

- 波特五力分析

- PESTEL 分析

- 專利分析(基於初步研究)

- 按技術領域分類的專利申請趨勢

- 主要專利擁有者人和智慧財產權 (IP) 的定位

- 新興技術的專利趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 服務類型收費系統(多式聯運與公路自駕)

- 燃油額外費用機制

- 拘留費和雜項費用

- 成本細分分析

- 專利分析(基於初步研究)

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 關於碳足跡的考量

- 交易數據分析(基於付費資料庫)

- 進出口數量和價值的變化趨勢

- 主要貿易走廊及關稅的影響

- 跨境鐵路貨運

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- GenAI 各細分市場的應用案例與部署藍圖

- 風險、限制和監管考量

- 服務交付能力和提供者基礎設施(基於初步調查)

- 區域醫療服務提供者網路密度和覆蓋範圍

- 供給能力缺口與可用需求不匹配

- 預測假設與情境分析(基於一手研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依服務業分類,2022-2035年

- 多式聯運服務

- 車輛間散裝運輸服務

- 轉運服務

第6章 市場估價與預測:依貨物類型分類,2022-2035年

- 散貨

- 礦物和礦石

- 煤炭

- 穀物和農產品

- 貨櫃貨物

- 消費品

- 電子設備

- 機械和設備

- 特種貨物

- 車

- 藥品和化學品

- 冷藏和生鮮產品

第7章 市場估計與預測:依距離分類,2022-2035年

- 短距離

- 中距離

- 長途

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 礦業

- 農業

- 能源

- 製造業

- 建造

- 零售

- 車

- 化學

- 食品/飲料

- 其他

第9章 市場估價與預測:依鐵路類型分類,2022-2035年

- 國內和區域鐵路

- 高速鐵路物流

- 僅供貨物通行的通道

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 波蘭

- 羅馬尼亞

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 埃及

第11章:公司簡介

- 世界公司

- BNSF Railway

- Canadian National Railway(CN)

- Canadian Pacific Kansas City(CPKC)

- China Railway Freight

- CSX Transportation

- Deutsche Bahn(DB Cargo)

- Indian Railways

- Norfolk Southern Railway

- Russian Railways(RZD)

- Union Pacific Railroad

- 本地企業

- Aurizon

- Euro Cargo Rail

- Ferromex

- Genesee & Wyoming

- Kansas City Southern

- OBB Rail Cargo

- PKP Cargo

- 新興企業

- Japan Freight Railway Company

- SNCF Logistics

- VTG

The Global Rail Logistics Market was valued at USD 428.2 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 680.3 billion by 2035.

Rail freight operators are increasingly combining rail transport with road and maritime logistics to create integrated supply chain solutions capable of supporting diverse shipping requirements. This multimodal approach improves operational flexibility while enabling cargo to move efficiently across regional and international trade corridors. Expanding cross-border rail networks are strengthening global supply chains by increasing the number of available freight routes and improving connectivity between production centers and consumption markets. As rail corridors expand and operational networks become more interconnected, freight operators are able to deliver goods across longer distances with improved reliability. The growing role of rail within global logistics networks is further supported by investments aimed at improving rail infrastructure, expanding freight capacity, and enhancing transportation efficiency. These developments are reinforcing the importance of rail freight as a cost-effective and environmentally sustainable solution for long-distance cargo transportation across major global trade routes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $428.2 Billion |

| Forecast Value | $680.3 Billion |

| CAGR | 4.8% |

Digital transformation is also playing a significant role in reshaping the rail logistics market. Increasing adoption of advanced technologies is enabling operators to improve operational visibility, optimize route planning, and enhance maintenance management. Rail companies are investing in digital systems that support real-time freight tracking, automated scheduling, and predictive maintenance capabilities. Technologies such as artificial intelligence, Internet of Things connectivity, and advanced analytics tools are helping operators monitor freight movement more effectively while improving network reliability and operational efficiency. In parallel, large-scale investments in rail freight infrastructure are expanding network capacity and enabling faster cargo movement.

The carload and bulk freight services segment held 52% share in 2025 and is projected to grow at a CAGR of 3.8% between 2026 and 2035. These transportation services remain essential for moving large volumes of goods over long distances. Rail operators frequently rely on this freight model to transport substantial cargo loads in dedicated railcars, making it particularly suitable for industrial shipments and large-scale manufacturing supply chains. Industries requiring high-volume transportation often depend on rail freight to move goods efficiently across extensive logistics networks. The consistent demand for bulk transportation services supports stable freight volumes, enabling rail companies to maintain strong utilization rates while delivering cost-effective long-distance logistics solutions.

The bulk commodities segment captured 44% share in 2025 and is expected to grow at a CAGR of 3.1% from 2026 to 2035. Rail transportation remains a preferred solution for moving large quantities of industrial and raw materials across long distances due to its cost efficiency and high capacity. Bulk freight shipments often involve heavy cargo that requires specialized transportation infrastructure capable of handling substantial loads. Rail operators are continuously focusing on improving operational efficiency by increasing train lengths, optimizing cargo capacity, and implementing automated loading systems. These operational improvements are helping reduce turnaround times while enabling logistics providers to handle growing freight volumes more effectively. As industrial production and energy sector activities continue to generate consistent demand for large-scale raw material transportation, rail freight services are expected to maintain a strong presence within global logistics networks.

United States Rail Logistics Market reached USD 91.5 billion in 2025 and is expected to grow at a CAGR of 4.7% between 2026 and 2035. Intermodal freight transportation is emerging as a key growth driver within the country's rail logistics sector. The increasing volume of retail shipments and digital commerce deliveries is encouraging logistics companies to integrate rail transportation into broader supply chain operations. Intermodal transportation allows cargo to move efficiently between ports, rail terminals, and last-mile delivery networks, creating a seamless distribution system capable of handling large container volumes. Rail operators are also investing in advanced technologies that support real-time shipment tracking, intelligent scheduling systems, and predictive analytics to improve operational efficiency. These technological capabilities help reduce transit delays and optimize freight movement across complex logistics networks, strengthening the role of rail transportation in the country's evolving freight infrastructure.

Major companies operating in the Global Rail Logistics Market include BNSF Railway, Canadian National Railway, Canadian Pacific Kansas City, China Railway, CSX Transportation, Deutsche Bahn (DB Cargo), Indian Railways, Norfolk Southern, Russian Railways (RZD), and Union Pacific. Companies participating in the Global Rail Logistics Market are implementing several strategic initiatives to strengthen their market positions and expand operational capabilities. Rail operators are investing in infrastructure modernization programs to improve network capacity, enhance freight handling capabilities, and support higher cargo volumes. Many companies are also focusing on digital transformation by deploying advanced technologies such as AI-based scheduling systems, predictive maintenance tools, and real-time cargo monitoring platforms to optimize operational performance. Strategic partnerships with shipping companies, port authorities, and logistics providers are helping rail operators develop integrated multimodal transportation solutions that enhance supply chain efficiency. Additionally, companies are prioritizing sustainability initiatives by improving fuel efficiency and adopting environmentally responsible freight transportation practices to align with evolving regulatory standards and customer expectations.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Cargo

- 2.2.4 Distance

- 2.2.5 End use

- 2.2.6 Rail

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Rail infrastructure providers

- 3.1.2 Rolling Stock Manufacturers

- 3.1.3 Service Operators

- 3.1.4 Terminal & Transloading Facilities

- 3.1.5 Technology & Software Provider

- 3.1.6 End user

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing intermodal transportation demand

- 3.2.1.2 Increasing e-commerce and retail shipments

- 3.2.1.3 Government investment in dedicated freight corridors

- 3.2.1.4 Rising need for cost-efficient and sustainable transport

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure maintenance costs

- 3.2.2.2 Regulatory and cross-border challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Digitalization and IoT-enabled rail solutions

- 3.2.3.2 Expansion in emerging markets (India, Africa)

- 3.2.3.3 Adoption of green and electrified locomotives

- 3.2.3.4 Integration with 3PL and multimodal logistics networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Railroad Administration (FRA)

- 3.4.1.2 Association of American Railroads (AAR)

- 3.4.2 Europe

- 3.4.2.1 European Union Agency for Railways (ERA)

- 3.4.2.2 International Union of Railways (UIC)

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Railways (India)

- 3.4.3.2 Japan Transport Safety Board / JR Standards

- 3.4.4 Latin America

- 3.4.4.1 Agencia Nacional de Transportes Terrestres (ANTT, Brazil)

- 3.4.4.2 Comision Nacional de Transporte Ferroviario (Mexico)

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Federal Transport Authority - Railways

- 3.4.5.2 Saudi Railways Organization / Standards Authority

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Patent analysis (Driven by primary research)

- 3.7.1 Patent Filing Trends by Technology Area

- 3.7.2 Key Patent Holders & IP Positioning

- 3.7.3 Emerging Technology Patent Activity

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Pricing Analysis (Driven by primary research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9.3 Rate Structure by Service Type (Intermodal vs Carload)

- 3.9.4 Fuel Surcharge Mechanisms

- 3.9.5 Demurrage & Accessorial Charges

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis (Driven by primary research)

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Trade Data Analysis (Driven by paid database)

- 3.13.1 Import/export volume & value trends

- 3.13.2 Key trade corridors & tariff impact

- 3.13.3 Cross-border rail freight flows

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-Driven Disruption of Existing Business Models

- 3.14.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.14.3 Risks, limitations & regulatory considerations

- 3.15 Service delivery capacity & provider infrastructure (Driven by primary research)

- 3.15.1 Provider network density & coverage by region

- 3.15.2 Capacity gaps & addressable demand mismatch

- 3.16 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Intermodal services

- 5.3 Carload/bulk services

- 5.4 Transloading services

Chapter 6 Market Estimates & Forecast, By Cargo, 2022 - 2035 ($Mn, Tons)

- 6.1 Key trends

- 6.2 Bulk commodities

- 6.2.1 Minerals & ores

- 6.2.2 Coal

- 6.2.3 Grains & agricultural products

- 6.3 Containerized cargo

- 6.3.1 Consumer goods

- 6.3.2 Electronics

- 6.3.3 Machinery & equipment

- 6.4 Specialized cargo

- 6.4.1 Automotive

- 6.4.2 Pharmaceuticals & chemicals

- 6.4.3 Refrigerated/perishable goods

Chapter 7 Market Estimates & Forecast, By Distance, 2022 - 2035 ($Mn, Tons)

- 7.1 Key trends

- 7.2 Short haul

- 7.3 Medium-haul

- 7.4 Long-haul

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Tons)

- 8.1 Key trends

- 8.2 Mining

- 8.3 Agriculture

- 8.4 Energy

- 8.5 Manufacturing

- 8.6 Construction

- 8.7 Retail

- 8.8 Automotive

- 8.9 Chemical

- 8.10 Food & beverages

- 8.11 Others

Chapter 9 Market Estimates & Forecast, By Rail, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 National/regional rail

- 9.3 High-speed rail logistics

- 9.4 Dedicated freight corridors

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Egypt

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 BNSF Railway

- 11.1.2 Canadian National Railway (CN)

- 11.1.3 Canadian Pacific Kansas City (CPKC)

- 11.1.4 China Railway Freight

- 11.1.5 CSX Transportation

- 11.1.6 Deutsche Bahn (DB Cargo)

- 11.1.7 Indian Railways

- 11.1.8 Norfolk Southern Railway

- 11.1.9 Russian Railways (RZD)

- 11.1.10 Union Pacific Railroad

- 11.2 Regional players

- 11.2.1 Aurizon

- 11.2.2 Euro Cargo Rail

- 11.2.3 Ferromex

- 11.2.4 Genesee & Wyoming

- 11.2.5 Kansas City Southern

- 11.2.6 OBB Rail Cargo

- 11.2.7 PKP Cargo

- 11.3 Emerging players

- 11.3.1 Japan Freight Railway Company

- 11.3.2 SNCF Logistics

- 11.3.3 VTG