|

市場調查報告書

商品編碼

1998690

2026 年至 2035 年獸用抗生素和抗菌劑的市場機會、成長要素、產業趨勢分析和預測。Animal Antibiotics and Antimicrobials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

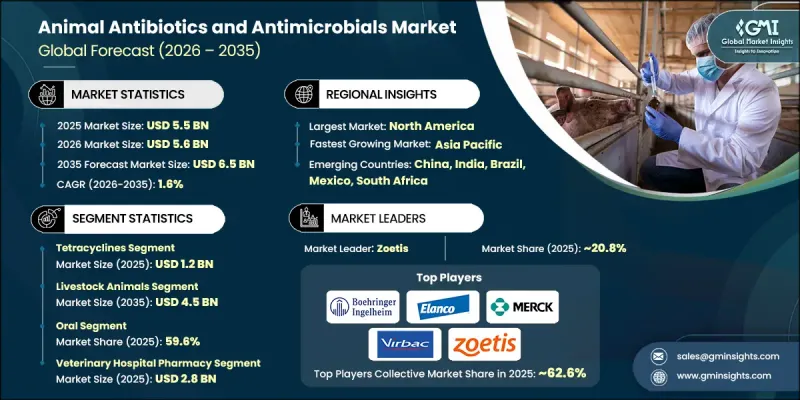

2025年全球動物抗生素和抗菌劑市場價值為55億美元,預計到2035年將以1.6%的複合年成長率成長至65億美元。

市場成長的促進因素包括動物性蛋白質需求的增加、牲畜感染疾病的蔓延以及人們對動物健康和生產力的日益關注。抗生素和抗菌劑在預防、控制和治療肉類及伴侶動物的細菌感染疾病方面發揮著至關重要的作用。集約化畜牧業的擴張,尤其是在家禽、豬和牛的養殖方面,顯著增加了對有效抗菌療法的需求,以降低死亡率並提高飼料轉換率。此外,農民對疾病預防和獸醫保健意識的提高也促進了全球市場的成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 55億美元 |

| 預計金額 | 65億美元 |

| 複合年成長率 | 1.6% |

新興國家獸醫基礎設施的完善和動物用藥品取得途徑的改善也影響市場成長。各國政府和監管機構日益重視動物疾病控制,以確保食品安全和公眾健康,這持續支撐獸用抗生素的需求。儘管針對抗菌素抗藥性(AMR)的監管日益嚴格,但標靶性和合理使用抗生素的研發正在推動市場穩步擴張。製劑技術和給藥方法的不斷進步也在提高療效的同時,最大限度地降低風險。

預計到2025年,四環黴素類抗生素市場規模將達到12億美元,主要得益於其頻譜抗菌活性、成本效益以及在畜牧業治療的廣泛應用。四環黴素常用於治療多種動物的呼吸道、消化器官系統和全身性感染疾病。其用途廣泛、劑型多樣(粉劑、注射劑、口服液等)以及已證實的臨床療效,使其成為獸醫和畜牧養殖戶的首選藥物。儘管法律規範不斷加大,但由於四環黴素抗生素在大規模畜牧場中具有良好的可靠性和易於給藥的特點,其市場需求仍然強勁。

預計到2035年,畜牧業市場規模將達到45億美元,主要得益於全球肉類、乳製品和雞蛋消費量的成長。畜牧養殖戶高度依賴抗生素和抗菌劑來維持牲畜健康、預防疾病爆發並確保穩定的生產力。隨著發展中地區畜牧業的工業化,制定疾病預防策略以最大限度減少經濟損失的需求日益成長。此外,對獸醫服務和畜牧技術的投入不斷增加,也進一步增強了畜牧業的競爭優勢。

亞太地區獸用抗生素和抗菌劑市場預計到2035年將以2.2%的複合年成長率成長,主要驅動力包括牲畜數量的快速成長、家禽生產的擴張以及對動物源性食品需求的不斷成長。中國和印度等國的成長尤其強勁,這得益於大規模農業生產和獸醫基礎設施的完善。該地區對糧食安全的日益重視以及動物疫病防治意識的提高,持續推動市場需求。此外,各國政府推出的有利於畜牧業健康計畫的舉措,也進一步鞏固了亞太地區在全球市場的主導地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 寵物飼養量增加

- 擴大畜牧業生產

- 研發經費的增加正在加速研究活動。

- 人們對動物保健意識的提高推動了對預防性治療的需求。

- 產業潛在風險與挑戰

- 治療的副作用

- 嚴格的監管要求

- 市場機遇

- 水產養殖業的擴張

- 數位化和遠程獸醫服務的廣泛應用

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 技術趨勢(基於初步調查)

- 當前技術趨勢

- 新興技術

- 未來市場趨勢(基於初步研究)

- 價格分析(基於初步調查)

- 供應鏈分析(基於初步研究)

- 波特五力分析

- 人工智慧和生成式人工智慧對市場的影響

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 青黴素

- 四環黴素

- 磺胺類藥物

- 大環內酯類

- Aminoglycosides

- 林可醯胺

- Fluoroquinolones

- 頭孢菌素

- 其他抗生素和抗菌產品

第6章 市場估計與預測:依動物種類分類,2022-2035年

- 家畜

- 牛

- 豬

- 家禽

- 魚

- 其他牲畜

- 伴侶動物

- 狗

- 貓

- 馬

- 其他伴侶動物

第7章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 外用

- 注射藥物

- 其他給藥途徑

第8章 市場估算與預測:依通路分類,2022-2035年

- 獸藥

- 普通藥房

- 電子商務

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AdvaCare Pharma

- Bimeda

- Boehringer Ingelheim

- Ceva Sante Animale

- Dechra Pharmaceuticals

- ECO Animal Health Group

- Elanco Animal Health Incorporated

- HIPRA

- Lutim Pharma Private Limited

- Meiji Holdings

- Merck

- Norbrook

- Phibro Animal Health

- Vetoquinol

- Virbac

- Zoetis

- Zydus(Zyvet Animal Health)

The Global Animal Antibiotics and Antimicrobials Market was valued at USD 5.5 billion in 2025 and is estimated to grow at a CAGR of 1.6% to reach USD 6.5 billion by 2035.

Market growth is driven by the rising demand for animal protein, the increasing prevalence of infectious diseases in livestock, and the growing emphasis on animal health and productivity. Antibiotics and antimicrobials play a critical role in preventing, controlling, and treating bacterial infections across food-producing and companion animals. The expansion of intensive livestock farming, particularly in poultry, swine, and cattle, has significantly increased the need for effective antimicrobial therapies to reduce mortality rates and improve feed efficiency. Additionally, rising awareness among farmers regarding disease prevention and veterinary care is further supporting market growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.5 Billion |

| Forecast Value | $6.5 Billion |

| CAGR | 1.6% |

The market growth is also influenced by evolving veterinary healthcare infrastructure and improved access to animal medicines in emerging economies. Governments and regulatory bodies are increasingly focusing on animal disease management to ensure food safety and public health, which continues to sustain demand for veterinary antimicrobials. While regulatory scrutiny around antimicrobial resistance (AMR) is tightening, the development of targeted and responsible-use antibiotics is supporting steady market expansion. Continuous advancements in formulation technologies and dosage delivery methods are also enhancing treatment efficacy while minimizing risks.

The tetracyclines segment generated USD 1.2 billion in 2025, owing to their broad-spectrum activity, cost-effectiveness, and widespread use in livestock treatment. Tetracyclines are commonly prescribed for respiratory, gastrointestinal, and systemic infections across multiple animal species. Their versatility, availability in multiple formulations such as powders, injectables, and oral solutions, and established clinical effectiveness make them a preferred choice among veterinarians and livestock producers. Despite increasing regulatory oversight, tetracyclines continue to maintain strong demand due to their proven reliability and ease of administration in large-scale farming operations.

The livestock segment is estimated to reach USD 4.5 billion by 2035, driven by the growing global consumption of meat, dairy, and eggs. Livestock producers rely heavily on antibiotics and antimicrobials to maintain herd health, prevent disease outbreaks, and ensure consistent productivity. Rising industrialization of animal farming, particularly in developing regions, has increased the need for disease prevention strategies to minimize economic losses. Additionally, growing investments in veterinary services and animal husbandry practices further strengthen the dominance of the livestock segment.

Asia Pacific Animal Antibiotics and Antimicrobials Market is estimated to grow at a CAGR of 2.2% through 2035, supported by rapid growth in livestock populations, expanding poultry production, and increasing demand for animal-derived food products. Countries such as China and India are witnessing strong growth due to large-scale farming operations and improving veterinary healthcare infrastructure. The region's increasing focus on food security, combined with rising awareness of animal disease management, continues to fuel demand. Additionally, favorable government initiatives supporting livestock health programs further reinforce Asia Pacific's leading position in the global market.

Key players operating in the Global Animal Antibiotics and Antimicrobials Market include Zoetis Inc., Elanco Animal Health, Boehringer Ingelheim, Merck & Co. (MSD Animal Health), Ceva Sante Animale, Virbac, Dechra Pharmaceuticals, Bayer AG, Vetoquinol, and Phibro Animal Health Corporation. These companies are actively expanding their veterinary portfolios, strengthening distribution networks, and investing in R&D to develop safer and more effective antimicrobial solutions. Companies in the animal antibiotics and antimicrobials market are focusing on responsible product innovation and portfolio diversification to strengthen their market presence. Leading players are investing in research and development to introduce targeted antibiotics with improved efficacy and reduced antimicrobial resistance risks. Strategic partnerships with veterinary clinics, livestock producers, and regional distributors help expand market reach and improve product accessibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Animal type trends

- 2.2.4 Mode of delivery trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

- 2.4.1 Future outlook

- 2.4.2 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing pet ownership rate

- 3.2.1.2 Expanding livestock production

- 3.2.1.3 Rise in R&D funding accelerating the research efforts

- 3.2.1.4 Growing awareness for animal healthcare spurring demand for preventive treatment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects of treatments

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of aquaculture sector

- 3.2.3.2 Growing adoption of digital and tele-veterinary services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Pricing analysis (Driven by Primary Research)

- 3.8 Supply chain analysis (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 Impact of AI and generative AI on the market

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Penicillins

- 5.3 Tetracyclines

- 5.4 Sulfonamides

- 5.5 Macrolides

- 5.6 Aminoglycosides

- 5.7 Lincosamides

- 5.8 Fluoroquinolones

- 5.9 Cephalosporins

- 5.10 Other antibiotics and antimicrobial products

Chapter 6 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Livestock animals

- 6.2.1 Cattle

- 6.2.2 Swine

- 6.2.3 Poultry

- 6.2.4 Fish

- 6.2.5 Other livestock animals

- 6.3 Companion animals

- 6.3.1 Dogs

- 6.3.2 Cats

- 6.3.3 Horses

- 6.3.4 Other companion animals

Chapter 7 Market Estimates and Forecast, By Mode of Delivery, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Topical

- 7.4 Injections

- 7.5 Other modes of delivery

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospital pharmacy

- 8.3 Retail pharmacy

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AdvaCare Pharma

- 10.2 Bimeda

- 10.3 Boehringer Ingelheim

- 10.4 Ceva Sante Animale

- 10.5 Dechra Pharmaceuticals

- 10.6 ECO Animal Health Group

- 10.7 Elanco Animal Health Incorporated

- 10.8 HIPRA

- 10.9 Lutim Pharma Private Limited

- 10.10 Meiji Holdings

- 10.11 Merck

- 10.12 Norbrook

- 10.13 Phibro Animal Health

- 10.14 Vetoquinol

- 10.15 Virbac

- 10.16 Zoetis

- 10.17 Zydus (Zyvet Animal Health)

獸用抗生素和抗菌劑市場:按類型、動物種類、給藥途徑、劑型、最終用戶和配銷通路分類-2026-2032年全球市場預測

獸用抗生素和抗菌劑市場:按類型、動物種類、給藥途徑、劑型、最終用戶和配銷通路分類-2026-2032年全球市場預測 活體動物市場規模、佔有率和成長分析:按動物類型、應用、健康狀況/等級、分銷管道和地區分類-2026-2033年產業預測

活體動物市場規模、佔有率和成長分析:按動物類型、應用、健康狀況/等級、分銷管道和地區分類-2026-2033年產業預測 2026-2034年全球獸用抗生素和抗菌劑市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球獸用抗生素和抗菌劑市場規模、佔有率、趨勢和成長分析報告 動物用抗生素和抗菌藥物市場分析及預測(至2035年):類型、產品類型、應用、劑型、最終用戶、技術、功能、階段

動物用抗生素和抗菌藥物市場分析及預測(至2035年):類型、產品類型、應用、劑型、最終用戶、技術、功能、階段 動物服裝市場-全球產業規模、佔有率、趨勢、機會和預測:按動物類型、材料、分銷管道、地區和競爭格局分類,2021-2031年雄烯二酮原料藥市場按產品類型、純度等級、劑型、通路、應用及最終用戶分類,全球預測,2026-2032年雄烯二酮及其衍生物市場依產品類型、衍生物、應用、通路及最終用戶分類-2026-2032年全球預測

動物服裝市場-全球產業規模、佔有率、趨勢、機會和預測:按動物類型、材料、分銷管道、地區和競爭格局分類,2021-2031年雄烯二酮原料藥市場按產品類型、純度等級、劑型、通路、應用及最終用戶分類,全球預測,2026-2032年雄烯二酮及其衍生物市場依產品類型、衍生物、應用、通路及最終用戶分類-2026-2032年全球預測 獸用抗生素和抗菌劑市場規模、佔有率和成長分析(按類型、劑型、動物和地區分類)—產業預測(2026-2033 年)動物抗生素和抗菌藥物市場-全球產業規模、佔有率、趨勢、機會和預測,按產品、給藥方式、動物類型、地區和競爭格局分類,2020-2030年預測2024 年至 2031 年全球動物抗生素和抗生素市場(按產品、動物類型、交付方式和地區劃分)

獸用抗生素和抗菌劑市場規模、佔有率和成長分析(按類型、劑型、動物和地區分類)—產業預測(2026-2033 年)動物抗生素和抗菌藥物市場-全球產業規模、佔有率、趨勢、機會和預測,按產品、給藥方式、動物類型、地區和競爭格局分類,2020-2030年預測2024 年至 2031 年全球動物抗生素和抗生素市場(按產品、動物類型、交付方式和地區劃分)