|

市場調查報告書

商品編碼

1998683

電動車充電管理軟體平台市場機會、成長要素、產業趨勢分析及2026-2035年預測EV Charging Management Software Platform Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

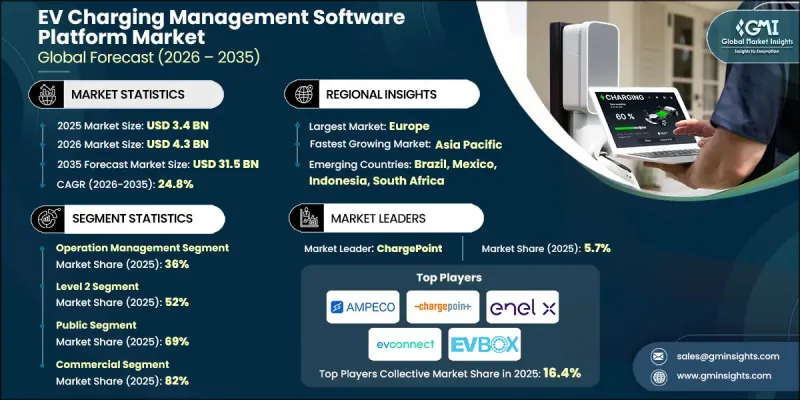

2025 年全球電動車充電管理軟體平台市場價值為 34 億美元,預計到 2035 年將達到 315 億美元,年複合成長率為 24.8%。

隨著電動車在多個地區普及速度加快,全球電動車充電管理軟體平台產業正迅速擴張。隨著電動車基礎設施的擴展,對能夠管理複雜充電網路的集中式數位平台的需求日益成長。這些軟體平台使營運商能夠監控充電活動、管理收費系統、驗證用戶身份,並在各種充電環境中平衡電力負荷。住宅、商業和車隊環境中充電基礎設施的持續部署,催生了對確保可靠且有效運作的整合管理系統的強勁需求。支持向清潔交通途徑轉型的公共也透過加速電動車充電網路的擴張,促進了市場成長。隨著各國政府和組織加強減少碳排放並促進永續能源利用,支持能源最佳化和排放監測的軟體平台的重要性日益凸顯。連接性和數位基礎設施的技術進步,透過實現即時分析、預測性維護和遠距離診斷,進一步增強了電動車充電平台的功能。與智慧型能源網路和先進電網系統的整合,使充電運營商能夠更有效地管理分散式充電資產。這些發展趨勢共同支撐了全球電動車充電管理軟體平台市場的長期成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 34億美元 |

| 預測金額 | 315億美元 |

| 複合年成長率 | 24.8% |

預計到2025年,營運管理細分市場將佔36%的市場佔有率,並在2026年至2035年間以24.1%的複合年成長率成長。營運管理軟體透過對充電網路進行集中控制和監控,在確保電動車充電基礎設施的平穩運作方面發揮著至關重要的作用。這些解決方案使營運商能夠即時監控充電站的效能,安排充電時段,並控制多個充電點之間的能量分配。該軟體還能在技術故障發生時發出警報,幫助營運商及早發現營運問題,從而快速啟動維護工作。這些平台提供的詳細效能分析功能,使充電網路營運商能夠評估充電站的利用率,最佳化營運效率,並維持高服務可用性。

預計到2025年,公共市佔率將達到69%,並在2026年至2035年間以25.3%的複合年成長率成長。公共充電基礎設施需要複雜的軟體平台來管理各種營運功能,包括用戶身份驗證、交易處理、充電會話監控以及不同充電服務供應商之間的網路互通性。該軟體平台還有助於營運商管理充電樁的功率負載,防止系統過載,並維持穩定的網路效能。隨著公共充電基礎設施的擴展,數位化工具正被擴大用於支援彈性價格設定模式和預約充電服務等功能。這些功能使營運商能夠更有效地管理充電站容量,同時提升用戶的整體充電體驗。

預計2025年,美國電動車充電管理軟體平台市場規模將達6.806億美元。在美國,電動車的日益普及推動了先進軟體平台的發展,這些平台旨在最佳化充電操作和降低能源消耗。全國範圍內的充電網路正擴大採用智慧調度系統,該系統能夠根據電價波動調整充電收費系統。這些功能有助於降低充電營運商和電動車車主的營運成本,同時最大限度地減少電網負載。隨著電動車用戶數量的成長,海量的營運和交易數據被產生,使得資料安全和用戶隱私成為網路營運商的重中之重。因此,各公司正在投資先進的網路安全技術,以確保安全的身份驗證和加密的交易系統。能源供應商、技術開發人員和基礎設施營運商之間的合作也促進了美國電動車充電管理軟體平台產業先進電動車充電軟體平台的持續發展。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電動車(EV)的廣泛普及

- 政府政策和獎勵

- 專注於永續性和能源最佳化

- 與智慧電網和數位技術的融合

- 產業潛在風險與挑戰

- 前期成本高,實施過程複雜。

- 互通性和標準化的障礙

- 市場機遇

- 向新興地區擴張

- 可再生能源與輸配電網路服務的整合

- 人工智慧與預測分析的整合

- 生態系內的夥伴關係與互通服務

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國能源局

- SAE國際/美國國家標準協會(ANSI)

- 歐洲

- 歐盟委員會

- CharIN/Eurovent Certita Certification

- 亞太地區

- 新加坡建設局 (BCA)

- JIS-日本工業標準

- 拉丁美洲

- 巴西技術標準協會

- 國家能源委員會

- 中東和非洲

- 阿拉伯聯合大公國(阿拉伯聯合大公國)能源與基礎設施部

- 沙烏地阿拉伯標準、計量和品質組織

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按球員類型分類的定價策略(高階/超值/成本加成)

- 成本細分分析

- 專利分析(基於初步研究)

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 關於碳足跡的考量

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 細分市場生成式人工智慧用例和實施藍圖

- 風險、限制和監管考量

- 基礎設施和實施情況(基於初步調查)

- 按地區和購買者群體分類的採用率和滲透率

- 基礎設施投資的可擴展性限制和趨勢

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估算與預測:依模組分類,2022-2035年

- 營運管理

- 能源管理

- 帳單和付款

- 其他

第6章 市場估算與預測:以收費方式分類,2022-2035年

- 一級

- 二級

- 3級

第7章 市場估價與預測:以充電地點分類,2022-2035年

- 公共

- 私人的

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 商業的

- 住宅

第9章 市場估計與預測:依最終用途分類,2022-2035年

- 充電樁運營商 (CPO)

- 車隊營運商

- 物業所有者和管理者

- 公共產業和能源公司

- 汽車製造商和經銷商

- 電動旅遊服務供應商(eMSP)

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 波蘭

- 羅馬尼亞

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 世界公司

- ABB

- Blink Charging

- Bosch

- ChargePoint

- Driivz

- Enel X

- EVBox

- Schneider Electric

- Shell Recharge Solutions

- Siemens

- Tesla

- 當地公司

- Ampeco

- AmpUp

- ChargeLab

- Current

- EV Connect

- Greenlots

- Pod Point

- Virta

- 新興企業

- Lincoln

- ElectreeFi

- Landis+Gyr

- Touch

The Global EV Charging Management Software Platform Market was valued at USD 3.4 billion in 2025 and is estimated to grow at a CAGR of 24.8% to reach USD 31.5 billion by 2035.

The global EV charging management software platform industry is witnessing rapid expansion as electric vehicle adoption accelerates across multiple regions. As EV infrastructure grows, there is an increasing requirement for centralized digital platforms capable of managing complex charging networks. These software platforms enable operators to monitor charging activities, manage billing systems, authenticate users, and balance energy loads across different types of charging environments. The increasing deployment of charging infrastructure in residential, commercial, and fleet environments is creating strong demand for integrated management systems that ensure reliable and efficient operation. Public policies supporting the transition toward cleaner transportation are also contributing to market growth by encouraging the expansion of EV charging networks. As governments and organizations intensify their efforts to reduce carbon emissions and promote sustainable energy use, software platforms that support energy optimization and emissions monitoring are gaining greater importance. Technological advancements in connectivity and digital infrastructure are further strengthening the capabilities of EV charging platforms by enabling real-time analytics, predictive maintenance, and remote diagnostics. Integration with smart energy networks and advanced grid systems is allowing charging operators to manage distributed charging assets more effectively. These developments are collectively supporting the long-term growth of the EV charging management software platform market worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.4 Billion |

| Forecast Value | $31.5 Billion |

| CAGR | 24.8% |

The operation management segment accounted for 36% share in 2025 and is expected to grow at a CAGR of 24.1% from 2026 to 2035. Operation management software plays a critical role in ensuring the smooth functioning of EV charging infrastructure by providing centralized control and oversight of charging networks. These solutions allow operators to monitor station performance in real time, schedule charging sessions, and control energy distribution across multiple charging points. The software also enables early detection of operational issues by generating alerts when technical faults occur, helping operators initiate maintenance activities quickly. Detailed performance analytics provided by these platforms allow charging network operators to evaluate station utilization, optimize operational efficiency, and maintain high service availability.

The public segment held 69% share in 2025 and is projected to grow at a CAGR of 25.3% between 2026 and 2035. Public charging infrastructure requires advanced software platforms to manage a wide range of operational functions. These include user authentication, transaction processing, charging session monitoring, and network interoperability across different charging service providers. Software platforms also help operators manage electricity loads across charging points to prevent system overloads and maintain stable network performance. As public charging infrastructure expands, digital tools are increasingly used to support features such as flexible pricing models and reservation-based charging services. These capabilities allow operators to manage station capacity more efficiently while improving the overall charging experience for users.

US EV Charging Management Software Platform Market reached USD 680.6 million in 2025. In the United States, increasing EV adoption is encouraging the development of advanced software platforms that optimize charging operations and energy consumption. Charging networks across the country are increasingly integrating intelligent scheduling systems that allow charging sessions to adapt to variable electricity pricing structures. These capabilities help reduce operational costs for charging operators and EV owners while also minimizing strain on the electricity grid. The growing number of EV users is generating large volumes of operational and payment data, making data security and user privacy a critical priority for network operators. As a result, companies are investing in advanced cybersecurity technologies to ensure secure authentication and encrypted transaction systems. Collaboration between energy providers, technology developers, and infrastructure operators is also supporting the continued development of sophisticated EV charging software platforms across the US EV charging management software platform industry.

Major companies operating in the Global EV Charging Management Software Platform Market include ABB, Ampeco, Blink Charging, ChargePoint, Driivz, Enel X, EVBox, Schneider Electric, Shell Recharge Solutions, Siemens, and Tesla. Companies active in the Global EV Charging Management Software Platform Market are adopting several strategic initiatives to strengthen their competitive position and expand their technological capabilities. A primary strategy involves continuous investment in research and development to enhance software functionalities such as real-time analytics, predictive maintenance, and advanced energy management features. Many companies are also focusing on expanding cloud-based platforms that support scalable and interoperable charging network management. Strategic partnerships with energy providers, mobility service companies, and infrastructure developers are helping software providers integrate their platforms into larger transportation and energy ecosystems. Additionally, companies are enhancing cybersecurity frameworks and data protection systems to safeguard sensitive user information.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Module

- 2.2.3 Charging type

- 2.2.4 Charging site

- 2.2.5 Application

- 2.2.6 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of electric vehicles (EVs)

- 3.2.1.2 Government policies & incentives

- 3.2.1.3 Focus on sustainability & energy optimization

- 3.2.1.4 Integration with smart grid & digital technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial costs & complex implementation

- 3.2.2.2 Interoperability & standardization barriers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging regions

- 3.2.3.2 Renewable energy & grid services integration

- 3.2.3.3 AI and predictive analytics integration

- 3.2.3.4 Ecosystem partnerships & interoperable services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Department of Energy

- 3.4.1.2 SAE International / American National Standards Institute (ANSI)

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 CharIN / Eurovent Certita Certification

- 3.4.3 Asia Pacific

- 3.4.3.1 BCA - Building and Construction Authority (Singapore)

- 3.4.3.2 JIS - Japanese Industrial Standards

- 3.4.4 Latin America

- 3.4.4.1 Associacao Brasileira de Normas Tecnicas

- 3.4.4.2 Comision Nacional de Energia

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Ministry of Energy and Infrastructure

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing Analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Infrastructure & deployment landscape (driven by primary research)

- 3.13.1 Deployment penetration by region & buyer segment

- 3.13.2 Scalability constraints & infrastructure investment trends

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Module, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Operation management

- 5.3 Energy management

- 5.4 Billing & payment

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Charging Type, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Level 1

- 6.3 Level 2

- 6.4 Level 3

Chapter 7 Market Estimates & Forecast, By Charging Site, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Public

- 7.3 Private

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Residential

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Charge point operators (CPOs)

- 9.3 Fleet operators

- 9.4 Property owners & managers

- 9.5 Utilities & energy companies

- 9.6 Automotive OEMs & dealerships

- 9.7 eMobility service providers (eMSPs)

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 ABB

- 11.1.2 Blink Charging

- 11.1.3 Bosch

- 11.1.4 ChargePoint

- 11.1.5 Driivz

- 11.1.6 Enel X

- 11.1.7 EVBox

- 11.1.8 Schneider Electric

- 11.1.9 Shell Recharge Solutions

- 11.1.10 Siemens

- 11.1.11 Tesla

- 11.2 Regional players

- 11.2.1 Ampeco

- 11.2.2 AmpUp

- 11.2.3 ChargeLab

- 11.2.4 Current

- 11.2.5 EV Connect

- 11.2.6 Greenlots

- 11.2.7 Pod Point

- 11.2.8 Virta

- 11.3 Emerging players

- 11.3.1 Lincoln

- 11.3.2 ElectreeFi

- 11.3.3 Landis+Gyr

- 11.3.4 Touch

電動車充電軟體平台市場預測至2034年—按組件、車輛類型、部署模式、最終用戶和地區分類的全球分析電動車充電市場分析與預測(至2034年)-全球分析,依充電器類型、充電方式、安裝配置、連接器類型、充電等級、連接方式、操作方式、應用領域與地區分類

電動車充電軟體平台市場預測至2034年—按組件、車輛類型、部署模式、最終用戶和地區分類的全球分析電動車充電市場分析與預測(至2034年)-全球分析,依充電器類型、充電方式、安裝配置、連接器類型、充電等級、連接方式、操作方式、應用領域與地區分類 電動車充電站軟體市場:按軟體類型、部署模式、充電站類型、最終用戶和應用分類-2026-2032年全球市場預測

電動車充電站軟體市場:按軟體類型、部署模式、充電站類型、最終用戶和應用分類-2026-2032年全球市場預測 電動車充電軟體市場:依模組、部署類型和最終用戶(充電樁運營商、電動旅行服務提供商、車隊運營商及其他)劃分 - 全球預測至 2036 年

電動車充電軟體市場:依模組、部署類型和最終用戶(充電樁運營商、電動旅行服務提供商、車隊運營商及其他)劃分 - 全球預測至 2036 年 2026年全球電動車充電人工智慧市場報告

2026年全球電動車充電人工智慧市場報告 電動車充電管理軟體平台市場:預測(2025-2030)

電動車充電管理軟體平台市場:預測(2025-2030) 電動車充電管理軟體平台的全球市場

電動車充電管理軟體平台的全球市場 電動車充電軟體市場,按充電器類型、充電站、車輛類型和地區 - 2024-2032 年產業分析、市場規模、市場佔有率和預測

電動車充電軟體市場,按充電器類型、充電站、車輛類型和地區 - 2024-2032 年產業分析、市場規模、市場佔有率和預測 電動車充電基礎設施 (EVCI) 軟體的全球市場的分析 (2024年前半期)

電動車充電基礎設施 (EVCI) 軟體的全球市場的分析 (2024年前半期) 全球電動車充電軟體市場規模研究,按充電站點(公共、私人)、充電器類型(1 級、2 級、3 級)、車輛類型(E-2Wheeler、E-3Wheeler、E-car Personal、E) -汽車商業)和2022-2032 年區域預測

全球電動車充電軟體市場規模研究,按充電站點(公共、私人)、充電器類型(1 級、2 級、3 級)、車輛類型(E-2Wheeler、E-3Wheeler、E-car Personal、E) -汽車商業)和2022-2032 年區域預測