|

市場調查報告書

商品編碼

1998680

腎結石治療市場:商機、成長要素、產業趨勢分析及2026-2035年預測Kidney Stone Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

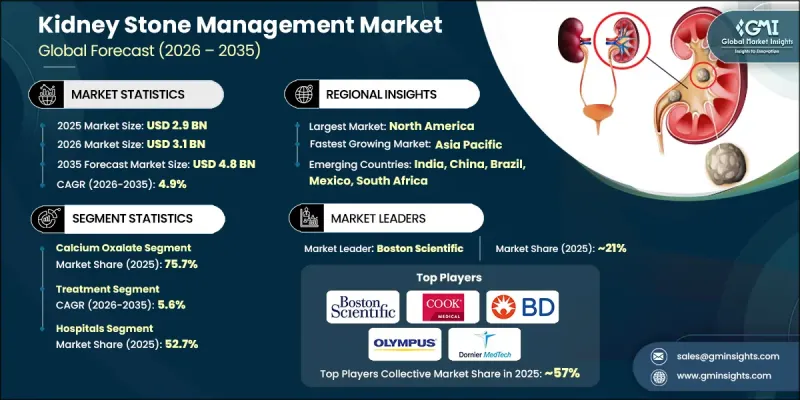

2025 年全球腎結石治療市場價值 29 億美元,預計到 2035 年將達到 48 億美元,年複合成長率為 4.9%。

腎結石治療市場的成長主要受以下因素驅動:全球腎結石發病率的上升、治療技術的不斷進步以及人口老化的持續加劇。醫療專業人員發現泌尿系統疾病患者數量不斷增加,這導致對可靠的診斷工具和有效的治療方案的需求日益成長。醫療技術的進步提高了結石檢測的準確性,同時也提升了治療效率和病人安全性。此外,微創治療的普及正在改變治療方式,縮短恢復時間並降低手術風險。醫院和專科診所擴大採用最新的醫療設備和先進的手術技術,以改善臨床療效並最佳化病患管理。此外,數位診斷和影像技術的融合使醫療專業人員能夠更早發現腎結石並制定更精準的治療策略。這些進步共同推動了腎結石治療市場的穩定成長,同時也提升了患者照護的整體品質。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 29億美元 |

| 預計金額 | 48億美元 |

| 複合年成長率 | 4.9% |

腎結石的治療包括透過影像學檢查、藥物治療以及微創或外科手術等手段進行識別、治療和長期管理。這些干預措施的主要目標是緩解症狀、清除或碎石、預防復發以及恢復正常的泌尿系統功能。輸尿管鏡檢查、雷射碎石術、體外震波碎石術和經皮手術等技術的進步顯著提高了治療效果。這些進步使臨床醫生能夠以更小的併發症實施更精準的手術。此外,隨著醫療機構擴大採用微創手術和門診手術方案,該行業正經歷快速成長。

預計到2025年,草酸鈣結石市佔率將達到75.7%。該細分市場的主導地位主要歸因於此類腎結石的高發病率及其與代謝和飲食風險因素的密切關聯。確診患有此病的患者通常需要反覆後續觀察和醫療干預,從而導致對診斷和治療方案的持續需求。由於此類腎結石容易復發,醫療專業人員強調包括飲食指導、藥物治療和定期後續觀察的長期管理策略。因此,此類結石的高發生率和易復發性持續推動著腎結石治療市場中草酸鈣結石細分市場的成長。

預計到2025年,腎結石治療市場規模將達到17億美元,並在2026年至2035年間以5.6%的複合年成長率成長。全球腎結石發生率的不斷上升,尤其是復發病例的增加,推動了對治療性介入的需求成長。由於疾病的複發性,需要即時治療和持續的患者管理,導致全球醫療程序數量顯著增加。此外,診斷技術的進步使醫療專業人員能夠更早發現結石並更精確地確定其位置。影像能力的提升使得治療方案的發展更加精準,有助於改善臨床療效。這些進步增強了醫師對現代治療方法的信心,同時也提高了醫療機構的診療效率。

預計到2025年,美國腎結石治療市場規模將達12億美元。全國範圍內腎結石的高發病率持續推動著對外科手術和預防保健方案的穩定需求。相當一部分患者會出現結石復發,需要持續監測和多次治療性介入。這一趨勢促進了市場的持續活力,並推動了對先進醫療技術需求的成長。美國擁有完善的醫療保健基礎設施,包括配備先進體外震波碎石機、輸尿管鏡設備和雷射治療技術的醫院和門診手術中心,這也為市場發展提供了有利條件。先進的影像系統有助於早期發現疾病並改善治療方案。隨著醫療機構不斷優先採用微創技術,整個醫療系統的治療效率和病患處理能力也穩定提升。

主要企業正積極實施各項策略性舉措,以鞏固市場地位並拓展全球業務。主要企業正大力投資研發,力求推出技術先進的治療系統,進而提高手術精準度並改善病患預後。許多企業也致力於產品創新,將更強大的成像功能、數位化連接和先進的雷射技術整合到醫療設備中。與醫療機構和技術供應商建立策略合作夥伴關係,有助於企業加速產品開發,並擴大臨床應用範圍。此外,透過夥伴關係和銷售協議進入新興醫療市場,企業可以拓展其先進治療方案的管道。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策和資料完整性計劃

- 資訊來源一致性通訊協定

- GMI人工智慧政策和資料完整性計劃

- 調查過程和可靠性評分

- 調查過程的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 腎結石發生率和復發率增加

- 微創治療的技術進步

- 體外震波碎石術的保險報銷優惠

- 人們對腎臟健康的整體認知不斷提高

- 產業潛在風險與挑戰

- 先進醫療設備高成本

- 體外震波碎石術的潛在長期副作用

- 市場機遇

- 新興市場的擴張

- 遠端醫療和遠端患者監護的發展

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 科技趨勢

- 當前技術趨勢

- 新興技術

- 救贖方案

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

- 價值鏈分析

- 客戶洞察

- Start-Ups場景

- 差距分析

- 人工智慧和生成式人工智慧對市場的影響

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依腎結石類型分類,2022-2035年

- 草酸鈣

- 鳥糞石

- 尿酸

- 磷酸鈣

- 半胱胺酸

第6章 市場估計與預測:依類別分類,2022-2035年

- 治療

- 體外震波碎石術(ESWL)

- 輸尿管鏡檢查

- 經皮腎鏡取石術(PCNL)

- 其他治療方法

- 診斷

- 電腦斷層掃描

- 超音波檢查

- 腹部X光檢查

- 靜脈腎盂造影

- 腹部磁振造影

- 其他診斷方法

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 專科診所

- 門診手術中心

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Allengers

- Becton, Dickinson and Company

- Boston Scientific

- Coloplast

- COOK MEDICAL

- DirexGroup

- Dornier MedTech

- ELMED Medical Systems

- EMS ELECTRO MEDICAL SYSTEMS

- KARL STORZ

- MEDISPEC

- OLYMPUS

- PolyDiagnost

- Richard Wolf

- SIEMENS Healthineers

The Global Kidney Stone Management Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 4.8 billion by 2035.

Growth in the kidney stone management market is supported by the increasing global incidence of kidney stone disorders, continuous advancements in treatment technologies, and the steady rise in the aging population. Healthcare providers are witnessing higher patient volumes associated with urinary tract disorders, which is intensifying the demand for reliable diagnostic tools and effective treatment solutions. Medical technology advancements are improving the accuracy of stone detection while also enhancing treatment efficiency and patient safety. Additionally, the shift toward minimally invasive therapeutic approaches is transforming the treatment landscape by offering shorter recovery times and reduced procedural risks. Hospitals and specialty clinics are increasingly adopting modern devices and advanced procedural techniques designed to improve clinical outcomes and optimize patient management. Furthermore, the integration of digital diagnostics and imaging technologies is enabling healthcare professionals to identify kidney stones earlier and plan more precise treatment strategies. Collectively, these developments are driving steady expansion of the kidney stone management market while improving the overall quality of patient care.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 4.9% |

Kidney stone management involves the identification, treatment, and long-term control of renal calculi through diagnostic imaging, medical therapy, and minimally invasive or surgical procedures. The primary objective of these interventions is to relieve symptoms, eliminate or break down stones, prevent recurrence, and restore normal urinary system function. Advancements in technologies used for ureteroscopy, laser-based stone fragmentation, extracorporeal shock wave lithotripsy, and percutaneous procedures have significantly enhanced treatment effectiveness. These improvements allow clinicians to perform procedures with greater precision while minimizing complications. The industry is also experiencing rapid growth as healthcare facilities expand their adoption of minimally invasive procedures and ambulatory surgical solutions.

The calcium oxalate segment held 75.7% share in 2025. The segment's leadership is largely attributed to the widespread occurrence of this type of kidney stone and its strong association with metabolic and dietary risk factors. Patients diagnosed with this condition often require repeated monitoring and medical intervention, which contributes to sustained demand for diagnostic and treatment solutions. Because this type of kidney stone frequently recurs, healthcare providers emphasize long-term management strategies that include dietary guidance, medical therapy, and routine monitoring. The high prevalence and recurrent nature of these stones, therefore, continue to support the growth of the calcium oxalate segment within the kidney stone management market.

The treatment segment generated USD 1.7 billion in 2025 and is expected to grow at a CAGR of 5.6% during 2026-2035. The increasing global incidence of kidney stone disease, particularly cases involving recurrence, is driving greater demand for therapeutic interventions. The recurring nature of the condition requires both immediate treatment procedures and continuous patient management, which significantly increases the volume of medical procedures performed worldwide. In addition, improvements in diagnostic technologies are enabling healthcare providers to detect stones at earlier stages and determine their exact location more accurately. Enhanced imaging capabilities support more precise treatment planning and improve clinical outcomes. These developments are increasing physician confidence in modern treatment methods while also contributing to higher procedural efficiency across healthcare facilities.

U.S. Kidney Stone Management Market reached USD 1.2 billion in 2025. The high occurrence of kidney stone disorders across the country continues to create consistent demand for both surgical procedures and preventive care solutions. A considerable portion of patients experience recurrent stone formation, which requires ongoing monitoring and multiple treatment interventions. This pattern contributes to sustained market activity and increased demand for advanced medical technologies. The United States also benefits from a well-developed healthcare infrastructure that includes hospitals and ambulatory surgical centers equipped with advanced lithotripsy systems, ureteroscopy devices, and laser-based treatment technologies. Access to sophisticated diagnostic imaging systems supports earlier disease detection and improved treatment planning. As healthcare providers continue to prioritize minimally invasive techniques, treatment efficiency and patient throughput are steadily improving across the healthcare system.

Several leading companies participate in the Global Kidney Stone Management Market, including Allengers, Becton, Dickinson and Company, Boston Scientific, Coloplast, COOK MEDICAL, DirexGroup, Dornier MedTech, ELMED Medical Systems, EMS ELECTRO MEDICAL SYSTEMS, KARL STORZ, MEDISPEC, OLYMPUS, PolyDiagnost, Richard Wolf, and SIEMENS Healthineers. Companies operating in the Global Kidney Stone Management Market are implementing a range of strategic initiatives to strengthen their market presence and expand their global footprint. Leading manufacturers are heavily investing in research and development to introduce technologically advanced treatment systems that enhance procedural precision and patient outcomes. Many firms are also focusing on product innovation by integrating improved imaging capabilities, digital connectivity, and advanced laser technologies into their medical devices. Strategic collaborations with healthcare institutions and technology providers are helping companies accelerate product development and broaden clinical adoption. Additionally, expansion into emerging healthcare markets through partnerships and distribution agreements is allowing companies to increase accessibility to advanced treatment solutions.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Stone type trends

- 2.2.3 Category trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence and recurrence rate of kidney stones

- 3.2.1.2 Technological advancements in minimally invasive treatments

- 3.2.1.3 Favourable reimbursement for lithotripsy procedures

- 3.2.1.4 Rising awareness regarding overall kidney health

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced treatment devices

- 3.2.2.2 Potential long-term adverse effects of lithotripsy

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Growth of telemedicine and remote patient monitoring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Value chain analysis

- 3.11 Customer insights

- 3.12 Start-up scenarios

- 3.13 Gap analysis

- 3.14 Impact of AI and generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Stone Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Calcium oxalate

- 5.3 Struvite

- 5.4 Uric acid

- 5.5 Calcium phosphate

- 5.6 Cysteine

Chapter 6 Market Estimates and Forecast, By Category, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Treatment

- 6.2.1 Extracorporeal shock wave lithotripsy (ESWL)

- 6.2.2 Ureteroscopy

- 6.2.3 Percutaneous nephrolithotomy (PCNL)

- 6.2.4 Other treatments

- 6.3 Diagnostics

- 6.3.1 Computed tomography

- 6.3.2 Ultrasound

- 6.3.3 Abdominal x-ray

- 6.3.4 Intravenous pyelography

- 6.3.5 Abdominal MRI

- 6.3.6 Other diagnostics

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Ambulatory surgical centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Allengers

- 9.2 Becton, Dickinson and Company

- 9.3 Boston Scientific

- 9.4 Coloplast

- 9.5 COOK MEDICAL

- 9.6 DirexGroup

- 9.7 Dornier MedTech

- 9.8 ELMED Medical Systems

- 9.9 EMS ELECTRO MEDICAL SYSTEMS

- 9.10 KARL STORZ

- 9.11 MEDISPEC

- 9.12 OLYMPUS

- 9.13 PolyDiagnost

- 9.14 Richard Wolf

- 9.15 SIEMENS Healthineers

2026年全球腎結石清除設備市場報告

2026年全球腎結石清除設備市場報告 全球腎結石清除設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球腎結石清除設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球石材搬運籃市場-產業規模、佔有率、趨勢、機會及預測:按類型、形狀、先進技術、最終用戶、地區和競爭格局分類,2021-2031年全球腎結石治療市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034)

全球石材搬運籃市場-產業規模、佔有率、趨勢、機會及預測:按類型、形狀、先進技術、最終用戶、地區和競爭格局分類,2021-2031年全球腎結石治療市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034) 腎結石治療市場規模、佔有率及成長分析(按類型、治療方法、診斷、最終用戶和地區分類)-2026-2033年產業預測腎結石取出器材市場-全球產業規模、佔有率、趨勢、機會和預測,依方法、原因、類型、最終用戶(醫院、門診手術中心及其他)、地區和競爭格局分類,2020-2030年預測2025年全球腎結石管理市場報告

腎結石治療市場規模、佔有率及成長分析(按類型、治療方法、診斷、最終用戶和地區分類)-2026-2033年產業預測腎結石取出器材市場-全球產業規模、佔有率、趨勢、機會和預測,依方法、原因、類型、最終用戶(醫院、門診手術中心及其他)、地區和競爭格局分類,2020-2030年預測2025年全球腎結石管理市場報告 全球腎結石取出設備市場全球去石籃市場

全球腎結石取出設備市場全球去石籃市場 2025-2029年全球腎結石藥物市場

2025-2029年全球腎結石藥物市場