|

市場調查報告書

商品編碼

1998666

智慧播種機市場機會、成長要素、產業趨勢分析及2026-2035年預測Smart Seed Planting Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

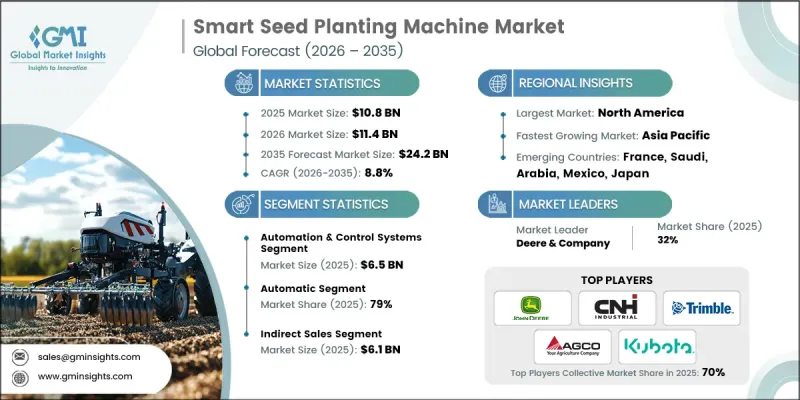

全球智慧播種機市場預計到 2025 年價值 108 億美元,預計到 2035 年將以 8.8% 的複合年成長率成長至 242 億美元。

智慧播種機市場在智慧農業設備領域的擴張主要源自於人們對提高農業生產力和最佳化作業效率日益成長的需求。農民擴大採用先進設備,這些設備能夠實現數據驅動的決策,使他們能夠透過評估土壤品質、田間差異、水分分佈和種子特性等因素來確定理想的播種條件。隨著先進數位平台、感測技術和自動化系統的普及,精密農業工具的取得也日益便利。因此,農民們意識到,更精準的播種能夠顯著提高發芽率,減少投入浪費,並帶來更穩定的產量。此外,數位化農業解決方案的整合正在改變播種作業,從而帶來更穩定、更可預測的成果。隨著農場作業的現代化以及對技術主導農業管理的持續依賴,對智慧播種機的需求預計將穩定成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 108億美元 |

| 預測金額 | 242億美元 |

| 複合年成長率 | 8.8% |

環境條件的變化進一步降低了依賴估算而非數據驅動洞察的傳統播種方法的可靠性。精準播種系統提供了一種可靠的替代方案,能夠在各種田間條件下提供穩定的性能。這些機器使農民能夠持續監測播種效率,自動調整機器設置,並保存詳細的田間記錄,從而支持改進規劃和製定長期作業策略。向精密農業的轉變代表著現代農業實踐的重大變革,它使種植者能夠更好地控制播種作業,並實現更有效率的農業資源管理。

到2025年,自動化控制系統的市場規模將達到65億美元。現代智慧播種設備高度依賴自動化控制技術,以確保種子播種的精準性和均勻性。這些系統結合了數位種子稱重裝置、電子控制執行器、即時可程式設計控制單元以及機器間通訊平台,用於調整種子位置、播種深度和行距的均勻性。透過自動化關鍵操作參數,這些技術減少了人工干預造成的誤差,並提高了作物播種的均勻性。自動化控制系統的另一個重要優勢在於其能夠與先進的監控技術整合,使機器能夠接收來自田間的即時回饋並據此調整作業。

到2025年,自動化播種機將佔據79%的市場。自動化播種機旨在設定好操作參數後,以最少的人工干預完成基本的播種功能。整合的電子和機械執行器在整個作業過程中控制種子流量,保持精確的株距並調整播種深度。引導和對準技術確保田間行距一致。操作員輸入所需設定後,即使田間條件變化,系統也能在播種過程中自主維持這些參數。這種自動化程度降低了操作員的工作量,並透過保持均勻的效能,提高了播種一致性,使其不受作業速度或地形條件的影響。

美國智慧播種機市場佔79.7%的佔有率,預計2025年市場規模將達33億美元。美國憑藉其高度機械化的農業部門和積極採用創新技術,在智慧農業機械的發展中扮演著至關重要的角色。大規模的農業生產、不斷上漲的人事費用以及強大的資本投資能力,正促使生產者在其農業實踐中採用自動化和精準播種技術。主要農業機械製造商的存在進一步鞏固了美國的地位,使生產者能夠便捷地獲得先進的數位化農業設備。此外,農業技術創新生態系統的持續發展也為美國農業部門的智慧播種解決方案進步提供了支持。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 對精密農業的需求日益成長

- 向大規模機械化農業過渡

- 勞動力短缺和工資上漲

- 產業潛在風險與挑戰

- 高昂的初始資本成本

- 農民缺乏技術知識

- 機會

- 人工智慧驅動的決策支援的整合

- 自動和電動種植機的普及

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 自動化和控制系統

- 導航系統

- 驅動系統

- 顯示系統

- 控制系統

- GPS接收器

- 無人機/無人飛行器

- 感測和監測設備

- 智慧電錶系統

- 感應器

- 相機

- 配送系統

第6章 市場估算與預測:依自動化程度分類,2022-2035年

- 自動的

- 手動的

第7章 市場估計與預測:依作物類型分類,2022-2035年

- 田間作物

- 穀物和穀類食品

- 豆類和油籽

- 蔬菜和水果

- 林業

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 小規模農場(小於400公頃)

- 大型農場(超過400公頃)

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- AGCO

- Agrisem International

- Bourgault Industries

- CLAAS KGaA

- CNH Industrial

- Deere &Company

- Jumil

- Kinze Manufacturing

- Kubota

- Mahindra &Mahindra

- MaterMacc

- Semeato

- Trimble

- Vaderstad AB

- Yetter Farm Equipment

The Global Smart Seed Planting Machine Market was valued at USD 10.8 billion in 2025 and is estimated to grow at a CAGR of 8.8% to reach USD 24.2 billion by 2035.

Expansion in the smart seed planting machine market for smart agricultural equipment is largely supported by the growing emphasis on improving farming productivity while optimizing operational efficiency. Agricultural producers are increasingly adopting advanced equipment that enables data-based decision making, allowing them to determine ideal planting conditions by evaluating factors related to soil quality, field variability, moisture distribution, and seed characteristics. The availability of advanced digital platforms, sensing technologies, and automated systems is also improving accessibility to precision farming tools. As a result, growers are recognizing that more accurate seed placement can significantly improve germination performance and reduce input wastage, which contributes to more stable crop yields. In addition, the integration of digital agriculture solutions is transforming planting operations by enabling more consistent and predictable outcomes. As farms continue to modernize operations and rely on technology-driven agricultural management, the demand for smart seed planting machines is expected to grow steadily.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.8 Billion |

| Forecast Value | $24.2 Billion |

| CAGR | 8.8% |

Changing environmental conditions have further reduced the reliability of conventional planting approaches that rely on estimation rather than data-driven insights. Precision planting systems offer a dependable alternative by delivering consistent operational performance across varying field conditions. These machines allow farmers to monitor planting efficiency continuously, adjust machine settings automatically, and maintain detailed field records that support improved planning and long-term operational strategies. The shift toward precision agriculture represents a major transformation in modern farming practices, providing producers with improved control over planting operations and enabling more efficient management of agricultural resources.

In 2025, the automation & control systems segment accounted for USD 6.5 billion. Modern smart planting equipment relies heavily on automation and control technologies to ensure highly accurate and uniform seed distribution. These systems combine digital seed metering mechanisms, electronically controlled actuators, real-time programmable control units, and machine communication platforms to regulate seed placement, depth consistency, and row spacing. By automating key operational parameters, these technologies reduce variability caused by manual intervention and improve the uniformity of crop establishment. Another important advantage of automation and control systems is their ability to integrate with advanced monitoring technologies, allowing machines to receive real-time field feedback and adjust operations accordingly.

The automatic segment held 79% share in 2025. Automatic seed planting machines are designed to perform essential planting functions with minimal operator involvement once operational parameters have been configured. Integrated electronics and mechanical actuators control seed flow, maintain accurate spacing, and regulate planting depth throughout the operation. Guidance and alignment technologies ensure that rows remain consistent across the entire field. After the operator inputs the desired settings, the system independently maintains those parameters during the planting process, even when field conditions change. This level of automation reduces operator workload and enhances planting consistency by maintaining uniform performance regardless of operational speed or terrain conditions.

U.S. Smart Seed Planting Machine Market captured 79.7% share, generating USD 3.3 billion in 2025. The United States plays a significant role in advancing smart agricultural machinery due to its highly mechanized farming sector and strong adoption of innovative technologies. Large-scale farming operations, rising labor costs, and strong capital investment capabilities encourage producers to incorporate automation and precision planting technologies into their agricultural practices. The presence of major agricultural machinery manufacturers further strengthens the country's position by enabling easier access to advanced digital farming equipment. Additionally, the continued development of agritech innovation ecosystems is supporting the advancement of intelligent planting solutions across the U.S. agricultural landscape.

Major companies operating in the Global Smart Seed Planting Machine Market include Deere & Company, AGCO, CNH Industrial, Kubota, Mahindra & Mahindra, Trimble, CLAAS KGaA, Bourgault Industries, Kinze Manufacturing, Vaderstad AB, Agrisem International, MaterMacc, Semeato, Jumil, and Yetter Farm Equipment. Companies participating in the Smart Seed Planting Machine Market are implementing several strategic initiatives to strengthen their market position and expand their global footprint. Leading manufacturers are investing heavily in research and development to introduce advanced precision planting technologies that improve accuracy, automation, and operational efficiency. Many firms are focusing on integrating digital agriculture platforms, sensor-based technologies, and connectivity features to enhance machine intelligence and real-time data analysis capabilities. Strategic partnerships with agricultural technology providers and equipment distributors are also helping companies expand their reach across key farming regions. In addition, manufacturers are emphasizing product customization to meet diverse farming requirements and crop types.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Automation level

- 2.2.4 Crop type

- 2.2.5 Application

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for precision agriculture

- 3.2.1.2 Shift toward large-scale mechanized farming

- 3.2.1.3 Labor shortages & rising wages

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital costs

- 3.2.2.2 Limited technical knowledge among farmers

- 3.2.3 Opportunities

- 3.2.3.1 Integration of AI-driven decision support

- 3.2.3.2 Growth of autonomous & electric planters

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Automation & control systems

- 5.2.1 Guidance systems

- 5.2.2 Drive systems

- 5.2.3 Display systems

- 5.2.4 Control systems

- 5.2.5 GPS receivers

- 5.2.6 Drones/UAVS

- 5.3 Sensing & monitoring devices

- 5.3.1 Smart metering systems

- 5.3.2 Sensors

- 5.3.3 Cameras

- 5.3.4 Delivery systems

Chapter 6 Market Estimates and Forecast, By Automation Level, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automatic

- 6.3 Manual

Chapter 7 Market Estimates and Forecast, By Crop Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Row crops

- 7.3 Grains & cereals

- 7.4 Pulses & oilseeds

- 7.5 Vegetables & fruits

- 7.6 Forestry

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Small farms (Below 400 hectares)

- 8.3 Large farms (Above 400 hectares)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AGCO

- 11.2 Agrisem International

- 11.3 Bourgault Industries

- 11.4 CLAAS KGaA

- 11.5 CNH Industrial

- 11.6 Deere & Company

- 11.7 Jumil

- 11.8 Kinze Manufacturing

- 11.9 Kubota

- 11.10 Mahindra & Mahindra

- 11.11 MaterMacc

- 11.12 Semeato

- 11.13 Trimble

- 11.14 Vaderstad AB

- 11.15 Yetter Farm Equipment

播種機市場:2026-2032年全球市場預測(依產品類型、播種方式、運作模式、農場規模、行距、動力來源、行數、安裝方式、應用領域及銷售管道)

播種機市場:2026-2032年全球市場預測(依產品類型、播種方式、運作模式、農場規模、行距、動力來源、行數、安裝方式、應用領域及銷售管道) 全球播種和種植設備市場

全球播種和種植設備市場 種植設備市場:按類型、作物類型、設計和地區分類-預測至2031年化肥機械市場:2026-2032年全球市場預測(依產品類型、動力來源、部署方式、技術、作物類型、最終用戶和銷售管道)種植工具市場:依產品類型、動力來源、材料、應用、通路和最終用戶分類-全球預測,2026-2032年自走式蔬菜移植市場:按類型、引擎功率、種植行數、價格範圍、通路、最終用戶和應用分類-2026-2032年全球預測蔬菜移植市場:按類型、操作方式、動力來源、應用和最終用戶分類,全球預測,2026-2032年農業植物保護無人機市場:按無人機類型、組件、作物類型、應用、最終用戶分類,全球預測(2026-2032)

種植設備市場:按類型、作物類型、設計和地區分類-預測至2031年化肥機械市場:2026-2032年全球市場預測(依產品類型、動力來源、部署方式、技術、作物類型、最終用戶和銷售管道)種植工具市場:依產品類型、動力來源、材料、應用、通路和最終用戶分類-全球預測,2026-2032年自走式蔬菜移植市場:按類型、引擎功率、種植行數、價格範圍、通路、最終用戶和應用分類-2026-2032年全球預測蔬菜移植市場:按類型、操作方式、動力來源、應用和最終用戶分類,全球預測,2026-2032年農業植物保護無人機市場:按無人機類型、組件、作物類型、應用、最終用戶分類,全球預測(2026-2032) 2026年全球播種機市場報告2026年全球施肥機械市場報告

2026年全球播種機市場報告2026年全球施肥機械市場報告