|

市場調查報告書

商品編碼

1998664

心臟監護設備市場:商機、成長要素、產業趨勢分析及2026-2035年預測Cardiac Monitoring Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

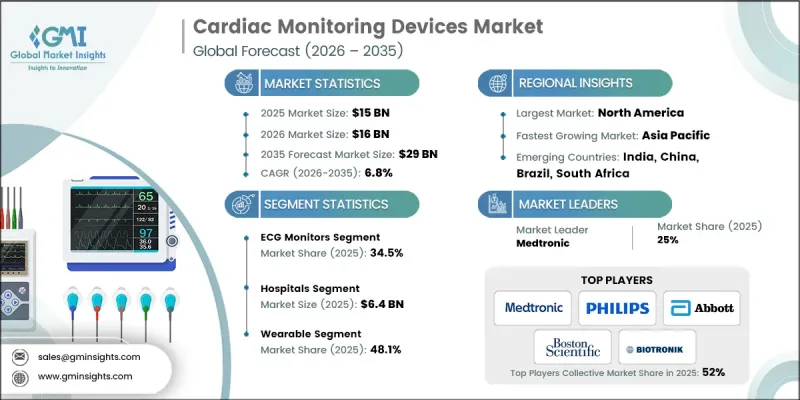

全球心臟監護設備市場預計到 2025 年將價值 150 億美元,預計到 2035 年將以 6.8% 的複合年成長率成長至 290 億美元。

隨著持續心血管監測和早期疾病檢測在醫療保健系統中變得日益重要,該市場正持續加速成長。成長要素之一是全球老年人口的快速成長,而老年人罹患心血管疾病的風險很高。與老齡化相關的心臟變化會顯著增加心律不整、心臟衰竭和其他心臟併發症的風險,因此對可靠的長期監測技術的需求日益成長。同時,數位健康技術的不斷進步正在提升監測系統的功能性和易用性,使醫療專業人員不僅能夠在傳統醫療環境中監測心臟功能,還可以進行遠端監測。這些改進有助於更早進行臨床介入、改善病患管理並提升醫療效果。飛利浦、Medtronic、雅培、波士頓科學公司和百多力等行業領導者不斷拓展產品功能,並大力投資先進的監測技術,從而鞏固其在全球心臟監測設備市場的領先地位,並推動該行業的穩步成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 150億美元 |

| 預測金額 | 290億美元 |

| 複合年成長率 | 6.8% |

由於預期壽命延長和出生率下降,全球65歲及以上人口數量持續成長。這一人口趨勢對心臟監測設備市場產生了重大影響,因為老年人罹患心血管併發症的風險更高,尤其是心律不整和心臟功能下降。生物老齡化會導致心臟結構和電生理變化,包括組織硬化、電傳導減慢和自主神經系統調節改變。這些生理變化會增加心臟異常活動和循環系統併發症的風險,凸顯了可靠的心臟監測技術的重要性日益凸顯。

到2025年,心電圖(ECG)監視器市佔率將達到34.5%。心電圖監護系統仍然是評估心臟電訊號和識別心律不整的重要工具。這些系統可幫助醫師評估心律不整、電傳導異常以及其他心臟功能變化。最新的心電圖監護技術透過改良的降噪和數位濾波功能,實現了高度精確的訊號擷取。這提高了診斷準確性,有助於及時做出臨床決策,同時確保患者在所有醫療環境中的安全。

預計到2025年,穿戴式心電圖監測設備市場將佔據48.1%的市場佔有率,到2035年市場規模將達到142億美元。穿戴式監測技術包括小巧便捷的設備,旨在持續監測日常活動中的心率。推動這些設備普及的主要因素包括:佩戴舒適度的提升、監測時間的延長以及能夠檢測到短期臨床評估可能遺漏的間歇性心率異常。隨著醫療保健不斷向遠距患者管理轉型,穿戴式監測解決方案對患者和醫療服務提供者都變得越來越重要。這些設備輕巧、無線,專為長期佩戴而設計,使用戶能夠在日常生活中不間斷地收集心率數據。

預計到2025年,北美心電圖(ECG)監測設備市場規模將達56億美元。該地區受益於完善的醫療保健生態系統、先進醫療技術的高普及率以及健全的法規結構,這些框架都確保了心電圖監測設備的安全性和性能標準。此外,該地區面臨沉重的心血管疾病負擔,這持續推動對先進監測技術的強勁需求。醫療機構越來越依賴連續心電圖監測解決方案來幫助早期發現心律不整和其他心血管併發症,從而改善疾病管理並提升患者預後。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策和資料完整性計劃

- 資訊來源一致性通訊協定

- GMI人工智慧政策和資料完整性計劃

- 調查過程和可靠性評分

- 調查過程的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 人口老化和心血管疾病風險增加

- 生活方式的改變和心臟病盛行率的上升

- 遠端監控和穿戴式科技的進步

- 數位醫療和人工智慧領域的進展

- 產業潛在風險與挑戰

- 資料隱私和安全問題

- 先進監控解決方案高成本

- 市場機遇

- 家庭和門診心臟監測的需求日益成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術趨勢(基於初步調查)

- 目前技術

- 新興技術

- 未來市場趨勢(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

- 價格分析(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依設備類型分類,2022-2035年

- 心電圖監測儀

- 心電圖監測

- 事件記錄器/外部循環記錄器

- 攜帶式心電遙測裝置

- 植入式心臟監測器

- 其他設備類型

第6章 市場估計與預測:依類型分類,2022-2035年

- 穿戴式裝置

- 不穿戴式

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 心律不整檢測

- 心房顫動

- 心搏過速

- 心搏過緩

- 房性/室性早期心搏(PACs/PVCs)

- 心肌缺血和心肌梗塞的檢測

- 心率和心率監測

- 監測暈厥和心悸

- 術前及術後監測

- 其他用途

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 醫院

- 診斷中心

- 門診手術中心

- 居家醫療設施

- 其他最終用戶

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Abbott Laboratories

- ACS Diagnostics

- AliveCor

- BIOTRONIK

- Boston Scientific Corporation

- BPL Medical

- GE Healthcare

- iRhythm

- Medtronic

- MicroPort

- Neurosoft

- Nihon Kohden

- Philips

- Schiller AG

The Global Cardiac Monitoring Devices Market was valued at USD 15 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 29 billion by 2035.

Growth across this market continues to accelerate as healthcare systems increasingly prioritize continuous cardiovascular surveillance and early disease detection. A key growth catalyst is the rapidly rising elderly population worldwide, which carries a greater probability of developing cardiovascular disorders. Age-related cardiac changes significantly increase the likelihood of rhythm disturbances, heart failure, and other cardiac complications, thereby increasing the need for reliable long-term monitoring technologies. At the same time, ongoing advancements in digital health technologies are enhancing the functionality and accessibility of monitoring systems, allowing healthcare providers to remotely observe cardiac performance, as well as in traditional care environments. These improvements support earlier clinical intervention, better patient management, and improved healthcare outcomes. Leading industry participants, such as Philips, Medtronic, Abbott Laboratories, Boston Scientific Corporation, and BIOTRONIK, continue to expand their product capabilities while investing heavily in advanced monitoring technologies, reinforcing their leadership in the global cardiac monitoring devices market and contributing to the steady growth of this industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15 Billion |

| Forecast Value | $29 Billion |

| CAGR | 6.8% |

The number of individuals aged 65 years and above continues to increase globally due to longer life expectancy and declining fertility rates. This demographic trend is playing an important role in shaping the cardiac monitoring devices market because older adults face a higher probability of developing cardiovascular complications, particularly rhythm-related disorders and reduced cardiac efficiency. Biological aging contributes to structural and electrical changes within the heart, including tissue stiffening, slower electrical conduction, and alterations in autonomic control. These physiological changes elevate the risk of abnormal cardiac activity and circulatory complications, which increases the importance of reliable cardiac monitoring technologies.

In 2025, the ECG monitors segment held 34.5% share. ECG monitoring systems remain a critical tool for assessing cardiac electrical signals and identifying irregular heart activity. These systems support physicians in evaluating rhythm disturbances, electrical conduction abnormalities, and other changes in cardiac function. Modern ECG monitoring technologies now deliver highly accurate signal acquisition supported by improved noise reduction and digital filtering capabilities, which strengthen diagnostic accuracy and enable timely clinical decisions while maintaining patient safety across healthcare environments.

The wearable cardiac monitoring devices segment captured 48.1% share in 2025 and is expected to reach USD 14.2 billion by 2035. Wearable monitoring technologies consist of compact and convenient devices designed to continuously track cardiac rhythm during normal daily activities. Their growing adoption is largely attributed to improved comfort, extended monitoring duration, and the ability to detect intermittent cardiac irregularities that might remain unnoticed during short clinical evaluations. As healthcare continues to shift toward remote patient management, wearable monitoring solutions are becoming increasingly valuable for both patients and healthcare providers. These devices are lightweight, wireless, and designed for long-term use, enabling uninterrupted cardiac data collection while individuals maintain their normal routines.

North America Cardiac Monitoring Devices Market reached USD 5.6 billion in 2025. The region benefits from a sophisticated healthcare ecosystem, high adoption of advanced medical technologies, and a well-structured regulatory framework that ensures safety and performance standards for cardiac monitoring equipment. In addition, the region faces a substantial burden of cardiovascular conditions, which continues to generate strong demand for advanced monitoring technologies. Healthcare providers increasingly rely on continuous cardiac monitoring solutions to support early identification of rhythm abnormalities and other cardiovascular complications, enabling improved disease management and better patient outcomes.

Prominent organizations operating in the Global Cardiac Monitoring Devices Market include Abbott Laboratories, Medtronic, Philips, Boston Scientific Corporation, BIOTRONIK, GE Healthcare, Nihon Kohden, Schiller AG, MicroPort, AliveCor, BPL Medical, iRhythm, Neurosoft, and ACS Diagnostics. Companies competing in the Cardiac Monitoring Devices Market are focusing on multiple strategic initiatives to strengthen their market position and expand global reach. Major players are prioritizing continuous investment in research and development to introduce technologically advanced monitoring solutions with improved accuracy, connectivity, and patient comfort. Strategic collaborations with healthcare institutions and digital health companies are also becoming common as firms aim to integrate remote monitoring capabilities and data analytics into their product ecosystems. Many organizations are expanding their geographic footprint through distribution partnerships and regional market entry strategies.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI ai policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI ai policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Device type trends

- 2.2.2 Type trends

- 2.2.3 Application

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising aging population and increased risk of cardiovascular diseases

- 3.2.1.2 Lifestyle changes and increasing prevalence of heart diseases

- 3.2.1.3 Advancements in remote monitoring and wearable technology

- 3.2.1.4 Advancements in digital health and AI

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and security concerns

- 3.2.2.2 High cost of advanced monitoring solutions

- 3.2.3 Market opportunity

- 3.2.3.1 Growing preference for home-based and ambulatory cardiac monitoring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Impact of AI and generative AI on the market

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Pricing analysis (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Device Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 ECG monitors

- 5.3 Holter monitors

- 5.4 Event recorders/external loop recorders

- 5.5 Mobile cardiac telemetry devices

- 5.6 Implantable cardiac monitors

- 5.7 Other device types

Chapter 6 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Wearable

- 6.3 Non wearable

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Arrhythmia detection

- 7.2.1 Atrial fibrillation

- 7.2.2 Tachycardia

- 7.2.3 Bradycardia

- 7.2.4 Premature atrial and ventricular contractions (PACs/PVCs)

- 7.3 Cardiac ischemia and myocardial infarction detection

- 7.4 Heart rate and rhythm monitoring

- 7.5 Syncope and palpitation monitoring

- 7.6 Pre/post-operative monitoring

- 7.7 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic centers

- 8.4 Ambulatory surgery centers

- 8.5 Homecare settings

- 8.6 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 ACS Diagnostics

- 10.3 AliveCor

- 10.4 BIOTRONIK

- 10.5 Boston Scientific Corporation

- 10.6 BPL Medical

- 10.7 GE Healthcare

- 10.8 iRhythm

- 10.9 Medtronic

- 10.10 MicroPort

- 10.11 Neurosoft

- 10.12 Nihon Kohden

- 10.13 Philips

- 10.14 Schiller AG

穿戴式心電圖監測解決方案市場預測至2034年—按設備類型、監測方法、技術、應用、最終用戶和地區分類的全球分析

穿戴式心電圖監測解決方案市場預測至2034年—按設備類型、監測方法、技術、應用、最終用戶和地區分類的全球分析 攜帶式心臟監測設備市場規模、佔有率和成長分析:按設備類型、技術、應用、最終用戶和地區分類-2026-2033年產業預測穿戴式心電圖監測設備市場預測至2034年:按設備類型、監測方法、技術、應用、最終用戶和地區分類的全球分析

攜帶式心臟監測設備市場規模、佔有率和成長分析:按設備類型、技術、應用、最終用戶和地區分類-2026-2033年產業預測穿戴式心電圖監測設備市場預測至2034年:按設備類型、監測方法、技術、應用、最終用戶和地區分類的全球分析 植入式心臟監測器市場:依產品類型、適應症、技術、最終用戶和通路分類-2026-2032年全球市場預測遠端心臟監測設備市場:按設備類型、連接方式、適應症、最終用戶和分銷管道分類-全球市場預測(2026-2032 年)

植入式心臟監測器市場:依產品類型、適應症、技術、最終用戶和通路分類-2026-2032年全球市場預測遠端心臟監測設備市場:按設備類型、連接方式、適應症、最終用戶和分銷管道分類-全球市場預測(2026-2032 年) 心臟心臟事件記錄器市場:按產品類型、應用、患者群、技術、最終用戶和地區分類攜帶式心電監視器市場:按類型、便攜性、監護類型、應用、最終用戶和分銷管道分類-全球預測,2026-2032年

心臟心臟事件記錄器市場:按產品類型、應用、患者群、技術、最終用戶和地區分類攜帶式心電監視器市場:按類型、便攜性、監護類型、應用、最終用戶和分銷管道分類-全球預測,2026-2032年 2026年全球智慧型可攜式心電圖(ECG)設備市場報告2026年全球遠距心臟監測市場報告2026年攜帶式心電圖(ECG)設備訂閱市場報告

2026年全球智慧型可攜式心電圖(ECG)設備市場報告2026年全球遠距心臟監測市場報告2026年攜帶式心電圖(ECG)設備訂閱市場報告