|

市場調查報告書

商品編碼

1998660

2026 年至 2035 年住宅滾動式快門市場的商業機會、成長要素、產業趨勢與預測。Residential Window Rolling Shutters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

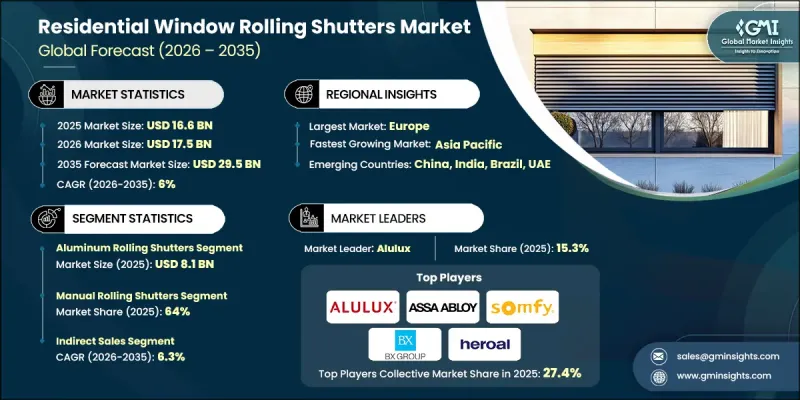

預計到 2025 年,全球住宅滾動式快門市場價值將達到 166 億美元,並有望以 6% 的複合年成長率成長,到 2035 年達到 295 億美元。

人們對住宅安全和個人隱私的日益關注,顯著提升了現代住宅開發項目中對滾動式快門系統的需求。快速的城市擴張和住宅計劃的持續成長也為市場成長創造了有利條件。住宅越來越追求兼顧安全性和美觀性的建築元素,這推動了先進捲百葉窗解決方案的普及。此外,節能意識的提升也是推動捲簾系統普及的重要因素,因為滾動式快門可以增強隔熱性能,並有助於調節室內溫度。消費者越來越注重降低暖氣和冷氣系統的能耗,這進一步促進了市場成長。百葉窗系統的技術進步也正在改變整個產業格局。整合自動化和智慧控制功能的產品越來越受到追求智慧家庭環境的住宅的青睞。此外,製造商還提供更廣泛的客製化選項,包括各種設計風格和顏色選擇,使消費者能夠選擇既符合住宅不同美學風格又兼顧實用功能的百葉窗。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 166億美元 |

| 預測金額 | 295億美元 |

| 複合年成長率 | 6% |

預計到2025年,鋁合金滾動式快門市場規模將達到81億美元,並在2035年之前以6.2%的複合年成長率成長。鋁合金百葉窗需求成長的主要促進因素是其輕質結構、使用壽命長以及優異的耐環境磨損性能。這些特性使鋁合金成為現代住宅尋求可靠、低維護窗戶防護解決方案的首選材料。除了強度和耐用性之外,鋁合金百葉窗還具有有效的隔熱和安全功能,進一步促進了其在住宅中的應用。同時,由於其成本效益高且維護需求低,PVC滾動式快門,因為除了其隔熱性能之外,它還提供多種款式選擇,以滿足不同的設計和美學偏好。

預計2026年至2035年,電動滾動式快門市場將以6.8%的複合年成長率成長。消費者對智慧住宅解決方案日益成長的興趣是推動電動百葉窗系統需求成長的主要動力。住宅越來越重視電動系統透過其自動化功能帶來的便利性和易用性。自動化技術與住宅環境的日益融合,正在促進這些產品的普及,尤其是在人口密集的都市區住宅。隨著智慧家庭的不斷普及,電動滾動式快門正成為那些既追求更強大的功能又渴望現代生活便利的消費者的更具吸引力的選擇。

美國住宅滾動式快門市場佔據76%的市場佔有率,預計2025年市場規模將達30億美元。美國市場擴張的主要驅動力是消費者對節能住宅維修方案日益成長的興趣以及對住宅安全的重視。人們對滾動式快門功能優勢的認知不斷提高,推動了住宅的採用。這些系統有助於改善室內隔熱、降低外部噪音,並增強對各種環境因素的防護。智慧家庭技術的日益普及也促進了具備遠端和數位控制功能的自動捲簾百葉窗系統的普及。此外,美國不斷變化的環境條件和氣候模式進一步增強了對可靠窗戶防護解決方案的需求,從而支撐了美國住宅滾動式快門市場的持續成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 監理情勢

- 北美(建築規範、颶風規範)

- 歐洲(CE標誌、能源效率標準)

- 亞太地區(當地認證要求)

- 認證標準(ISO、ASTM、EN 標準)

- 與能源效率相關的法規和獎勵

- 價格分析(基於初步調查)

- 過去價格趨勢分析(2022-2025)

- 根據玩家類型(高階/超值/經濟型)制定的定價策略(基於初步研究)

- 區域價格波動分析

- 安裝成本基準分析

- 主要貿易路線和關稅影響分析(基於初步調查)

- HS編碼分類與貿易統計(7308.30,7610.90)

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧正在改變傳統的經營模式。

- GenAI按客戶群分類的應用案例和實施藍圖

- 風險、局限性和監管考量

- 人工智慧驅動的智慧家庭生態系統的整合

- 生產能力和生產環境(擠出成型、輥壓成型、組裝自動化)基準測試(基於初步調查)

- 按地區和主要製造商分類的製造能力(基於初步調查)

- 運轉率和擴張計劃(基於初步調查)

- 生產技術

- 波特五力分析

- PESTEL 分析

- 消費者購買行為

- 購買模式

- 偏好分析

- 消費行為的區域差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依材料分類,2022-2035年

- 鋁合金滾動式快門

- PVC滾動式快門

- 鋼製滾動式快門

- 其他(木製滾動式快門等)

第6章 市場估計與預測:依營運方式分類,2022-2035年

- 手動百葉窗

- 電動百葉窗

- 電動遙控型

- 牆壁開關

- 智慧/物聯網相容型百葉窗

第7章 市場估計與預測:計劃類型,2022-2035年

- 新建工程

- 維修和維修工程

第8章 市場估算與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Alulux

- Aluroll

- American Industrial Door

- ASSA ABLOY

- Bunka Shutter

- 黑刺李,北美洲

- Heroal

- Hormann Group

- Novoferm

- Pentagon

- Roll Shutter Systems

- Rollac

- ROMA

- Sanwa Holdings

- Somfy Group

The Global Residential Window Rolling Shutters Market was valued at USD 16.6 billion in 2025 and is estimated to grow at a CAGR of 6% to reach USD 29.5 billion by 2035.

The rising focus on residential safety and personal privacy is significantly increasing demand for rolling shutter systems across modern housing developments. Rapid urban expansion and the continued rise in residential construction projects are also creating favorable conditions for the market's expansion. Homeowners are increasingly incorporating architectural elements that enhance both security and visual appeal, which is strengthening the adoption of advanced window shutter solutions. Growing awareness of energy efficiency is another key factor encouraging adoption, as rolling shutters contribute to better insulation and help regulate indoor temperatures. Consumers are becoming more conscious of reducing energy consumption associated with cooling and heating systems, further supporting market growth. Technological developments in shutter systems are also transforming the industry landscape. Integration of automated and intelligent control features is gaining popularity among homeowners who prefer connected home environments. In addition, manufacturers are offering wider customization possibilities that include various design styles and color options, allowing consumers to match shutters with diverse residential aesthetics while maintaining functional performance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.6 Billion |

| Forecast Value | $29.5 Billion |

| CAGR | 6% |

The aluminum rolling shutters segment generated USD 8.1 billion in 2025 and is expected to grow at a CAGR of 6.2% throughout 2035. The increasing preference for aluminum shutters is largely attributed to the material's lightweight structure, long-lasting durability, and strong resistance to environmental wear. These characteristics make aluminum a preferred material choice for modern residential properties seeking reliable and low-maintenance window protection solutions. In addition to strength and longevity, aluminum shutters provide effective insulation and improved security features, further supporting their adoption across newly developed housing units. At the same time, PVC rolling shutters are expected to record steady market growth due to their cost-effective nature and minimal maintenance requirements. Consumers are increasingly selecting PVC options because they provide insulation benefits while offering diverse styling possibilities that accommodate different design preferences and aesthetic choices.

The motorized rolling shutters segment is expected to register a CAGR of 6.8% from 2026 to 2035. Rising consumer interest in automated home solutions is a major factor accelerating the demand for motorized shutter systems. Homeowners increasingly value convenience and ease of operation, which motorized systems provide through automated functionality. The growing integration of automation technologies into residential environments is encouraging wider adoption of these products, particularly within densely populated urban housing developments. As smart home adoption continues to expand, motorized rolling shutters are becoming an increasingly attractive option for consumers seeking both enhanced functionality and modern living convenience.

United States Residential Window Rolling Shutters Market accounted for 76% share, generating USD 3 billion in 2025. Market expansion in the United States is primarily driven by increasing consumer interest in energy-efficient home improvement solutions combined with a strong focus on residential security. Greater awareness of the functional advantages of window rolling shutters is encouraging adoption among homeowners. These systems contribute to improved indoor insulation, reduced external noise levels, and enhanced protection against varying environmental conditions. The growing popularity of smart home technologies is also supporting the adoption of automated window shutter systems equipped with remote and digital control capabilities. In addition, shifting environmental conditions and changing climate patterns across the country are further strengthening demand for reliable window protection solutions, supporting the continued growth of the residential window rolling shutters market in the United States.

Key companies operating in the Global Residential Window Rolling Shutters Market include Alulux, Aluroll, American Industrial Door, Assa Abloy, Bunka Shutter, Croci North America, Heroal, Hormann Group, Novoferm, Pentagon, Roll Shutter Systems, Rollac, ROMA, Sanwa Holdings, and Somfy Group. Companies participating in the Global Residential Window Rolling Shutters Market are implementing several strategic initiatives to strengthen their market position and expand global presence. Manufacturers are investing heavily in research and development to introduce advanced shutter technologies that offer improved durability, enhanced insulation performance, and integrated automation features. Product innovation focused on smart control systems and energy-efficient materials is helping companies differentiate their offerings in a competitive market environment. Many firms are also expanding their distribution networks and strengthening partnerships with construction companies, home improvement retailers, and residential developers to improve product availability.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Operation Type

- 2.2.4 Project Type

- 2.2.5 Distribution Channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.7 Regulatory landscape

- 3.7.1 North America (Building Codes, Hurricane Standards)

- 3.7.2 Europe (CE Marking, Energy Performance Standards)

- 3.7.3 Asia Pacific (Local Certification Requirements)

- 3.7.4 Certification Standards (ISO, ASTM, EN Standards)

- 3.7.5 Energy Efficiency Regulations & Incentives

- 3.8 Pricing analysis (driven by primary research)

- 3.8.1 Historical price trend analysis (2022-2025)

- 3.8.2 Pricing strategy by player type (premium/value/economy) (driven by primary research)

- 3.8.3 Regional price variation analysis

- 3.8.4 Installation cost benchmarking

- 3.9 Key trade corridors & tariff impact analysis (driven by primary research)

- 3.9.1 HS Code Classification & Trade Statistics (7308.30, 7610.90)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-Driven Disruption of Traditional Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Customer Segment

- 3.10.3 Risks, Limitations & Regulatory Considerations

- 3.10.4 AI-Enabled Smart Home Ecosystem Integration

- 3.11 Benchmarking (extrusion, roll-forming, assembly automation) capacity & production landscape (driven by primary research)

- 3.11.1 Manufacturing capacity installed by region & key producer (driven by primary research)

- 3.11.2 Capacity utilization rates & expansion pipelines (driven by primary research)

- 3.11.3 Production technology

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Consumer buying behavior

- 3.14.1 Purchasing patterns

- 3.14.2 Preference analysis

- 3.14.3 Regional variations in consumer behavior

- 3.14.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Material Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Aluminum rolling shutters

- 5.3 PVC rolling shutters

- 5.4 Steel rolling shutters

- 5.5 Others (wood rolling shutters etc.)

Chapter 6 Market Estimates & Forecast, By Operation Type, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Manual rolling shutters

- 6.3 Motorized rolling shutters

- 6.3.1 Motorized remote

- 6.3.2 Motorized wall switch

- 6.4 Smart/IoT-enabled rolling shutters

Chapter 7 Market Estimates & Forecast, By Project Type, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 New construction

- 7.3 Renovation/retrofit

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alulux

- 10.2 Aluroll

- 10.3 American Industrial Door

- 10.4 ASSA ABLOY

- 10.5 Bunka Shutter

- 10.6 Croci North America

- 10.7 Heroal

- 10.8 Hormann Group

- 10.9 Novoferm

- 10.10 Pentagon

- 10.11 Roll Shutter Systems

- 10.12 Rollac

- 10.13 ROMA

- 10.14 Sanwa Holdings

- 10.15 Somfy Group

車庫門市場:2026-2032年全球市場預測(依產品類型、材質、操作機制、最終用途、應用及通路分類)電動商用車庫門市場:依運作模式、門體材料、安裝類型、公司規模、通路、最終用戶產業分類,全球預測(2026-2032年)

車庫門市場:2026-2032年全球市場預測(依產品類型、材質、操作機制、最終用途、應用及通路分類)電動商用車庫門市場:依運作模式、門體材料、安裝類型、公司規模、通路、最終用戶產業分類,全球預測(2026-2032年) 智慧車庫門控制器市場規模、佔有率和成長分析(按控制器類型、控制機制、功能特性、安裝方式、公司規模、應用領域和地區分類)—產業預測(2026-2033年)

智慧車庫門控制器市場規模、佔有率和成長分析(按控制器類型、控制機制、功能特性、安裝方式、公司規模、應用領域和地區分類)—產業預測(2026-2033年) 全球戶外百葉窗市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球捲簾百葉窗馬達市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球戶外百葉窗市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球捲簾百葉窗馬達市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球百葉窗市場報告2026年全球自動車庫大門市場報告

2026年全球百葉窗市場報告2026年全球自動車庫大門市場報告 全球戶外百葉窗市場全球捲簾百葉窗馬達市場

全球戶外百葉窗市場全球捲簾百葉窗馬達市場 百葉窗市場-全球產業規模、佔有率、趨勢、機會和預測(按產品類型、機制、應用、地區和競爭細分,2020-2030 年)

百葉窗市場-全球產業規模、佔有率、趨勢、機會和預測(按產品類型、機制、應用、地區和競爭細分,2020-2030 年)