|

市場調查報告書

商品編碼

1982386

自行車車架市場商機、成長要素、產業趨勢分析及2026-2035年預測。Bicycle Frames Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

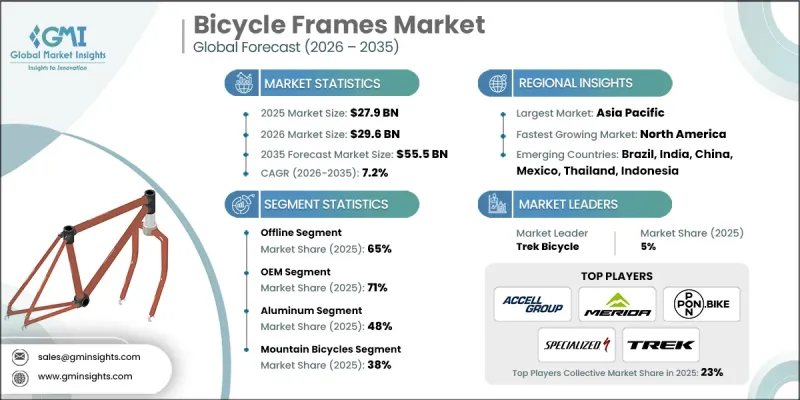

預計到 2025 年,全球自行車車架市場價值將達到 279 億美元,並預計以 7.2% 的複合年成長率成長,到 2035 年達到 555 億美元。

自行車車架在任何自行車的整體性能、安全性、耐用性和騎乘體驗中都扮演著至關重要的角色,無論是公路車、山地自行車、混合動力車或電動自行車。由於車架直接影響騎乘舒適度、重量、空氣動力學性能和載重能力,製造商正致力於輕量化材料和創新設計。該市場涵蓋使用鋁、碳纖維、鋼、鈦和先進複合材料製造車架,包括設計、管材成型、焊接、表面處理以及向OEM和售後市場管道供貨。液壓成型鋁和高模量碳纖維車架的技術進步顯著提高了剛性重量比,並增強了性能。人們對健康、城市交通和自行車基礎設施日益成長的關注正在推動對先進車架的需求。政府推廣永續交通途徑的措施和電動自行車的普及進一步促進了對增強型電池相容車架設計的需求,推動市場朝向高性能、環保的出行解決方案發展。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 279億美元 |

| 預測金額 | 555億美元 |

| 複合年成長率 | 7.2% |

預計到2025年,線下通路將佔據65%的市場佔有率,並在2035年之前以6.9%的複合年成長率成長。由於自行車購買涉及實體檢驗,因此能夠提供試騎、專業適配服務和社區互動的離線管道仍然至關重要。專業零售商透過提供專家諮詢、交貨前組裝和持續維護支援來建立客戶忠誠度並保證其零售利潤。

預計到2025年,OEM(整車製造商)市佔率將達到71%,並在2035年之前以7.5%的複合年成長率成長。 OEM夥伴關係的重點在於產量保障、聯合技術開發、供應鏈整合以及智慧財產權(IP)合作。車架製造商透過材料創新、懸吊設計、製造流程最佳化和產品測試等方式為自行車品牌提供支援。電動自行車的成長進一步鞏固了OEM管道,因為電池、馬達和電子元件的整合需要車架供應商和品牌之間密切的技術合作。

預計2026年至2035年,中國自行車車架市場將以5.6%的複合年成長率成長。國家政策強調輕量化車架技術和與電動自行車相容的設計,以支持城市交通現代化、環保交通基礎設施建設以及提升國內製造業競爭力。鼓勵在地採購獎勵和遵守出口法規的激勵措施正在增強國內車架製造商在國內外市場的競爭力。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 健康意識的提高和騎乘運動的普及。

- 城市交通轉型與交通擁擠解決方案

- 政府為促進自行車基礎建設所做的努力

- 電動自行車市場的快速成長正在推動對專用車架的需求。

- 高性能自行車對輕質材料的需求

- 產業潛在風險與挑戰

- 先進材料(碳纖維、鈦)高成本

- 供應鏈中斷和原料短缺

- 後疫情時代市場飽和與庫存過剩

- 來自低成本亞洲製造商的競爭

- 市場機遇

- 電動自行車市場的發展需要更堅固的車架。

- 對客製化的需求使得高價位產品成為可能。

- 永續和可回收材料的創新

- 在新興市場(印度、東南亞、拉丁美洲)拓展業務

- 直接面對消費者(D2C)經營模式的成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國消費品安全委員會 (CPSC) 自行車車架標準

- 加拿大 - 《加拿大消費品安全法》(CCPSA)下的自行車法規

- 歐洲

- 德國DIN標準與EN 15194電動自行車車架認證

- 英國—脫歐後自行車車架的安全和UKCA標誌要求

- 法國 - NF 標準和國家主動出行認證框架

- 義大利-UNI標準與智慧交通系統自行車基礎設施的整合

- 亞太地區

- 中國和英國關於電動自行車車架的標準以及工信部技術法規

- 印度 - BIS 認證和 AIS 自行車車架安全標準

- 日本JIS標準與國土交通省自行車安全框架

- 澳洲 - 澳洲消費者法和AS/NZS自行車車架標準

- 拉丁美洲

- 墨西哥 - NOM 自行車安全標準和積極移動框架

- 阿根廷 - 交通法第 24.449 號

- 中東和非洲(MEA)

- 南非 - 道路交通法(1996 年)

- 沙烏地阿拉伯—SASO標準和2030願景計劃促進積極出行

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 感測器技術的發展(攝影機、LiDAR、雷達、超音波)

- 整合感測器融合

- 人工智慧和機器學習在行人偵測的應用

- 新興技術

- V2X 通訊可提高偵測能力

- 適用於夜間和低光源環境的偵測技術

- 當前技術趨勢

- 專利分析

- 主要專利趨勢

- 技術創新熱點

- 主要企業提交的專利申請

- 新的智慧財產權戰略

- 價格分析

- 對過去價格趨勢的分析

- 鋁合金車架價格走勢(2022-2025)

- 鋼骨價格趨勢(2022-2025)

- 碳纖維車架價格趨勢(2022-2025)

- 鈦合金車架價格趨勢(2022-2025)

- 按玩家類型分類的定價策略

- 高階定位策略(鈦合金、高模量碳纖維)

- 價值細分市場策略(鋁、標準碳鋼)

- 成本定價模式(OEM製造)

- 使用案例和成功案例

- 案例研究

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 設計自動化與生成式工程

- 品管和缺陷檢測系統

- 需求預測和庫存最佳化

- 風險、限制和監管考量

- 客戶設計資料中的資料隱私

- 人工智慧模型在結構工程中的可靠性

- 對勞動力替代的擔憂

- 未來前景與機遇

- 新興市場板塊

- 未來預期的技術變革

- 永續發展趨勢

- 經營模式創新

- 長期成長預測(2030-2040 年)

- 相關人員的策略建議

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依材料分類,2022-2035年

- 鋁

- 鋼

- 碳纖維

- 鈦

- 其他

第6章 市場估計與預測:依框架分類,2022-2035年

- 山地自行車

- 油電混合自行車

- 電動自行車

- 公路自行車

- 其他

第7章 市場估價與預測:依銷售管道分類,2022-2035年

- 線上

- 離線

第8章 市場估算與預測:依通路分類,2022-2035年

- OEM

- 售後市場

第9章 市場估計與預測:依最終用途分類,2022-2035年

- 專業賽車自行車

- 休閒和愛好者的自行車

- 通勤者/都市區騎行者

- 年輕的自行車手

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 瑞典

- 丹麥

- 波蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 以色列

第11章:公司簡介

- 世界公司

- Argon 18

- Bianchi

- Cannondale Bikes

- Canyon

- Cervelo

- Cicli Pinarello SRL

- Giant Manufacturing

- GT Bicycles

- Kona Bikes

- Merida

- Santa Cruz

- SCOTT Sports

- Specialized Bicycle

- Trek

- 本地球員

- Chicago Bicycle Company

- Ideal Bike

- Dengfu Sports Equipment

- 新興企業和技術基礎設施公司

- Pinion

- YT Industries

- Aventon Bikes

The Global Bicycle Frames Market was valued at USD 27.9 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 55.5 billion by 2035.

Bicycle frames play a crucial role in overall bicycle performance, safety, durability, and rider experience across road, mountain, hybrid, and electric models. They directly affect ride quality, weight, aerodynamics, and load capacity, prompting manufacturers to focus on lightweight materials and innovative designs. The market includes frame production using aluminum, carbon fiber, steel, titanium, and advanced composite materials, encompassing design, tube forming, welding, surface finishing, and supply to OEM and aftermarket channels. Advances in hydroformed aluminum and high-modulus carbon fiber frames have significantly improved stiffness-to-weight ratios, enhancing performance. Rising interest in health, urban mobility, and cycling infrastructure is driving demand for advanced frames. Government initiatives promoting sustainable transportation and the growth of e-bikes further support demand for reinforced, battery-compatible frame designs, positioning the market toward high-performance, eco-friendly mobility solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $27.9 Billion |

| Forecast Value | $55.5 Billion |

| CAGR | 7.2% |

The offline segment held a 65% share in 2025 and is expected to grow at a CAGR of 6.9% through 2035. Offline channels remain critical due to the hands-on nature of bicycle purchases, enabling test rides, professional fitting services, and community engagement. Specialty retailers provide expert consultations, pre-delivery assembly, and ongoing mechanical support, creating customer loyalty and justifying retail margins.

The OEM segment accounted for 71% share in 2025 and is estimated to grow at a CAGR of 7.5% through 2035. OEM partnerships focus on volume commitments, technical co-development, supply chain integration, and IP collaboration. Frame manufacturers support bicycle brands through material innovation, suspension design, manufacturing optimization, and product testing. Growth in e-bikes further strengthens the OEM channel, as integrating batteries, motors, and electronics requires close technical collaboration between frame suppliers and brands.

China Bicycle Frames Market is projected to grow at a CAGR of 5.6% from 2026 to 2035. National policies emphasize lightweight frame technologies and e-bike-compatible designs to support urban mobility modernization, green transportation infrastructure, and domestic manufacturing competitiveness. Incentives for local sourcing and compliance with export regulations enhance the competitiveness of domestic frame manufacturers in both local and international markets.

Key players in the Global Bicycle Frames Market include Trek, Cannondale Bikes, Bianchi, Cervelo, Specialized Bicycle, SCOTT Sports, Argon 18, Santa Cruz, Giant Manufacturing, and Canyon. Leading companies in the Global Bicycle Frames Market strengthen their position through strategic approaches. They invest in research and development to launch innovative, lightweight, and high-performance frames, integrating advanced materials and e-bike-ready designs. Firms expand distribution across offline and online channels, ensuring professional fitting and after-sales support. Partnerships with OEMs and component manufacturers enhance co-development and technical collaboration. Marketing emphasizes performance, durability, and sustainability, while strategic global expansion, manufacturing localization, and adherence to regulatory requirements allow companies to capture new markets and reinforce brand reputation in a highly competitive landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Frame

- 2.2.4 Sales Channel

- 2.2.5 Distribution Channel

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising health awareness and cycling adoption.

- 3.2.1.2 Urban mobility shift and traffic congestion solutions.

- 3.2.1.3 Government initiatives promoting cycling infrastructure.

- 3.2.1.4 E-bike market boom driving specialized frame demand.

- 3.2.1.5 Lightweight material demand for performance cycling.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced materials (carbon fiber, titanium).

- 3.2.2.2 Supply chain disruptions and raw material shortages.

- 3.2.2.3 Post-COVID market saturation and excess inventory.

- 3.2.2.4 Price competition from low-cost Asian manufacturers.

- 3.2.3 Market opportunities

- 3.2.3.1 Growing e-bike segment requiring reinforced frames.

- 3.2.3.2 Customization demand enabling premium pricing.

- 3.2.3.3 Sustainable and recycled material innovation.

- 3.2.3.4 Expansion in emerging markets (India, Southeast Asia, LATAM).

- 3.2.3.5 Direct-to-consumer (D2C) business model growth.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Consumer product safety commission (CPSC) bicycle frame Standards

- 3.4.1.2 Canada - Canada consumer product safety act (CCPSA) bicycle regulations

- 3.4.2 Europe

- 3.4.2.1 Germany- DIN standards & EN 15194 E-bike frame certification

- 3.4.2.2 UK- Post-brexit bicycle frame safety & UKCA marking requirements

- 3.4.2.3 France- NF standards & national active mobility certification framework

- 3.4.2.4 Italy- UNI standards & ITS cycling infrastructure integration

- 3.4.3 Asia Pacific

- 3.4.3.1 China- GB standards & MIIT E-bike frame technical regulations

- 3.4.3.2 India- BIS certification & AIS bicycle frame safety standards

- 3.4.3.3 Japan- JIS standards & ministry of land infrastructure transport and tourism bicycle safety framework

- 3.4.3.4 Australia- Australian consumer law & AS/NZS bicycle frame standards

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM bicycle safety standards & active mobility framework

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- SASO standards & vision 2030 active mobility initiatives

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Sensor technology evolution (camera, LiDAR, RADAR, ultrasonic)

- 3.7.1.2 Sensor fusion & integration

- 3.7.1.3 AI & machine learning in pedestrian detection

- 3.7.2 Emerging technologies

- 3.7.2.1 V2X communication for enhanced detection

- 3.7.2.2 Nighttime & low-light detection technologies

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.8.1 Key patent trends

- 3.8.2 Technology innovation hotspots

- 3.8.3 Patent filing by key players

- 3.8.4 Emerging IP strategies

- 3.9 Pricing analysis

- 3.9.1 Historical price trend analysis

- 3.9.2 Aluminum frame price trends (2022-2025)

- 3.9.3 Steel frame price trends (2022-2025)

- 3.9.4 Carbon fiber frame price trends (2022-2025)

- 3.9.5 Titanium frame price trends (2022-2025)

- 3.10 Pricing strategy by player type

- 3.10.1 Premium positioning strategy (titanium, high-modulus carbon)

- 3.10.2 Value segment strategy (aluminum, standard carbon)

- 3.10.3 Cost-plus pricing models (OEM manufacturing)

- 3.11 Use cases & success stories

- 3.12 Case studies

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Impact of AI & generative AI on the market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.2 Design automation & generative engineering

- 3.14.3 Quality control & defect detection systems

- 3.14.4 Demand forecasting & inventory optimization

- 3.15 Risks, limitations & regulatory considerations

- 3.15.1 Data privacy in customer design data

- 3.15.2 AI model reliability in structural engineering

- 3.15.3 Workforce displacement concerns

- 3.16 Future outlook & opportunities

- 3.16.1 Emerging market segments

- 3.16.2 Technology disruptions on the horizon

- 3.16.3 Sustainability trends

- 3.16.4 Business model innovations

- 3.16.5 Long-term growth projections (2030-2040)

- 3.16.6 Strategic recommendations by stakeholder type

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Steel

- 5.4 Carbon Fiber

- 5.5 Titanium

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Frame, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Mountain bicycle

- 6.3 Hybrid bicycle

- 6.4 Electric bicycle

- 6.5 Road bicycle

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Professional/competitive cyclists

- 9.3 Recreational/enthusiast cyclists

- 9.4 Commuters/urban cyclists

- 9.5 Youth cyclists

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Argon 18

- 11.1.2 Bianchi

- 11.1.3 Cannondale Bikes

- 11.1.4 Canyon

- 11.1.5 Cervelo

- 11.1.6 Cicli Pinarello SRL

- 11.1.7 Giant Manufacturing

- 11.1.8 GT Bicycles

- 11.1.9 Kona Bikes

- 11.1.10 Merida

- 11.1.11 Santa Cruz

- 11.1.12 SCOTT Sports

- 11.1.13 Specialized Bicycle

- 11.1.14 Trek

- 11.2 Regional Players

- 11.2.1 Chicago Bicycle Company

- 11.2.2 Ideal Bike

- 11.2.3 Dengfu Sports Equipment

- 11.3 Emerging Players & Technology Enablers

- 11.3.1 Pinion

- 11.3.2 YT Industries

- 11.3.3 Aventon Bikes