|

市場調查報告書

商品編碼

1982381

汽車暖通空調市場機會、成長要素、產業趨勢分析及2026-2035年預測Automotive HVAC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

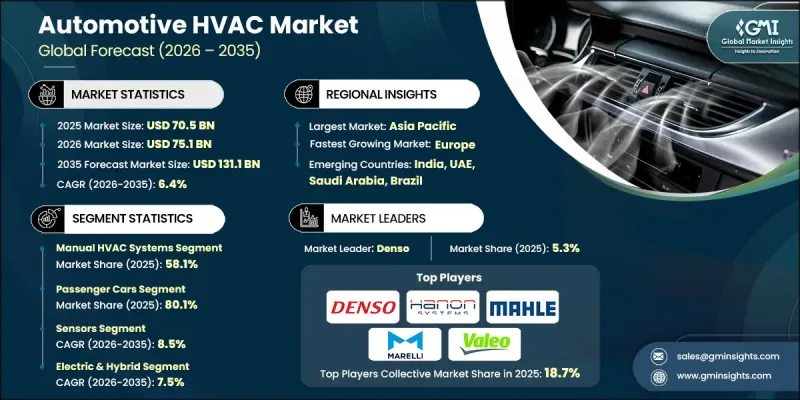

預計到 2025 年,全球汽車 HVAC 市場價值將達到 705 億美元,並預計以 6.4% 的複合年成長率成長,到 2035 年達到 1,311 億美元。

全球汽車保有量的成長推動了市場成長,而可支配收入的增加和消費者出行偏好的轉變也為此提供了支撐。隨著越來越多的消費者購買私家車,對先進的暖通空調(HVAC)系統的需求持續成長。在中檔和豪華車領域,能夠提升車內舒適度和溫度控制性能的先進HVAC技術正被日益廣泛地採用。同時,製造商正在將智慧氣候控制解決方案與先進的感測技術相結合,使車內乘客能夠個性化調節氣流和溫度設定。隨著電動車的快速普及,HVAC系統的效率變得愈發重要,因為這些系統直接影響電池性能和總續航里程。為了應對這項挑戰,各公司正在開發節能解決方案,例如熱泵系統和先進的溫度控管模組。同時,日益嚴格的環境法規正在推動低全球暖化潛能值冷媒、改進的密封系統和可回收零件的應用,從而加速向永續汽車HVAC技術的轉型。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 705億美元 |

| 預測金額 | 1311億美元 |

| 複合年成長率 | 6.4% |

預計到2025年,手動空調系統市佔率將達到58.1%,市場規模將達到409億美元。其主導地位源自於其相比自動化系統更高的成本效益、更簡化的設計和結構,以及更低的製造成本和維護成本。由於電子元件和感測器數量較少,這些系統性能可靠且易於維護,使其成為大規模生產的大型車輛極具吸引力的選擇。其耐用性和較低的技術複雜性也進一步支撐了市場的持續需求。

預計到2025年,乘用車市佔率將達到80.1%,到2035年市場規模將達到1,076億美元。由於乘用車的全球產量和銷售量遠高於商用車,因此該類別對空調系統的需求正在大幅增加。汽車製造商持續致力於提升車內舒適度以滿足消費者期望,進一步鞏固了乘用車市場的主導地位。乘用車正日益整合先進的氣候控制技術,以優先考慮乘員的舒適度和車內體驗。

受高汽車保有量和消費者對舒適性的強烈偏好推動,預計到2025年,美國汽車空調系統市場規模將達到780萬美元。此外,電動和混合動力汽車銷量的成長(這些汽車需要節能型空調系統)也促進了市場成長。包括區域管理和互聯控制在內的智慧氣候控制技術在原廠配套市場和售後市場通路中正得到越來越廣泛的應用。監管措施日益重視車輛能源效率,推動了系統設計和零件最佳化的創新。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 乘客舒適度需求日益成長

- 全球汽車產量增加

- 電動車和混合動力汽車的成長

- 暖通空調系統的技術進步

- 產業潛在風險與挑戰

- 暖通空調系統整合的複雜性

- 嚴格的環境法規

- 市場機遇

- 新興市場需求不斷成長

- 適用於電動車的輕巧緊湊型HVAC設計

- 售後空調升級和改裝

- 與物聯網和聯網汽車系統的整合

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國國家公路交通安全管理局(NHTSA)

- 美國環保署(EPA)

- 加州空氣資源委員會(CARB)

- 加拿大標準協會(CSA)

- 歐洲

- 歐洲汽車製造商協會 (ACEA)

- 歐盟排放交易體系(EU ETS)

- 歐洲標準化委員會(CEN)

- 歐洲環境署(EEA)

- 亞太地區

- 公路運輸和公路部(MoRTH)

- 印度能源效率局 (BEE)

- 中國汽車技術研究中心(CATARC)

- 日本汽車製造商協會(JAMA)

- 拉丁美洲

- INMETRO

- 運輸部

- 國家陸路交通管理局(ANTT)

- 中東和非洲

- 波灣合作理事會標準化組織(GSO)

- ESMA(阿拉伯聯合大公國標準化和計量局)

- 沙烏地阿拉伯標準、計量和品質組織(SASO)

- 南非標準局(SABS)

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 暖通空調系統的電氣化

- 雙區和多區氣候控制

- 車載空氣過濾淨化系統

- 與車輛遠端資訊處理和資訊娛樂系統的整合

- 新興技術

- 熱電式暖通空調系統

- 太陽能空調機組

- 智慧人工智慧空調控制

- 適用於電動車的輕巧緊湊型HVAC設計

- 當前技術趨勢

- 價格趨勢

- 按地區

- 依產品

- 成本細分分析

- 永續性和環境影響

- 環境影響評估

- 社會影響和對當地社區的貢獻

- 公司管治與企業社會責任

- 永續金融與投資趨勢

- 電氣化對暖通空調架構的影響

- 高壓和低壓暖通空調系統的比較

- 車載環境與能源管理的預校準策略

- 解決有關駕駛距離的擔憂

- 雙源暖氣系統

- OEM整合策略與平台方法

- 模組化暖通空調平台的開發

- 車輛架構整合(內燃機與電動車)面臨的挑戰

- 原始設備製造商和供應商之間的共同開發夥伴關係

- 客製化與標準化

- 健康與保健功能的整合

- 高效能空氣過濾器和PM2.5去除功能

- 抗菌抗病毒塗層技術

- 濕度控制,以達到最佳健康狀態

- 過敏原和病原體檢測系統

- 芳香療法和空氣電離功能

- 案例研究

- 未來前景與機遇

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依系統分類,2022-2035年

- 自動空調系統

- 手動空調系統

第6章 市場估計與預測:依組件分類,2022-2035年

- 感應器

- 溫度感測器

- 濕度感測器

- 空氣品質感測器

- 其他

- 熱交換器

- 冷凝器

- 蒸發器

- 壓縮機

- 擴充設備

- 接收器/烘乾機

- 鼓風機電機

- 其他

第7章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- LCV

- MCV

- 重型車輛(HCV)

第8章 市場估算與預測:依促進因素分類,2022-2035年

- 內燃機(ICE)

- 電動/混合動力

- BEV

- HEV

- PHEV

- FCEV

第9章 市場估價與預測:依銷售管道分類,2022-2035年

- OEM

- 售後市場

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 捷克共和國

- 比利時

- 俄羅斯

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 印尼

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 世界公司

- Denso

- Valeo

- Mahle

- Hanon Systems

- Sanden

- Marelli

- Delphi

- Visteon

- Johnson Electric

- 當地公司

- Air International Thermal Systems

- Subros

- Songz

- Shanghai Velle

- Hubei Meibiao

- Bergstrom

- 新興企業

- Gentherm

- Behr Hella Service

- Trans Air Manufacturing

- Motherson

- Modine

The Global Automotive HVAC Market was valued at USD 70.5 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 131.1 billion by 2035.

Market growth is driven by increasing vehicle ownership worldwide, supported by rising disposable income and shifting consumer mobility preferences. As more consumers invest in personal vehicles, demand for advanced heating, ventilation, and air conditioning systems continues to accelerate. Mid-range and premium vehicle categories are increasingly incorporating enhanced HVAC technologies that deliver improved cabin comfort and climate control performance. At the same time, manufacturers are integrating intelligent climate solutions equipped with advanced sensing technologies that allow occupants to personalize airflow and temperature settings. The rapid growth of electric vehicles has further elevated the importance of HVAC efficiency, as these systems directly influence battery performance and overall driving range. To address this, companies are developing energy-efficient solutions such as heat pump systems and advanced thermal management modules. In parallel, evolving environmental regulations are encouraging the adoption of low global warming potential refrigerants, improved sealing systems, and recyclable components, reinforcing the shift toward sustainable automotive HVAC technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $70.5 Billion |

| Forecast Value | $131.1 Billion |

| CAGR | 6.4% |

The manual HVAC systems segment accounted for 58.1% share in 2025, generating USD 40.9 billion. Their leadership position stems from cost efficiency, simplified design architecture, and lower production and maintenance expenses compared to automatic systems. With fewer electronic components and sensors, these systems offer dependable performance and straightforward servicing, making them highly attractive across large vehicle production volumes. Their durability and reduced technical complexity further support sustained demand.

The passenger cars segment held 80.1% share in 2025 and is forecast to reach USD 107.6 billion by 2035. Higher global production and sales volumes of passenger vehicles compared to commercial vehicles significantly increase HVAC system demand within this category. Automakers continue to enhance cabin comfort features to meet consumer expectations, reinforcing segment dominance. Passenger vehicles prioritize occupant comfort and interior experience, which drives greater integration of advanced climate control technologies.

U.S. Automotive HVAC Market reached USD 7.8 million in 2025, supported by high vehicle ownership rates and strong consumer preference for comfort-oriented features. Growth is further driven by the expansion of electric and hybrid vehicle sales, which require optimized energy-efficient HVAC systems. Smart climate control technologies, including zonal management and connected controls, are gaining traction in both OEM and aftermarket channels. Regulatory measures increasingly emphasize vehicle energy efficiency, reinforcing innovation in system design and component optimization.

Leading companies operating in the Global Automotive HVAC Market include Valeo, Denso, Marelli, Hanon Systems, Sensata, Mahle, Air International Thermal Systems, Sanden, Johnson Electric, and Visteon. Companies in the Global Automotive HVAC Market are strengthening their competitive positions through continuous innovation and strategic partnerships. Major players are investing in advanced thermal management technologies, energy-efficient compressors, and intelligent climate control systems tailored for electric and hybrid vehicles. Collaboration with automakers enables early integration of next-generation HVAC platforms into new vehicle architectures. Firms are expanding global manufacturing footprints to improve supply chain resilience and reduce production costs. Research and development efforts focus on lightweight materials, smart sensors, and environmentally friendly refrigerants to comply with tightening emission regulations.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System

- 2.2.3 Component

- 2.2.4 Vehicle

- 2.2.5 Propulsion

- 2.2.6 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for passenger comfort

- 3.2.1.2 Rising vehicle production globally

- 3.2.1.3 Growth in electric and hybrid vehicles

- 3.2.1.4 Technological advancements in HVAC systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexity in HVAC system integration

- 3.2.2.2 Stringent environmental regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in emerging markets

- 3.2.3.2 Lightweight and compact HVAC designs for EVs

- 3.2.3.3 Aftermarket HVAC upgrades and retrofitting

- 3.2.3.4 Integration with IoT and connected vehicle systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Environmental Protection Agency (EPA)

- 3.4.1.3 California Air Resources Board (CARB)

- 3.4.1.4 Canadian Standards Association (CSA)

- 3.4.2 Europe

- 3.4.2.1 European Automobile Manufacturers’ Association (ACEA)

- 3.4.2.2 European Union Emissions Trading System (EU ETS)

- 3.4.2.3 European Committee for Standardization (CEN)

- 3.4.2.4 European Environment Agency (EEA)

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Road Transport and Highways (MoRTH)

- 3.4.3.2 Bureau of Energy Efficiency (BEE)

- 3.4.3.3 China Automotive Technology & Research Center (CATARC)

- 3.4.3.4 Japan Automobile Manufacturers Association (JAMA)

- 3.4.4 Latin America

- 3.4.4.1 INMETRO

- 3.4.4.2 Ministry of Transport

- 3.4.4.3 National Agency for Land Transportation (ANTT)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council Standardization Organization (GSO)

- 3.4.5.2 Emirates Authority for Standardization & Metrology (ESMA)

- 3.4.5.3 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.4 South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Electrification of HVAC Systems

- 3.7.1.2 Dual-Zone and Multi-Zone Climate Control

- 3.7.1.3 Cabin Air Filtration and Purification Systems

- 3.7.1.4 Integration with Vehicle Telematics and Infotainment

- 3.7.2 Emerging technologies

- 3.7.2.1 Thermoelectric HVAC Systems

- 3.7.2.2 Solar-Powered HVAC Units

- 3.7.2.3 Smart and AI-Enabled Climate Control

- 3.7.2.4 Lightweight and Compact HVAC Designs for EVs

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Electrification impact on HVAC architecture

- 3.11.1 High voltage vs. low voltage HVAC system comparison

- 3.11.2 Cabin preconditioning strategies and energy management

- 3.11.3 Range anxiety mitigation

- 3.11.4 Dual-source heating systems

- 3.12 OEM integration strategies and platform approaches

- 3.12.1 Modular HVAC platform development

- 3.12.2 Vehicle architecture integration challenges (ICE vs. EV)

- 3.12.3 Co-development partnerships between OEMs and suppliers

- 3.12.4 Customization vs. standardization

- 3.13 Health and wellness feature integration

- 3.13.1 HEPA filtration and PM2.5 removal capabilities

- 3.13.2 Antimicrobial and antiviral coating technologies

- 3.13.3 Humidity control for health optimization

- 3.13.4 Allergen and pathogen detection systems

- 3.13.5 Aromatherapy and air ionization features

- 3.14 Case studies

- 3.15 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By System, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Automatic HVAC systems

- 5.3 Manual HVAC systems

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Sensors

- 6.2.1 Temperature sensors

- 6.2.2 Humidity sensors

- 6.2.3 Air quality sensors

- 6.2.4 Others

- 6.3 Heat exchangers

- 6.3.1 Condenser

- 6.3.2 Evaporator

- 6.4 Compressor

- 6.5 Expansion device

- 6.6 Receiver/drier

- 6.7 Blower motor

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Electric & hybrid

- 8.3.1 BEV

- 8.3.2 HEV

- 8.3.3 PHEV

- 8.3.4 FCEV

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Czech Republic

- 10.3.7 Belgium

- 10.3.8 Russia

- 10.3.9 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.4.10 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Denso

- 11.1.2 Valeo

- 11.1.3 Mahle

- 11.1.4 Hanon Systems

- 11.1.5 Sanden

- 11.1.6 Marelli

- 11.1.7 Delphi

- 11.1.8 Visteon

- 11.1.9 Johnson Electric

- 11.2 Regional players

- 11.2.1 Air International Thermal Systems

- 11.2.2 Subros

- 11.2.3 Songz

- 11.2.4 Shanghai Velle

- 11.2.5 Hubei Meibiao

- 11.2.6 Bergstrom

- 11.3 Emerging players

- 11.3.1 Gentherm

- 11.3.2 Behr Hella Service

- 11.3.3 Trans Air Manufacturing

- 11.3.4 Motherson

- 11.3.5 Modine

汽車PTC加熱器市場:2026年至2032年全球市場預測(按車輛類型、材料、額定功率、技術、燃料類型、應用和最終用戶分類)

汽車PTC加熱器市場:2026年至2032年全球市場預測(按車輛類型、材料、額定功率、技術、燃料類型、應用和最終用戶分類) 汽車暖通空調系統市場規模、佔有率、趨勢和預測報告:按組件、技術、車輛類型和地區分類,2026-2034年

汽車暖通空調系統市場規模、佔有率、趨勢和預測報告:按組件、技術、車輛類型和地區分類,2026-2034年 汽車空調系統:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

汽車空調系統:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 汽車暖通空調(HVAC)全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)日本汽車空調市場規模、佔有率、趨勢及預測(按組件、技術、車輛類型及地區分類),2026-2034年

汽車暖通空調(HVAC)全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)日本汽車空調市場規模、佔有率、趨勢及預測(按組件、技術、車輛類型及地區分類),2026-2034年 2026年全球汽車HVAC鼓風機馬達市場研究報告

2026年全球汽車HVAC鼓風機馬達市場研究報告 2026年全球汽車冷藏庫市場報告2026年全球汽車暖通空調市場報告

2026年全球汽車冷藏庫市場報告2026年全球汽車暖通空調市場報告 汽車暖通空調市場-全球產業規模、佔有率、趨勢、機會與預測:按車輛類型、零件類型、技術類型、地區和競爭格局分類,2021-2031年汽車空調市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、組件、車輛類型、地區和競爭格局分類,2021-2031年

汽車暖通空調市場-全球產業規模、佔有率、趨勢、機會與預測:按車輛類型、零件類型、技術類型、地區和競爭格局分類,2021-2031年汽車空調市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、組件、車輛類型、地區和競爭格局分類,2021-2031年