|

市場調查報告書

商品編碼

1982360

碳管理系統市場機會、成長要素、產業趨勢分析及2026-2035年預測Carbon Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

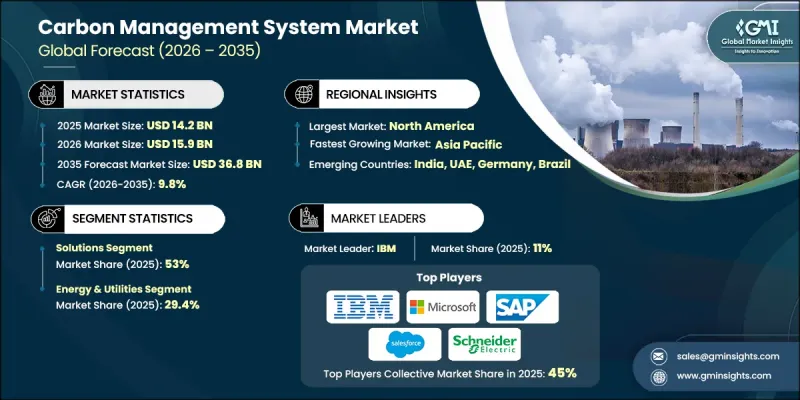

全球碳管理系統市場預計到 2025 年將價值 142 億美元,預計到 2035 年將以 9.8% 的複合年成長率成長至 368 億美元。

由於技術創新、監管壓力和企業永續發展優先事項的轉變,碳管理市場正在經歷轉型。企業正擴大採用碳管理解決方案,以實現全球氣候目標、管理營運排放並降低氣候相關風險。雲端平台的興起,以及人工智慧 (AI)、機器學習 (ML) 和物聯網 (IoT) 技術的融合,正在重塑碳管理實踐,實現即時監測、預測分析和自動化報告,從而提高準確性和營運效率。環境、社會和管治(ESG) 報告已成為一項策略要求,促使碳管理服務提供者提供整合的 ESG 工具,用於追蹤排放、能源消耗和更廣泛的永續發展措施。生命週期評估也日益重要,使企業能夠量化產品製造、物流、使用和處置階段的排放,從而提供可操作的數據,以減少整個供應鏈的碳足跡。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 142億美元 |

| 預測金額 | 368億美元 |

| 複合年成長率 | 9.8% |

預計到 2025 年,解決方案領域將佔據 53% 的市場佔有率,到 2035 年將以 9.4% 的複合年成長率成長。製造業、能源和交通運輸業排放概況的日益複雜化,推動了對提供預測分析、即時追蹤和 ESG 報告功能的企業級 CMS 平台的需求。

預計到2025年,能源和公共產業產業將佔據29.4%的市場佔有率,到2035年將以10%的複合年成長率成長。由於該產業溫室氣體排放龐大,因此是碳管理系統(CMS)應用的主要目標領域。隨著公共產業不斷擴大可再生能源、儲能、智慧電網和綠色費率方案的應用,亟需能夠即時準確量化碳排放強度,並提供透明、可審計數據的系統,以用於規劃和客戶報告。

美國碳管理系統市場佔82%的佔有率,預計2025年市場規模將達39億美元。監管要求已將排放管理轉變為營運必需環節,尤其是在油氣基礎設施的甲烷排放管理方面。各公司正利用碳管理系統平台整合感測器和衛星數據,實現洩漏偵測和修復工作流程的自動化,將技術估計值與實際測量結果進行核對,並維護可供執法部門審計的記錄。州級法規和採購計畫也在推動將範圍1-3的數據整合到資金籌措和合約中,使碳管理系統從單純的合規工具提升為核心的營運、風險和財務系統。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTEL 分析

- 新機會和趨勢

- 數位化和物聯網整合

- 進入新興市場

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 策略舉措

- 競爭性標竿分析

- 戰略儀錶板

- 創新與科技趨勢

第5章 市場規模及預測:依組件分類,2022-2035年

- 解決方案

- 服務

第6章 市場規模及預測:依市場進入方式分類,2022-2035年

- 雲

- 現場

第7章 市場規模及預測:依產業分類,2022-2035年

- 能源與公共產業

- 製造業

- 住宅/商業建築

- 運輸/物流

- 資訊科技/通訊

- 其他

第8章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第9章:公司簡介

- Accuvio

- Carbon Footprint Ltd.

- Dakota Software

- Enablon

- EnergyCap

- Engie

- Enviance

- Envirosoft

- ESP

- IBM

- Intelex

- Isometrix

- Locus Technologies

- NativeEnergy

- Salesforce

- SAP

- Schneider Electric

- Trinity Consultants

- Watershed

- Zevero

The Global Carbon Management System Market was valued at USD 14.2 billion in 2025 and is estimated to grow at a CAGR of 9.8% to reach USD 36.8 billion by 2035.

The market is transformed by a combination of technological innovation, regulatory pressure, and evolving corporate sustainability priorities. Businesses are increasingly adopting CMS solutions to align with global climate targets, manage operational emissions, and mitigate climate-related risks. The rise of cloud-based platforms, along with the integration of Artificial Intelligence (AI), Machine Learning (ML), and Internet of Things (IoT) technologies, is reshaping carbon management practices, enabling real-time monitoring, predictive insights, and automated reporting for improved accuracy and operational efficiency. Environmental, Social, and Governance (ESG) reporting has become a strategic imperative, prompting CMS providers to offer integrated ESG tools that track emissions, energy consumption, and broader sustainability initiatives. Lifecycle assessments are also gaining prominence, allowing organizations to quantify emissions from product manufacturing, logistics, use, and end-of-life disposal, providing actionable data to reduce carbon footprints across supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.2 Billion |

| Forecast Value | $36.8 Billion |

| CAGR | 9.8% |

The solutions segment held 53% share in 2025 and is anticipated to grow at a CAGR of 9.4% through 2035. Rising complexity in emissions profiles across manufacturing, energy, and transport sectors is driving demand for enterprise-grade CMS platforms offering predictive analytics, real-time tracking, and ESG reporting capabilities.

The energy and utilities segment held 29.4% share in 2025 and is projected to grow at a CAGR of 10% by 2035. The sector is a major adopter of CMS due to its substantial greenhouse gas emissions. As utilities increase renewable integration, storage, smart grids, and green tariff offerings, they require systems that quantify carbon intensity accurately in real time and provide transparent, auditable data for planning and customer reporting.

U.S. Carbon Management System Market held 82% share, generating USD 3.9 billion in 2025. Regulatory mandates are converting emissions management into operational imperatives, particularly for methane across oil and gas infrastructure. Companies are leveraging CMS platforms to integrate sensor and satellite data, automate leak detection and repair workflows, reconcile engineering estimates with actual measurements, and maintain auditable records suitable for enforcement. State-level regulations and procurement programs are also driving Scope 1-3 data integration into financing and contracts, elevating CMS from a compliance tool to a core operational, risk, and financial system.

Key players in the Global Carbon Management System Market include: Engie, SAP, Enablon, Watershed, Locus Technologies, Accuvio, Dakota Software, IBM, EnergyCap, Intelex, Zevero, NativeEnergy, ESP, Isometrix, Schneider Electric, Carbon Footprint Ltd., Envirosoft, Trinity Consultants, Salesforce, and Enviance. Companies in the Carbon Management System Market are employing strategic initiatives to strengthen their position and expand market presence. They are investing heavily in AI, IoT, and cloud-based innovations to deliver real-time emissions monitoring, predictive analytics, and automated ESG reporting. Strategic alliances and partnerships with utilities, manufacturing firms, and government agencies improve market access and long-term adoption. Companies are expanding globally, localizing solutions to meet regional compliance standards, and integrating CMS platforms with energy management, sustainability, and finance systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Component trends

- 2.1.3 Deployment trends

- 2.1.4 Industry trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Component, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Solutions

- 5.3 Services

Chapter 6 Market Size and Forecast, By Deployment, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premises

Chapter 7 Market Size and Forecast, By Industry, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Energy & utilities

- 7.3 Manufacturing

- 7.4 Residential & commercial building

- 7.5 Transportation & logistics

- 7.6 IT & telecom

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 UK

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 Accuvio

- 9.2 Carbon Footprint Ltd.

- 9.3 Dakota Software

- 9.4 Enablon

- 9.5 EnergyCap

- 9.6 Engie

- 9.7 Enviance

- 9.8 Envirosoft

- 9.9 ESP

- 9.10 IBM

- 9.11 Intelex

- 9.12 Isometrix

- 9.13 Locus Technologies

- 9.14 NativeEnergy

- 9.15 Salesforce

- 9.16 SAP

- 9.17 Schneider Electric

- 9.18 Trinity Consultants

- 9.19 Watershed

- 9.20 Zevero

2026年全球雲端排放管理市場報告

2026年全球雲端排放管理市場報告 脫碳軟體市場:按類型、可近性、技術、部署模式、企業規模和最終用戶產業分類-2026-2032年全球預測2026年全球雲碳管理系統市場報告碳管理軟體市場:按組件、應用、部署類型、最終用戶產業、組織類型和企業規模分類-2026-2032年全球預測2026年智慧碳全球市場報告2026年全球碳管理系統市場報告

脫碳軟體市場:按類型、可近性、技術、部署模式、企業規模和最終用戶產業分類-2026-2032年全球預測2026年全球雲碳管理系統市場報告碳管理軟體市場:按組件、應用、部署類型、最終用戶產業、組織類型和企業規模分類-2026-2032年全球預測2026年智慧碳全球市場報告2026年全球碳管理系統市場報告 智慧碳足跡分析市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、模組、功能分類酵素催化二氧化碳還原市場分析及預測(至2035年):依類型、產品、服務、技術、應用、材料類型、製程、最終用戶、功能及設備分類

智慧碳足跡分析市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、模組、功能分類酵素催化二氧化碳還原市場分析及預測(至2035年):依類型、產品、服務、技術、應用、材料類型、製程、最終用戶、功能及設備分類 2026-2034年全球能源和公共產業碳管理系統市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球能源和公共產業碳管理系統市場規模、佔有率、趨勢和成長分析報告 碳管理軟體市場規模、佔有率、趨勢及預測(按組件、應用、垂直產業及地區分類),2026-2034年

碳管理軟體市場規模、佔有率、趨勢及預測(按組件、應用、垂直產業及地區分類),2026-2034年