|

市場調查報告書

商品編碼

1982356

遠程操作車輛市場機會、成長要素、產業趨勢分析及2026-2035年預測。Remote Operated Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

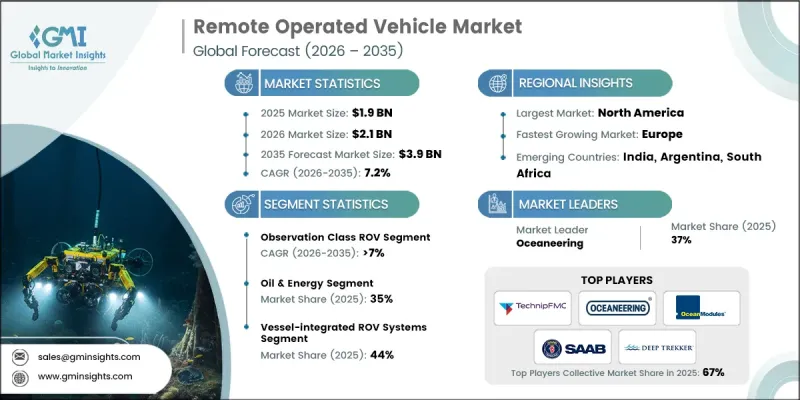

全球遙控潛水器(ROV)市場預計到 2025 年價值 19 億美元,預計到 2035 年將以 7.2% 的複合年成長率成長至 39 億美元。

研究機構和政府部門對先進海洋技術的資金支持不斷增加,顯著加速了市場成長。遙控探勘(ROV)擴大被部署到複雜的海底任務中,這些任務需要高解析度影像、先進感測器以及在人類無法觸及的深海中進行精確操控。這些系統在收集環境資訊方面發揮著至關重要的作用,為海洋科學、海洋學評估、生物多樣性分析和氣候相關研究提供支援。人們對永續海洋管理和全球環境監測計畫日益成長的興趣進一步推動了ROV的應用。同時,石油、天然氣和可再生能源領域的海上基礎設施擴張也持續催生了對可靠水下機器人的需求。 ROV能夠提高作業安全性、提升成本效益,並最大限度地減少人員暴露於危險海底環境的風險。其實即時資料傳輸、精確的操作能力和遠端介入能力支援持續的水下作業。 ROV在國防和海上安全領域的應用不斷擴展,進一步鞏固了全球遠程操作車輛(ROV)產業的長期成長動能。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 19億美元 |

| 預測金額 | 39億美元 |

| 複合年成長率 | 7.2% |

遠程操作車輛(ROV)市場的產業相關人員正積極尋求非內部成長策略,例如推出新產品、收購和建立策略聯盟,以保持競爭優勢。對海上能源投資的增加顯著提升了對海底檢測、干預和建造服務的需求。 ROV系統能夠在確保作業精度和成本控制的同時,安全地進入惡劣的水下環境。它們能夠以最小的停機時間完成技術難度極高的任務,這增強了ROV在整個能源相關產業(該產業依賴不間斷的海底作業)的價值提案。此外,國防領域的現代化建設也正在推動先進遙控系統在海上作業的應用。

預計到2025年,觀測型ROV市佔率將達到35%,並在2026年至2035年間以7%的複合年成長率成長。這些緊湊型系統因其價格實惠、易於部署和高機動性,被廣泛應用於各行各業的常規水下評估。它們尤其適用於對水下基礎設施和需要持續監測的關鍵資產進行目視檢查。法律規範和不斷成長的資產保護要求正在加速對高清視覺數據解決方案的需求,從而推動全球觀測型ROV市場的持續擴張。

預計到2025年,石油和能源產業將佔據35%的市場佔有率,並在2026年至2035年間以6.5%的複合年成長率成長。在更深、技術更複雜的儲存中持續進行的海上油氣探勘活動,大大推動了水下機器人(ROV)的應用。作業者依靠先進的系統來支援鑽井作業、檢查設備、安裝海底組件以及維護管道基礎設施。這些水下機器人能夠在惡劣的海底環境中提供高效、高精度的干涉能力,從而保障作業的連續性,提升安全標準,並提高整體油氣採收率。

美國遠程操作車輛(ROV)市場佔有71%的佔有率,預計到2025年市場規模將達到5.28億美元。推動美國對先進ROV系統需求的主要動力是持續的海洋能源生產活動。高效能的遠端操作技術對於海洋資產的日常維護、深海開發和海底基礎設施的升級改造至關重要。透過持續監測和系統升級來延長老舊海洋設施的運作,進一步提升了船隊的穩定運作和市場的長期穩定性。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 擴大海上油氣探勘

- 離岸風力發電的快速發展

- 擴大國防和海軍現代化計劃

- 海底通訊和電力電纜基礎設施的成長

- 機器人技術和人工智慧整合的技術進步

- 產業潛在風險與挑戰

- 高昂的資本和營運成本

- 熟練操作人員短缺

- 惡劣的海洋作業環境

- 對海洋能量循環的依賴

- 市場機遇

- 深海採礦活動的擴張

- 擴大海洋研究和環境監測

- 水產養殖和近海養殖業務的擴張

- 與自主水下航行器(AUV)的整合

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國船舶意外排放法案

- 美國海岸警衛隊防衛隊安全規章

- 美國安全與環境執法局(BSEE)海事規則

- 歐洲

- 歐盟海事安全指令

- 符合CE標誌和機械指令。

- 各國海事當局之間的差異

- 海上可再生能源法規

- 有關潛水員安全和水下作業的規定

- 亞太地區

- 中國的離岸法律規範

- 印度的離岸法規環境

- 東協在海洋協調方面所做的努力

- 日本海洋和近海框架

- 澳洲和韓國離岸合規標準

- 拉丁美洲

- 巴西海事法律規範

- 墨西哥海事安全與環境法規

- 為協調區域海洋開發法規所做的努力

- 中東和非洲

- 海灣合作理事會海事法規結構

- 南非海事安全法規

- 西非和紅海海洋開發法規

- 北美洲

- 關鍵市場趨勢與轉型

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 生產統計

- 生產基地

- 消費者群體

- 進出口

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 關於碳足跡的考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依類型分類,2022-2035年

- 工作用遙控潛水器

- 用於輕型作業的遙控潛水器

- 用於觀察的遙控潛水器

- 微型/迷你型遙控潛水器

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 水產養殖

- 商業潛水和打撈潛水

- 地方政府基礎設施

- 軍隊

- 石油與能源

- 其他

第7章 市場估計與預測:依深度分類,2022-2035年

- 淺海遙控潛水器(水深1000公尺以下)

- 中深度ROV(1,000-3,000公尺海水)

- 深海遙控潛水器(水深3000-6000公尺)

- 超深海遙控潛水器(水深6000公尺或以上)

第8章 市場估算與預測:依系統結構,2022-2035年

- 船載整合式ROV系統

- 模組化貨櫃式水下機器人系統

- 全容器化水下機器人系統

第9章 市場估計與預測:依地區分類,2021-2034年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 北歐國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 東南亞

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中東和非洲(MEA)

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第10章:公司簡介

- 世界公司

- DeepOcean

- DOF Subsea

- Forum Energy Technologies

- Fugro

- Kongsberg Maritime

- Oceaneering International

- Saab Seaeye

- Saipem

- SLB(Schlumberger)

- TechnipFMC

- 當地公司

- ROVOP

- AC-CESS Co UK

- Anritsu Corp

- Deep Ocean Engineering

- Deep Ocean Search

- SEAMOR Marine

- Seatronics

- 新興企業

- Deep Trekker

- Rovtech

- VideoRay

The Global Remote Operated Vehicle Market was valued at USD 1.9 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 3.9 billion by 2035.

Growing financial support from research institutions and government bodies for advanced marine technologies is significantly accelerating market growth. Remote operated vehicles are increasingly deployed for complex subsea missions that require high-resolution imaging, advanced sensors, and precise maneuverability at extreme depths beyond human reach. These systems play a critical role in collecting environmental intelligence that supports marine science, oceanographic assessments, biodiversity analysis, and climate-related studies. The rising emphasis on sustainable ocean management and global environmental monitoring programs continues to strengthen adoption. In parallel, expanding offshore infrastructure across oil, gas, and renewable energy sectors is creating sustained demand for dependable underwater robotics. ROVs enhance operational safety, improve cost efficiency, and minimize human exposure to hazardous subsea environments. Their ability to deliver real-time data transmission, accurate manipulation capabilities, and remote-controlled intervention supports continuous underwater operations. Increased utilization across defense and maritime security applications further reinforces the long-term expansion trajectory of the global remote operated vehicle industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.9 Billion |

| CAGR | 7.2% |

Industry participants in the remote operated vehicle market are actively implementing inorganic growth initiatives, including product introductions, acquisitions, and strategic collaborations, to maintain competitive positioning. Rising offshore energy investments are driving substantial demand for subsea inspection, intervention, and construction services. ROV systems provide safe access to challenging underwater environments while ensuring operational precision and cost control. Their capability to execute technically demanding tasks with minimal downtime has strengthened their value proposition across energy-driven industries that rely on uninterrupted subsea performance. Additionally, expanding defense modernization efforts are contributing to greater integration of advanced remotely operated systems within maritime operations.

The observation class ROV segment accounted for 35% share in 2025 and is anticipated to grow at a CAGR of 7% from 2026 to 2035. These compact systems are widely adopted for routine underwater assessments across multiple industries due to their affordability, ease of deployment, and high maneuverability. They are particularly suited for visual inspections of submerged infrastructure and critical assets requiring consistent monitoring. Increasing regulatory oversight and asset integrity requirements are accelerating demand for high-definition visual data solutions, supporting sustained expansion of the observation class category worldwide.

The oil & energy segment held a 35% share in 2025 and is forecast to grow at a CAGR of 6.5% between 2026 and 2035. Continued offshore hydrocarbon exploration activities in deeper and more technically complex reservoirs are significantly contributing to ROV deployment. Operators rely on advanced systems to assist drilling operations, perform equipment inspections, install subsea components, and maintain pipeline infrastructure. These vehicles provide efficient, high-precision intervention capabilities that support operational continuity, enhance safety standards, and improve overall hydrocarbon recovery performance in demanding subsea conditions.

United States Remote Operated Vehicle Market held 71% share, generating USD 528 million in 2025. Sustained offshore energy production activities are a major driver of demand for advanced work-class ROV systems in the country. Ongoing maintenance of offshore assets, deepwater developments, and subsea infrastructure upgrades requires highly capable remotely operated technologies. Efforts to extend the operational life of mature offshore facilities through continuous monitoring and system upgrades further support steady fleet utilization and long-term market stability.

Key companies operating in the Global Remote Operated Vehicle Market include Forum Energy Technologies, Halma Deep Trekker, Ocean Modules, Oceaneering, Saab Seaeye, Saipem, Seamor, SLB, TechnipFMC, and VideoRay. Companies within the Global Remote Operated Vehicle Market are strengthening their competitive position by investing in research and development to introduce technologically advanced and energy-efficient systems. Strategic mergers, acquisitions, and partnerships enable broader product portfolios and expanded geographic reach. Many firms are focusing on modular system designs, enhanced data analytics integration, and improved sensor capabilities to increase operational flexibility. Establishing regional service hubs and long-term maintenance agreements with offshore operators helps secure recurring revenue streams.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Class

- 2.2.3 Application

- 2.2.4 Depth rating

- 2.2.5 System architecture

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of offshore oil & gas exploration

- 3.2.1.2 Rapid growth of offshore wind energy

- 3.2.1.3 Rising defense and naval modernization programs

- 3.2.1.4 Growth in subsea telecom and power cable infrastructure

- 3.2.1.5 Technological advancements in robotics and AI integration

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital and operational costs

- 3.2.2.2 Skilled operator shortage

- 3.2.2.3 Harsh offshore operating environments

- 3.2.2.4 Dependency on offshore energy cycles

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of deep-sea mining activities

- 3.2.3.2 Growth in marine research and environmental monitoring

- 3.2.3.3 Rising aquaculture and offshore farming operations

- 3.2.3.4 Integration with autonomous underwater vehicles (AUVs)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US Vessel Incidental Discharge Act

- 3.4.1.2 US coast guard safety regulations

- 3.4.1.3 Bureau of Safety and Environmental Enforcement (BSEE) Offshore Rules

- 3.4.2 Europe

- 3.4.2.1 EU Offshore Safety Directive

- 3.4.2.2 CE Marking & Machinery Directive Compliance

- 3.4.2.3 National Maritime Authority Variations

- 3.4.2.4 Offshore Renewable Energy Regulations

- 3.4.2.5 Diver Safety & Subsea Intervention Regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 Chinese Offshore Regulatory Framework

- 3.4.3.2 Indian Offshore Regulatory Environment

- 3.4.3.3 ASEAN Maritime Harmonization Efforts

- 3.4.3.4 Japanese Maritime & Offshore Framework

- 3.4.3.5 Australia & South Korea Offshore Compliance Standards

- 3.4.4 Latin America

- 3.4.4.1 Brazilian Offshore Regulatory Framework

- 3.4.4.2 Mexican Offshore Safety & Environmental Regulations

- 3.4.4.3 Regional Offshore Harmonization Initiatives

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Offshore Regulatory Framework

- 3.4.5.2 South African Maritime Safety Regulations

- 3.4.5.3 West Africa & Red Sea Offshore Development Regulations

- 3.4.1 North America

- 3.5 Major market trends and disruptions

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Cost breakdown analysis

- 3.13 Patent analysis

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Class, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Work class ROV

- 5.3 Light work class ROV

- 5.4 Observation class ROV

- 5.5 Micro/mini ROV

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Aquaculture

- 6.3 Commercial & salvage diving

- 6.4 Municipal INFRASTRUCTURE

- 6.5 Military

- 6.6 Oil & Energy

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Depth Rating, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Shallow water ROVs (≤1,000 msw)

- 7.3 Mid-water ROVs (1,000-3,000 msw)

- 7.4 Deepwater ROVs (3,000-6,000 msw)

- 7.5 Ultra-deepwater ROVs (more than 6,000 msw)

Chapter 8 Market Estimates & Forecast, By System Architecture, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Vessel-integrated ROV systems

- 8.3 Modular containerized ROV systems

- 8.4 Fully containerized ROV systems

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 DeepOcean

- 10.1.2 DOF Subsea

- 10.1.3 Forum Energy Technologies

- 10.1.4 Fugro

- 10.1.5 Kongsberg Maritime

- 10.1.6 Oceaneering International

- 10.1.7 Saab Seaeye

- 10.1.8 Saipem

- 10.1.9 SLB (Schlumberger)

- 10.1.10 TechnipFMC

- 10.2 Regional Players

- 10.2.1 ROVOP

- 10.2.2 AC-CESS Co UK

- 10.2.3 Anritsu Corp

- 10.2.4 Deep Ocean Engineering

- 10.2.5 Deep Ocean Search

- 10.2.6 SEAMOR Marine

- 10.2.7 Seatronics

- 10.3 Emerging Players

- 10.3.1 Deep Trekker

- 10.3.2 Rovtech

- 10.3.3 VideoRay

2026年全球遠距獸醫處方服務市場報告

2026年全球遠距獸醫處方服務市場報告 汽車遠端車輛診斷市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署狀態、最終用戶、功能、解決方案車輛遠距離診斷市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、設備、流程、最終用戶、解決方案

汽車遠端車輛診斷市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署狀態、最終用戶、功能、解決方案車輛遠距離診斷市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、設備、流程、最終用戶、解決方案 人工智慧遠距離診斷市場預測至2034年:全球組件、技術、設備類型、連接方式、應用、最終用戶和區域分析獸醫遠距離診斷市場預測至2034年—按產品類型、動物種類、技術、應用、最終用戶和地區分類的全球分析遠程操作車輛(ROV)市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、最終用戶、功能及安裝類型分類2026年全球車輛日誌軟體市場報告2026年全球遠程車輛廢氣感知器市場報告2026年全球遠端車輛診斷通訊市場報告

人工智慧遠距離診斷市場預測至2034年:全球組件、技術、設備類型、連接方式、應用、最終用戶和區域分析獸醫遠距離診斷市場預測至2034年—按產品類型、動物種類、技術、應用、最終用戶和地區分類的全球分析遠程操作車輛(ROV)市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、最終用戶、功能及安裝類型分類2026年全球車輛日誌軟體市場報告2026年全球遠程車輛廢氣感知器市場報告2026年全球遠端車輛診斷通訊市場報告 遠端車輛關閉市場規模、佔有率和成長分析(按系統、車輛類型和地區分類)-2026-2033年產業預測

遠端車輛關閉市場規模、佔有率和成長分析(按系統、車輛類型和地區分類)-2026-2033年產業預測