|

市場調查報告書

商品編碼

1982355

太空機器人市場機會、成長要素、產業趨勢以及 2026-2035 年預測的分析。Space Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

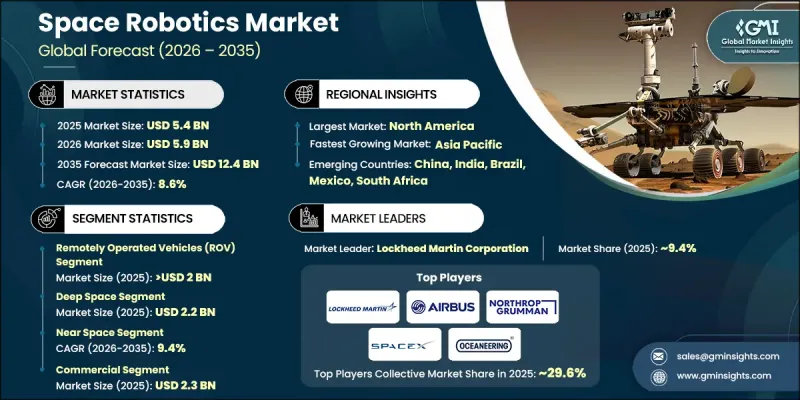

預計到 2025 年,全球空間機器人市場價值將達到 54 億美元,並預計以 8.6% 的複合年成長率成長,到 2035 年達到 124 億美元。

隨著太空任務日益複雜和規模化,該領域也在不斷擴展,對能夠在各種地外環境中運行的先進機器人和自動化技術的需求也隨之成長。航太機構和私人企業正在開發機器人系統,以支援深空長期任務,減少對太空人的依賴,並提高運作效率。這些系統旨在應用於包括太空維護、組裝和行星探勘在內的廣泛領域,從而實現更頻繁、更複雜、更經濟高效的任務。將機器人技術整合到太空計劃中,可以實現即時監控、自動化任務執行和任務支持,而這些工作原本會給人力資源帶來沉重負擔。各國政府、研究機構和私人企業正攜手合作,推動創新,確保機器人技術在未來的太空行動中發揮關鍵作用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 54億美元 |

| 預測金額 | 124億美元 |

| 複合年成長率 | 8.6% |

由於遠程操作車輛(ROV)在太空探勘、在軌道檢查、探測車和太空站運行中發揮至關重要的作用,預計到2025年,ROV市場規模將達到20億美元。 ROV作為一種多功能平台,能夠在危險和難以進入的環境中進行遠端作業,利用即時控制和自主能力來支援表面探勘、樣本採集和在軌維護。

預計到2025年,商業航太領域市場規模將達到23億美元,主要得益於從事衛星部署、太空旅遊、在軌製造和商業太空站建設的私人航太公司的快速擴張。商業航太機器人技術廣泛應用於衛星管理、發射操作、檢查和維護,從而實現擴充性且經濟高效的營運。強勁的私人投資、不斷提高的發射頻率以及技術創新正在進一步加速商業任務中航太機器人技術的應用。

預計到2025年,北美太空機器人市佔率將達到38.5%。這一成長主要得益於政府的大量投入、蓬勃發展的太空探勘計劃、國防相關舉措以及對太空基礎設施的投資。北美政府機構和企業正利用長期專案開發先進的機器人平台,從而鞏固該地區在太空機器人技術領域的領先地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 衛星星系和深空任務的擴展

- 對自主和人工智慧驅動的太空行動的需求日益成長

- 太空旅遊和商業航太活動的成長

- 擴大太空計畫中的公私合營

- 對在軌服務、太空碎片清除和衛星維護的需求。

- 產業潛在風險與挑戰

- 開發成本高且技術複雜

- 在惡劣且不可預測的太空環境中開展業務的風險

- 市場機遇

- 擴大自主機器人系統在太空任務中的應用

- 對在軌服務、組裝和製造(ISAM)的需求不斷成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域部署對比

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 財務績效比較

- 2022-2025 年重大發展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估計與預測:依解法分類,2022-2035年

- 遠程操作車輛(ROV)

- 探測車/太空船著陸器

- 太空探勘

- 其他

- 遠端控制系統(RMS)

- 機械臂/機械手臂系統

- 抓取和對接系統

- 其他

- 軟體

- 服務

第6章 市場估計與預測:依技術分類,2022-2035年

- 遙感探測

- 自主系統

- 遙控

- 機器人軟體

- 人工智慧(AI)和機器學習(ML)

- 人機交互

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 深空

- 行星探勘

- 小行星採礦

- 太空探索

- 近太空

- 衛星運行

- 太空站的維護

- 軌道運輸

- 其他

- 地面以上

- 發射操作

- 地面管制操作

- 空間研究設施

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 商業的

- 政府

- 防禦

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界公司

- Airbus SE

- ITT Corporation

- Lockheed Martin Corporation

- MAXAR TECHNOLOGIES

- MDA Space

- Northrop Grumman

- SpaceX

- 本地球員

- Altius Space Machine

- Astrobotic Technology

- Astroscale Holdings Inc.

- Honeybee Robotics

- Intuitive Machines, LLC.

- Ispace

- Made In Space Inc.(Redwire LLC)

- Metecs, LLC.

- Oceaneering International, Inc.

- 區域/利基公司

- BluHaptics, Inc.

- Motiv Space Systems, Inc.

- Olis Robotics

The Global Space Robotics Market was valued at USD 5.4 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 12.4 billion by 2035.

The sector is expanding as the complexity and scope of space missions grow, creating demand for advanced robotic and automation technologies that can operate across diverse extraterrestrial environments. Space agencies and commercial enterprises are developing robotic systems to support long-duration missions in deep space, reduce reliance on astronauts, and enhance operational efficiency. These systems are being designed for multiple applications, including in-space servicing, assembly, and planetary exploration, enabling more frequent, complex, and cost-effective missions. Integration of robotics into space programs allows for real-time monitoring, automated task execution, and mission support that would otherwise strain human resources. Governments, research institutions, and private players are collectively driving innovation, ensuring that robotics plays a pivotal role in the future of space operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.4 Billion |

| Forecast Value | $12.4 Billion |

| CAGR | 8.6% |

The remotely operated vehicles (ROV) segment reached USD 2 billion in 2025, owing to their critical role in space exploration, orbital inspections, planetary rovers, and space station operations. ROVs act as versatile platforms capable of performing remote tasks in hazardous or inaccessible environments, supporting surface exploration, sample collection, and in-orbit maintenance with both real-time control and autonomous capabilities.

The commercial segment reached USD 2.3 billion in 2025, driven by the rapid expansion of private space companies engaged in satellite deployment, space tourism, in-orbit manufacturing, and commercial stations. Commercial space robotics is extensively applied for satellite management, launch operations, inspection, and maintenance, allowing scalable and cost-efficient operations. Strong private investments, increasing launch cadence, and technological innovation further accelerate adoption across commercial missions.

North America Space Robotics Market held a 38.5% share in 2025. The region's growth is fueled by substantial government funding, robust space exploration programs, defense initiatives, and investment in space infrastructure. Agencies and enterprises in North America are leveraging long-term programs to develop advanced robotic platforms, strengthening the region's leadership in space robotics technologies.

Key players operating in the Global Space Robotics Market include Lockheed Martin Corporation, Honeybee Robotics, Astroscale Holdings Inc., Northrop Grumman, Astrobotic Technology, Intuitive Machines LLC, Made In Space Inc. (Redwire LLC), SpaceX, MAXAR TECHNOLOGIES, Airbus SE, Oceaneering International Inc., MDA Space, Altius Space Machine, ITT Corporation, Motiv Space Systems Inc., Olis Robotics, BluHaptics Inc., Ispace, and Metecs LLC. Companies in the Global Space Robotics Market are adopting several strategies to solidify their market presence and expand their global footprint. Leading players are investing in research and development to design autonomous and semi-autonomous robotic systems for deep-space exploration, orbital servicing, and planetary operations. Strategic collaborations with space agencies, commercial launch providers, and satellite operators enable deployment at scale. Firms are also focusing on modular, reconfigurable robotic platforms to support multiple mission profiles and reduce operational costs. Technological innovation in AI, machine learning, sensors, and teleoperation is a priority to enhance precision, reliability, and safety.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.8 Mathematical impact of growth parameters on forecast

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Solution trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End User trends

- 2.3 TAM analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of Satellite Constellations and Deep-Space Missions

- 3.2.1.2 Rising Demand for Autonomous and AI-Enabled Space Operations

- 3.2.1.3 Growth in Space Tourism and Commercial Space Activities

- 3.2.1.4 Increasing Public-Private Sector Collaboration in Space Programs

- 3.2.1.5 Need for In-Orbit Servicing, Debris Removal, and Satellite Maintenance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Development Costs and Technical Complexity

- 3.2.2.2 Operational Risks in Harsh and Unpredictable Space Environments

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of autonomous robotic systems for space missions

- 3.2.3.2 Growing demand for in-orbit servicing, assembly, and manufacturing (ISAM)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Solution, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Remotely Operated Vehicles (ROV)

- 5.2.1 Rovers/Spacecraft Landers

- 5.2.2 Space Probes

- 5.2.3 Others

- 5.3 Remote Manipulator System (RMS)

- 5.3.1 Robotic Arms/Manipulator Systems

- 5.3.2 Gripping & Docking Systems

- 5.3.3 Others

- 5.4 Software

- 5.5 Services

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Remote Sensing

- 6.3 Autonomous Systems

- 6.4 Teleoperation

- 6.5 Robotic Software

- 6.6 Artificial Intelligence (AI) and Machine Learning (ML)

- 6.7 Human-Robot Interaction

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Deep Space

- 7.2.1 Planetary Exploration

- 7.2.2 Asteroid Mining

- 7.2.3 Space Research

- 7.3 Near Space

- 7.3.1 Satellite Operations

- 7.3.2 Space Station Maintenance

- 7.3.3 Orbital Transportation

- 7.3.4 Others

- 7.4 Ground

- 7.4.1 Launch Operations

- 7.4.2 Ground Control Operations

- 7.4.3 Space Research Labs

Chapter 8 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government

- 8.4 Defence

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Airbus SE

- 10.1.2 ITT Corporation

- 10.1.3 Lockheed Martin Corporation

- 10.1.4 MAXAR TECHNOLOGIES

- 10.1.5 MDA Space

- 10.1.6 Northrop Grumman

- 10.1.7 SpaceX

- 10.2 Regional Players

- 10.2.1 Altius Space Machine

- 10.2.2 Astrobotic Technology

- 10.2.3 Astroscale Holdings Inc.

- 10.2.4 Honeybee Robotics

- 10.2.5 Intuitive Machines, LLC.

- 10.2.6 Ispace

- 10.2.7 Made In Space Inc. (Redwire LLC)

- 10.2.8 Metecs, LLC.

- 10.2.9 Oceaneering International, Inc.

- 10.3 Local / Niche Players

- 10.3.1 BluHaptics, Inc.

- 10.3.2 Motiv Space Systems, Inc.

- 10.3.3 Olis Robotics