|

市場調查報告書

商品編碼

1982352

食品加工機市場機會、成長要素、產業趨勢分析及2026-2035年預測Food Processor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

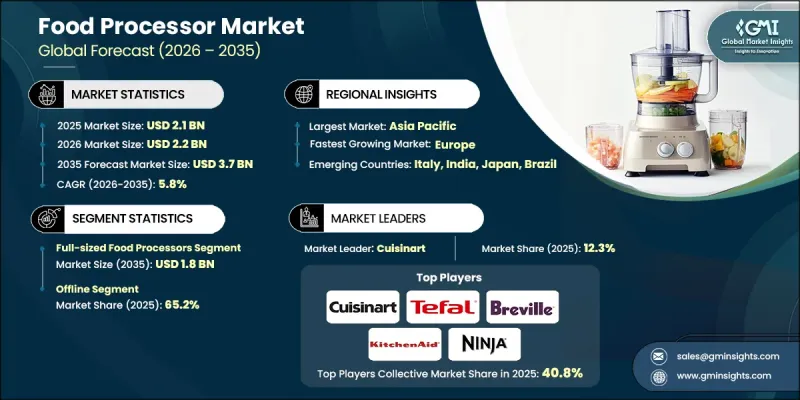

全球食品加工設備市場預計到 2025 年將價值 21 億美元,預計到 2035 年將以 5.8% 的複合年成長率成長至 37 億美元。

全球食品加工機市場的成長主要受消費者對高效能廚房電器日益成長的需求所驅動,這些電器能夠滿足現代烹飪習慣的需求。食物處理機用途廣泛,可用於切碎、切片、攪拌、研磨、揉麵和混合等多種功能,是時間緊迫的家庭的必備工具。人們對均衡飲食和健康飲食習慣的日益重視,以及公共部門推廣營養改善的舉措,進一步推動了市場需求。消費者希望找到既能簡化備餐流程又能確保食物品質和口感的電器。為此,製造商紛紛推出技術先進的產品,這些產品具備智慧連接、多功能性和增強的安全性能。預製食品和易烹飪食品的日益普及也推動了對可靠食品加工機的需求。隨著生活節奏加快和城市人口成長,消費者越來越傾向於選擇兼具便利性、高性能和耐用性的電器。持續的產品創新和不斷變化的消費者偏好正在塑造全球食品加工機市場的競爭格局。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 21億美元 |

| 預測金額 | 37億美元 |

| 複合年成長率 | 5.8% |

千禧世代和職場人士對能夠簡化備餐流程、提高效率的多功能廚房電器表現出濃厚的興趣。便利性仍然是重要的購買因素,尤其對於希望縮短烹飪時間的都市區而言更是如此。快速的城市發展、有利的政策環境以及飲食習慣的改變,都推動了食品加工產業的持續成長。在不斷成長的需求推動下,製造商持續推出符合現代烹飪趨勢和節省空間廚房設計的新型號產品。

預計到2025年,全尺寸食物料理機市場規模將達10億美元,2035年將達到18億美元。全尺寸機型之所以能推動這一品類的發展,是因為它們能夠處理大量食材,並且功能多樣,既適合家庭使用,也適合商用。這些產品通常具有多種速度設定、高處理能力和先進功能,以滿足不同的烹飪需求。人們對永續性和節能家電日益成長的興趣也影響著該領域的產品開發策略。

預計到2025年,線下通路將佔據65.2%的市佔率。實體店仍然發揮著至關重要的作用,因為消費者可以在購買前直接評估產品。商店展示、銷售人員的個人化服務以及產品對比的機會都能增強消費者的信心。這種購買行為在發展中地區尤其突出,因為那裡的消費者重視親身觸摸和評估產品。政府主導的旨在促進透過本地零售網路購物的措施也推動了線下銷售的成長。為此,一些知名品牌正在拓展其實體店網路,以增強市場滲透率。

預計到2025年,美國食品加工機市佔率將達到73.9%。北美食品加工機市場受益於家庭烹飪和餐食準備趨勢的日益成長。完善的零售基礎設施、穩定的進口量以及持續的國內生產為產品供應和消費者獲取提供了保障。聯邦貿易數據顯示,小型廚房電器的出貨量和進口量持續成長,顯示全部區域需求強勁。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 人們對烹飪便利性的需求日益成長。

- 人們越來越關注健康和保健

- 技術進步與產品創新

- 產業潛在風險與挑戰

- 競爭加劇和產品商品化

- 消費者轉向一體化智慧廚房系統

- 機會

- 消費者對以便捷性為首要考慮因素的家庭烹飪解決方案的需求日益成長。

- 智慧連網廚房電器的發展

- 促進因素

- 成長潛力分析

- 監理情勢

- 關鍵市場趨勢與顛覆性因素

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 2025年價格分析

- 按地區

- 按類型

- 未來市場趨勢

- 貿易統計

- 主要進口國

- 主要出口國

- 波特的分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 偏好分析

- 不同地區的消費行為差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 大型食品加工機

- 迷你食物處理器

- 手動食物處理器

第6章 市場估計與預測:依投資類型分類,2022-2035年

- 手動的

- 電的

第7章 市場估計與預測:依產能分類,2022-2035年

- 少於2公升

- 2-5升

- 超過5公升

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅

- 商業的

第9章 市場估計與預測:依價格分類,2022-2035年

- 低價位

- 中號

- 高價位範圍

第10章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 超級市場/大賣場

- 專賣店

- 其他(個體店、百貨公司等)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- Black+Decker

- Bosch

- Braun

- Breville

- Cuisinart

- Hamilton Beach

- Kenwood

- KitchenAid

- Magimix

- Moulinex

- Ninja

- Oster

- Panasonic

- Philips

- Tefal

The Global Food Processor Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 3.7 billion by 2035.

Growth in the global food processor market is being driven by increasing demand for efficient kitchen appliances that support modern cooking habits. Food processors are widely used for chopping, slicing, blending, grinding, kneading, and mixing, making them essential tools for time-conscious households. Rising awareness of balanced diets and healthier eating patterns, supported by public initiatives promoting improved nutrition, is further strengthening market demand. Consumers are seeking appliances that simplify meal preparation while maintaining quality and consistency. In response, manufacturers are introducing technologically advanced models featuring smart connectivity, multifunctional capabilities, and enhanced safety features. The growing popularity of partially prepared and easy-to-cook food products is also reinforcing the need for reliable food processing solutions. As lifestyles become busier and urban populations expand, consumers increasingly prefer appliances that combine convenience, performance, and durability. Continuous product innovation and evolving consumer preferences are shaping the competitive dynamics of the food processor market worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.7 Billion |

| CAGR | 5.8% |

Millennials and working professionals are showing strong interest in multifunctional kitchen appliances that streamline meal preparation and maximize efficiency. Convenience remains a primary purchasing factor, particularly among urban households seeking to reduce preparation time. Rapid urban development, supportive policy frameworks, and shifting dietary habits are contributing to sustained expansion in the food processor industry. As demand rises, manufacturers continue to launch new models designed to align with contemporary culinary trends and space-conscious kitchen designs.

The full-sized food processors segment generated USD 1 billion in 2025 and is forecast to reach USD 1.8 billion by 2035. Full-sized units dominate this category due to their ability to handle larger food volumes and deliver versatile performance suitable for both household and professional use. These appliances typically offer multiple speed settings, larger processing capacities, and enhanced functionality to support diverse cooking needs. Growing emphasis on sustainability and energy-efficient appliances is also influencing product development strategies within this segment.

The offline distribution channels segment accounted for 65.2% share in 2025. Physical retail outlets remain significant because they allow consumers to evaluate products directly before purchasing. In-store demonstrations, personal assistance from sales representatives, and the opportunity to compare models contribute to stronger buyer confidence. This purchasing behavior is particularly relevant in developing regions where consumers value hands-on product assessment. Government-backed initiatives that encourage shopping through local retail networks have also supported offline sales growth. In response, several leading brands are expanding their brick-and-mortar presence to strengthen market penetration.

U.S. Food Processor Market held 73.9% share in 2025. The North American food processor market is benefiting from increased home cooking activity and meal preparation trends. Strong retail infrastructure, steady import volumes, and consistent domestic manufacturing output are supporting product availability and consumer access. Trade data from federal sources indicates ongoing growth in small kitchen appliance shipments and imports, underscoring resilient demand across the region.

Key companies operating in the Global Food Processor Market include KitchenAid, Braun, Philips, Black + Decker, Kenwood, Panasonic, Moulinex, Breville, Oster, Magimix, Tefal, Hamilton Beach, Cuisinart, Bosch, and Ninja. Companies in the Food Processor Market are reinforcing their competitive position through innovation, portfolio expansion, and strategic distribution enhancements. Manufacturers are investing heavily in research and development to introduce multifunctional, energy-efficient, and smart-enabled appliances that address evolving consumer preferences. Many brands are focusing on product differentiation through advanced motor technologies, improved durability, and compact designs suited for modern kitchens. Strategic collaborations with retail chains and e-commerce platforms are strengthening omnichannel presence and improving customer reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.3.1 Source consistency protocol

- 1.4 Research Trail & Confidence Scoring

- 1.4.1 Research Trail Components

- 1.4.2 Scoring Components

- 1.5 Data Collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.7 Paid sources

- 1.7.1 Sources, by region

- 1.8 Base estimates and calculations

- 1.8.1 Base year calculation for any one approach

- 1.9 Forecast model

- 1.9.1 Quantified market impact analysis

- 1.9.1.1 Mathematical impact of growth parameters on forecast

- 1.9.1 Quantified market impact analysis

- 1.10 Research transparency addendum

- 1.10.1 Source attribution framework

- 1.10.2 Quality assurance metrics

- 1.10.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Mode of Operation

- 2.2.4 Capacity

- 2.2.5 Application

- 2.2.6 Price

- 2.2.7 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for convenience in food preparation

- 3.2.1.2 Increasing health and wellness awareness

- 3.2.1.3 Technological advancements and product innovation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Rising competition & product commoditization

- 3.2.2.2 Consumer shift toward all in one smart kitchen systems

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for convenience driven home cooking solutions

- 3.2.3.2 Growth of smart, connected kitchen appliances

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Major market trends and disruptions

- 3.6 Technological and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Pricing analysis, 2025

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Trade statistics

- 3.9.1 Major importing countries

- 3.9.2 Major exporting countries

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behaviour analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behaviour

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Full-sized food processors

- 5.3 Mini food processors

- 5.4 Hand-operated food processors

Chapter 6 Market Estimates & Forecast, By Mode of Operation, 2022-2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Electric

Chapter 7 Market Estimates & Forecast, By Capacity, 2022-2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Up to 2 liters

- 7.3 2-5 liters

- 7.4 Above 5 liters

Chapter 8 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Price, 2022-2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-Commerce

- 10.2.2 Company website

- 10.3 Offline

- 10.3.1 Supermarkets/Hypermarkets

- 10.3.2 Specialty Stores

- 10.3.3 Others (Individual stores, Departmental stores, etc.)

Chapter 11 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 France

- 11.3.3 UK

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Black+Decker

- 12.2 Bosch

- 12.3 Braun

- 12.4 Breville

- 12.5 Cuisinart

- 12.6 Hamilton Beach

- 12.7 Kenwood

- 12.8 KitchenAid

- 12.9 Magimix

- 12.10 Moulinex

- 12.11 Ninja

- 12.12 Oster

- 12.13 Panasonic

- 12.14 Philips

- 12.15 Tefal

工業食品加工機械市場規模、佔有率及成長分析(依設備類型、操作方式、應用及地區分類)-2026-2033年產業預測

工業食品加工機械市場規模、佔有率及成長分析(依設備類型、操作方式、應用及地區分類)-2026-2033年產業預測 蔬果切片機的全球市場規模:各產品,各用途,各地區,範圍及預測

蔬果切片機的全球市場規模:各產品,各用途,各地區,範圍及預測 工業食品加工機市場、機會、成長動力、產業趨勢分析與預測,2024-2032

工業食品加工機市場、機會、成長動力、產業趨勢分析與預測,2024-2032