|

市場調查報告書

商品編碼

1982344

洗面乳市場:商機、成長要素、產業趨勢分析及2026-2035年預測Facial Cleanser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

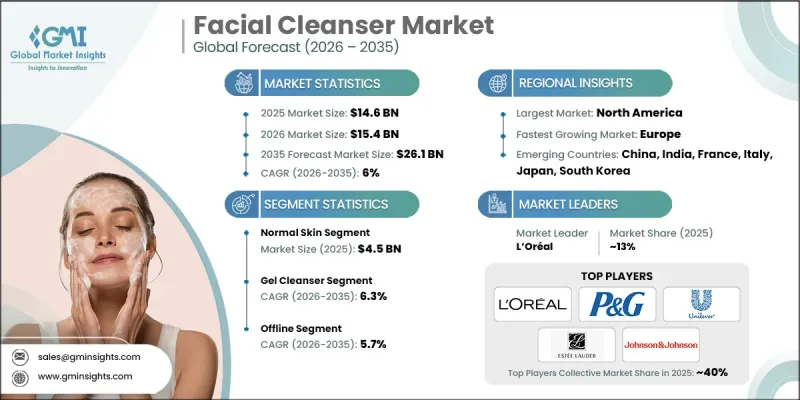

預計到 2025 年,全球洗面乳市場價值將達到 146 億美元,並有望以 6% 的複合年成長率成長,到 2035 年達到 261 億美元。

消費者對日常護膚程序的日益重視推動了洗面乳的需求成長。越來越多的人認知到保持健康亮麗肌膚的重要性。隨著都市區污染的加劇以及人們對整裝儀容的日益關注,消費者開始購買那些承諾有效清潔且不損害皮膚健康的專業產品。社群媒體和美妝內容的普及使人們更容易了解護膚方法,從而提升了對高階洗面乳的需求。年輕消費者尤其容易受到美妝潮流的影響,而男性也擴大將洗面乳納入日常整裝儀容程序。電商平台和線上美妝零售商的蓬勃發展也促進了銷售成長,使消費者能夠輕鬆購買到種類繁多的產品。

| 市場規模 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 146億美元 |

| 預計金額 | 261億美元 |

| 複合年成長率 | 6% |

預計到2025年,中性肌膚市場規模將達到45億美元,並在2026年至2035年間以6.3%的複合年成長率成長。中性肌膚市場佔據主導地位,因為許多消費者偏好溫和配方,既能清潔肌膚,又不會帶走肌膚的天然水分。各年齡層消費者堅持每日使用,加上高階和大眾市場產品線的廣泛覆蓋,確保了銷售額的穩定成長。

預計到2025年,線下零售通路將佔據74.96%的市場佔有率,並在2026年至2035年間以5.7%的複合年成長率成長。實體店憑藉其即時的購物體驗、清晰的產品展示以及影響購買決策的店內促銷活動,在洗面乳銷售中繼續發揮著核心作用。消費者可以在超級市場、藥妝店和專賣店輕鬆找到產品,並在購買前查看包裝、品質和品牌信譽。

美國洗面乳市場預計到2025年將達到37億美元,並在2026年至2035年間以5.9%的複合年成長率成長。個人照護支出的增加以及社群媒體上日益成長的關注度,正促使消費者選擇適合自身膚質和肌膚問題的洗面乳。男士護理的日益普及以及皮膚科醫生的建議,推動了對經臨床驗證、能夠滿足特定需求的洗面乳的需求。訂閱服務也促進了消費者的重複購買和持續使用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 消費者對護膚和整裝儀容的興趣日益濃厚

- 影響者主導的數位美妝內容成長

- 電子商務和線上美妝零售的擴張

- 陷阱與挑戰

- 激烈的競爭壓力和品牌數量的激增

- 對化妝品成分的監管限制

- 機會

- 個性化和人工智慧驅動的護膚建議

- 清潔、永續、可重複填充包裝的創新。

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特的分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依膚質分類,2022-2035年

- 正常皮膚

- 油性肌膚

- 乾性皮膚

- 敏感肌膚

- 混合性肌膚

- 其他

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 凝膠潔面乳

- 乳霜/乳液型洗面乳

- 泡沫洗面乳

- 固態

- 其他

第7章 市場估計與預測:依消費群組分類,2022-2035年

- 男性

- 女士

- 男女通用的

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 個人

- 商業的

第9章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務網站

- 企業網站

- 離線

- 大賣場/超級市場

- 百貨公司

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第11章:公司簡介

- Amorepacific Corporation

- Beiersdorf AG

- Clarins Group

- Coty Inc.

- Estee Lauder

- Johnson &Johnson

- Kao Corporation

- L'Oreal

- Mary Kay Inc.

- Natura &Co

- Pierre Fabre Group

- Procter &Gamble

- Revlon, Inc.

- Shiseido Company

- Unilever

The Global Facial Cleanser Market was valued at USD 14.6 billion in 2025 and is estimated to grow at a CAGR of 6% to reach USD 26.1 billion by 2035.

Consumer awareness about daily skincare routines is driving demand for facial cleansers, as more people recognize the importance of maintaining healthy, clear skin. With increased exposure to urban pollutants and the rising emphasis on personal grooming, consumers are purchasing specialized products that promise effective cleansing without compromising skin health. Social media and beauty content have made it easier for individuals to understand skincare practices, fueling demand for advanced facial cleansers. Younger consumers are particularly influenced by beauty trends, while men are increasingly adopting facial cleansers as part of their daily grooming habits. The growth of e-commerce platforms and online beauty retailing also supports higher sales, offering consumers convenient access to a wide range of products.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.6 Billion |

| Forecast Value | $26.1 Billion |

| CAGR | 6% |

In 2025, the normal skin segment accounted for USD 4.5 billion and is expected to grow at a CAGR of 6.3% between 2026 and 2035. Normal skin dominates the market as a large portion of consumers prefer mild formulations that cleanse without disturbing natural moisture. Consistent daily use across all age groups, along with widespread product availability in both premium and mass-market categories, ensures steady sales growth.

The offline retail channels segment held 74.96% share in 2025 and is projected to grow at a CAGR of 5.7% from 2026 to 2035. Brick-and-mortar stores remain central to facial cleanser sales, as they offer immediate access, product visibility, and in-store promotions that influence buying decisions. The accessibility of products in supermarkets, pharmacies, and specialty stores allows consumers to evaluate packaging, quality, and brand trust before purchasing.

U.S. Facial Cleanser Market reached USD 3.7 billion in 2025 and is projected to grow at a CAGR of 5.9% from 2026 to 2035. Rising personal care spending and social media awareness encourage consumers to select cleansers suited to their skin types and concerns. Increasing interest in men's grooming and professional dermatology endorsements boosts demand for targeted and clinically recommended facial cleansing products. Subscription-based services also drive repeat purchases and consistent product usage.

Major players in the Global Facial Cleanser Market include Beiersdorf AG, Shiseido Company, L'Oreal, Clarins Group, Coty Inc., Procter & Gamble, Johnson & Johnson, Mary Kay Inc., Unilever, Amorepacific Corporation, Natura &Co, Estee Lauder, Revlon, Inc., Pierre Fabre Group, and Kao Corporation. Leading companies are adopting multiple strategies to strengthen their market presence. They are investing in research and development to launch innovative and skin-specific products, expanding online and offline distribution networks, and collaborating with dermatologists to enhance credibility. Many brands focus on influencer partnerships and social media campaigns to connect with younger consumers, while premium and subscription offerings encourage repeat purchases. Aggressive promotional activities, brand loyalty programs, and global market expansion remain key tactics to maintain competitive positioning and capture a larger share of the growing facial cleanser market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Skin Type

- 2.2.2 Product Type

- 2.2.3 Consumer Group

- 2.2.4 End User

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing consumer focus on skincare and personal grooming

- 3.2.1.2 Growth in influencer-led and digital beauty content

- 3.2.1.3 Expansion of e-commerce and online beauty retailing

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Intense competitive pressure and brand proliferation

- 3.2.2.2 Regulatory constraints on cosmetic ingredients

- 3.2.3 Opportunities

- 3.2.3.1 Customization and AI-driven skincare recommendations

- 3.2.3.2 Clean, sustainable and refillable packaging innovations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Skin Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Normal Skin

- 5.3 Oily skin

- 5.4 Dry skin

- 5.5 Sensitive skin

- 5.6 Combination skin

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Gel cleanser

- 6.3 Cream & lotion cleanser

- 6.4 Foaming cleanser

- 6.5 Bar cleanser

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Consumer Group, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Male

- 7.3 Female

- 7.4 Unisex

Chapter 8 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Individual

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce websites

- 9.2.2 Company websites

- 9.3 Offline

- 9.3.1 Hypermarket/supermarket

- 9.3.2 Departmental stores

- 9.3.3 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Amorepacific Corporation

- 11.2 Beiersdorf AG

- 11.3 Clarins Group

- 11.4 Coty Inc.

- 11.5 Estee Lauder

- 11.6 Johnson & Johnson

- 11.7 Kao Corporation

- 11.8 L’Oreal

- 11.9 Mary Kay Inc.

- 11.10 Natura &Co

- 11.11 Pierre Fabre Group

- 11.12 Procter & Gamble

- 11.13 Revlon, Inc.

- 11.14 Shiseido Company

- 11.15 Unilever

洗面乳和化妝水市場報告:趨勢、預測和競爭分析(至2035年)

洗面乳和化妝水市場報告:趨勢、預測和競爭分析(至2035年) 洗面乳市場規模、佔有率和成長分析:依產品類型、價格範圍、應用、最終用戶、銷售管道和地區分類-2026-2033年產業預測

洗面乳市場規模、佔有率和成長分析:依產品類型、價格範圍、應用、最終用戶、銷售管道和地區分類-2026-2033年產業預測 洗面乳市場:2026-2032年全球預測,依年齡層、性別、膚質、產品類型、配方及分銷管道分類

洗面乳市場:2026-2032年全球預測,依年齡層、性別、膚質、產品類型、配方及分銷管道分類 全球洗面乳及潔面產品市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球洗面乳市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球洗面乳及潔面產品市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球洗面乳市場規模、佔有率、趨勢及成長分析報告(2026-2034年) 洗面乳市場-全球產業規模、佔有率、趨勢、機會、預測:按形狀、應用、銷售管道、地區和競爭格局分類,2021-2031年活性碳面部護理產品市場-全球產業規模、佔有率、趨勢、機會及預測(按產品類型、性別、分銷管道、地區和競爭格局分類,2021-2031年)

洗面乳市場-全球產業規模、佔有率、趨勢、機會、預測:按形狀、應用、銷售管道、地區和競爭格局分類,2021-2031年活性碳面部護理產品市場-全球產業規模、佔有率、趨勢、機會及預測(按產品類型、性別、分銷管道、地區和競爭格局分類,2021-2031年) 全球洗面乳和清潔產品市場全球臉部磨砂膏市場全球洗面乳市場

全球洗面乳和清潔產品市場全球臉部磨砂膏市場全球洗面乳市場