|

市場調查報告書

商品編碼

1982334

文字轉語音市場機會、成長要素、產業趨勢分析及2026-2035年預測Text to Speech (TTS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

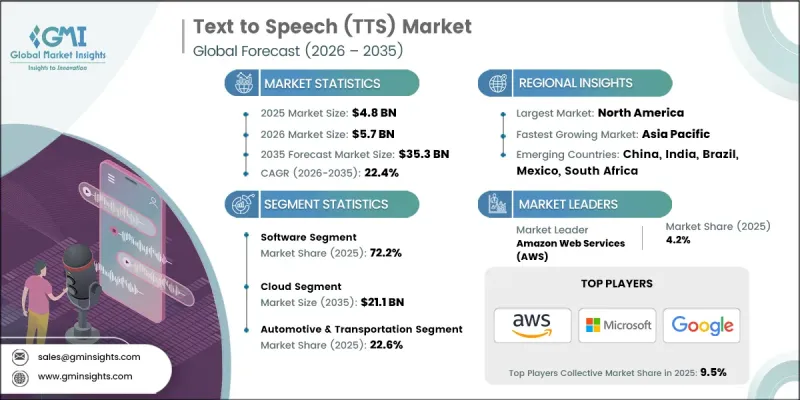

2025 年全球文字轉語音 (TTS) 市場價值為 48 億美元,預計到 2035 年將達到 353 億美元,年複合成長率為 22.4%。

市場擴張的驅動力在於人們對更自然、更接近人聲的合成語音的需求日益成長,而人工智慧 (AI) 和自然語言處理 (NLP) 技術的進步則進一步推動了這一需求。這些技術使文字轉語音 (TTS) 平台能夠更準確地解讀文字內容,並產生高度逼真的語音輸出。此外,人們越來越關注無障礙、包容性和輔助技術,以滿足視障人士、學習障礙人士或偏好聽覺學習人士的需求,這也促進了 TTS 解決方案的普及。將 TTS 整合到數位內容和應用程式中,既能提高資訊的可近性,又能幫助企業遵守無障礙標準。然而,該市場也面臨著許多挑戰,例如倫理問題以及合成語音被濫用於詐騙、深度造假或傳播虛假訊息,這些都可能威脅到數位通訊中的隱私、聲譽和信任。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 48億美元 |

| 預測金額 | 353億美元 |

| 複合年成長率 | 22.4% |

預計2026年至2035年間,服務領域的複合年成長率將達到24%。服務提供者提供諮詢、實施、客製化和持續支持,使企業能夠有效部署TTS解決方案,同時專注於核心業務營運。包括語音個人化、語音微調和維護在內的託管TTS服務需求日益成長,旨在提升效能和使用者體驗。

混合型文字轉語音(TTS)市場預計在2025年達到5.713億美元,並在2026年至2035年間以22.7%的複合年成長率成長。混合型TTS透過結合裝置內處理和雲端功能,平衡了延遲、隱私和整體效能。這種方法在行動裝置、穿戴式科技和汽車應用領域正日益普及,在這些應用中,離線功能可以與基於雲端的更新和增強功能形成互補。

預計到2025年,北美文字轉語音(TTS)市佔率將達到38.1%。這一區域成長主要得益於嚴格的數位無障礙法規以及政府、教育和企業部門對輔助科技的廣泛應用。各組織正在加速更新其數位平台以符合無障礙標準,這推動了TTS在多個行業和應用場景中的整合。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 人工智慧和自然語言處理技術的進步將實現聽起來自然的口語

- 擴大文字轉語音技術在無障礙和包容性數位體驗中的應用

- 視覺障礙者和老年人對輔助科技的需求日益成長。

- TTS技術與客戶支援和IVR系統的整合正在穩步推進。

- 對多語言和區域語言支援的需求

- 產業潛在風險與挑戰

- 高昂的實施和整合成本

- 倫理考量與濫用

- 市場機遇

- 進入識字率較低的新興市場

- 在醫療保健領域實施,以病人參與和遠端監測

- 促進因素

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域部署對比

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 財務績效比較

- 2022-2025 年重大發展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 軟體

- 服務

- SaaS 和支持

- 實施與諮詢

第6章 市場估算與預測:依語音技術分類,2022-2035年

- 神經

- 非神經系統

第7章 市場估算與預測、實施模型(2022-2035年)

- 雲

- 現場

- 混合

第8章 市場估計與預測:依語言分類,2022-2035年

- 英語

- 印地語

- 中文(國語)

- 西班牙語

- 拉丁美洲

- 阿拉伯

- 其他

第9章 市場估計與預測:依最終用途產業分類,2022-2035年

- 教育和數位學習

- BFSI

- 資訊科技/通訊

- 家用電子電器

- 汽車和交通運輸

- 衛生保健

- 媒體與娛樂

- 零售與電子商務

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 主要企業

- Amazon.com Inc.

- Google Inc.

- Microsoft Corporation

- IBM Corporation

- Nuance Communication

- 按地區分類的主要企業

- Baidu Inc.

- iFLYTEK Co., Ltd

- LumenVox LLC

- Readspeaker

- VONAGE AMERICA, LLC

- 特殊玩家/干擾者

- CEREPROC LTD.

- DEEPBRAIN AI

- ElevenLabs

- Lovo

- MURF.AI

- SESTEK

- SYNTHESIA LIMITED

- TextSpeak

The Global Text to Speech (TTS) Market was valued at USD 4.8 billion in 2025 and is estimated to grow at a CAGR of 22.4% to reach USD 35.3 billion by 2035.

The market expansion is driven by rising demand for more natural, human-like synthesized voices, powered by advancements in artificial intelligence (AI) and natural language processing (NLP). These technologies enable TTS platforms to better interpret written content and generate highly realistic speech outputs. The adoption of TTS solutions is also fueled by the growing emphasis on accessibility, inclusivity, and assistive technologies, catering to individuals with visual impairments, learning disabilities, or those who prefer auditory learning. The integration of TTS into digital content and applications enhances information accessibility while enabling organizations to comply with accessibility standards. However, the market faces challenges, including ethical concerns and the potential misuse of synthetic voices for fraudulent activities, deep fakes, or misinformation, which can threaten privacy, reputations, and trust in digital communications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.8 Billion |

| Forecast Value | $35.3 Billion |

| CAGR | 22.4% |

The services segment is expected to grow at a CAGR of 24% from 2026 to 2035. Providers offer consulting, implementation, customization, and ongoing support, allowing businesses to deploy TTS solutions effectively while focusing on core operations. Managed TTS services, including voice personalization, speech fine-tuning, and maintenance, are increasingly sought after to enhance performance and user experience.

The hybrid segment reached USD 571.3 million in 2025 and is projected to grow at a CAGR of 22.7% during 2026-2035. Hybrid TTS combines on-device processing with cloud capabilities, balancing latency, privacy, and overall performance. This approach is gaining traction in mobile devices, wearable technologies, and automotive applications, where offline functionality complements cloud-based updates and improvements.

North America Text to Speech (TTS) Market held 38.1% share in 2025. Growth in this region is supported by stringent digital accessibility regulations and widespread adoption of assistive technologies across government, education, and corporate sectors. Organizations are increasingly updating digital platforms to comply with accessibility standards, driving TTS integration across multiple industries and use cases.

Key companies operating in the Global Text to Speech (TTS) Market include Google Inc., IBM Corporation, Amazon.com Inc., DEEPBRAIN AI, ElevenLabs, iFLYTEK Co., Ltd, Baidu Inc., and CEREPROC LTD. Companies in the Global Text to Speech (TTS) Market are focusing on strategic partnerships, technological innovation, and geographic expansion to strengthen their market presence. Providers are investing in AI-driven voice synthesis, multilingual capabilities, and personalized voice development. Collaborations with educational, corporate, and government sectors expand deployment opportunities. Companies are also enhancing cloud and hybrid offerings to provide low-latency, secure, and scalable solutions. Expanding distribution networks, improving developer tools, and offering managed services further consolidate their market position while ensuring consistent customer engagement and long-term growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Offering trends

- 2.2.2 Voice technology trends

- 2.2.3 Deployment model trends

- 2.2.4 Language trends

- 2.2.5 End-use industry trends

- 2.2.6 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in AI and NLP for natural-sounding speech

- 3.2.1.2 Increasing adoption of TTS for accessibility and inclusive digital experiences

- 3.2.1.3 Growing demand for assistive technologies for visually impaired and elderly

- 3.2.1.4 Rising integration of TTS in customer support and IVR systems

- 3.2.1.5 Demand for multilingual and regional language support

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and integration costs

- 3.2.2.2 Ethical considerations and misuse

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with low literacy rates

- 3.2.3.2 Adoption in healthcare for patient engagement and remote monitoring

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Offering, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

- 5.3.1 Software-as-a-service and support

- 5.3.2 Implementation & consulting

Chapter 6 Market Estimates and Forecast, By Voice Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Neural

- 6.3 Non-Neural

Chapter 7 Market Estimates and Forecast, Deployment Model, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 On-premises

- 7.4 Hybrid

Chapter 8 Market Estimates and Forecast, By Language, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 English

- 8.3 Hindi

- 8.4 Mandarin chinese

- 8.5 Spanish

- 8.6 Latin

- 8.7 Arabic

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Education & E-learning

- 9.3 BFSI

- 9.4 IT & telecom

- 9.5 Consumer electronics

- 9.6 Automotive & transportation

- 9.7 Healthcare

- 9.8 Media & entertainment

- 9.9 Retail & E-commerce

- 9.10 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Amazon.com Inc.

- 11.1.2 Google Inc.

- 11.1.3 Microsoft Corporation

- 11.1.4 IBM Corporation

- 11.1.5 Nuance Communication

- 11.2 Regional Key Players

- 11.2.1 Baidu Inc.

- 11.2.2 iFLYTEK Co., Ltd

- 11.2.3 LumenVox LLC

- 11.2.4 Readspeaker

- 11.2.5 VONAGE AMERICA, LLC

- 11.3 Niche Players / Disruptors

- 11.3.1 CEREPROC LTD.

- 11.3.2 DEEPBRAIN AI

- 11.3.3 ElevenLabs

- 11.3.4 Lovo

- 11.3.5 MURF.AI

- 11.3.6 SESTEK

- 11.3.7 SYNTHESIA LIMITED

- 11.3.8 TextSpeak

文字轉語音市場:按組件、型號、設備類型、定價模式、支援語言、應用、最終用戶、最終用戶產業和部署模式分類-2026-2032年全球市場預測

文字轉語音市場:按組件、型號、設備類型、定價模式、支援語言、應用、最終用戶、最終用戶產業和部署模式分類-2026-2032年全球市場預測 2026年全球文字轉語音市場報告2026年全球文字轉語音(TTS)軟體市場報告

2026年全球文字轉語音市場報告2026年全球文字轉語音(TTS)軟體市場報告 2025-2029年全球TTS(文字轉語音)市場

2025-2029年全球TTS(文字轉語音)市場 全球文字轉語音 (TTS) 市場規模(按產品、供應、應用、區域覆蓋)預測(至 2025 年)

全球文字轉語音 (TTS) 市場規模(按產品、供應、應用、區域覆蓋)預測(至 2025 年) 全球文字轉語音 (TTS) 市場:市場規模、佔有率、趨勢、產業分析(按產品、部署方法、語音類型、組織規模、語言和地區)、未來預測(2025-2034 年)

全球文字轉語音 (TTS) 市場:市場規模、佔有率、趨勢、產業分析(按產品、部署方法、語音類型、組織規模、語言和地區)、未來預測(2025-2034 年) 全球螢幕閱讀器軟體市場規模研究(按平台、作業系統、應用程式、配銷通路)以及 2022-2032 年區域預測

全球螢幕閱讀器軟體市場規模研究(按平台、作業系統、應用程式、配銷通路)以及 2022-2032 年區域預測