|

市場調查報告書

商品編碼

1982328

汽車彈簧市場機會、成長要素、產業趨勢分析及2026-2035年預測Automotive Spring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

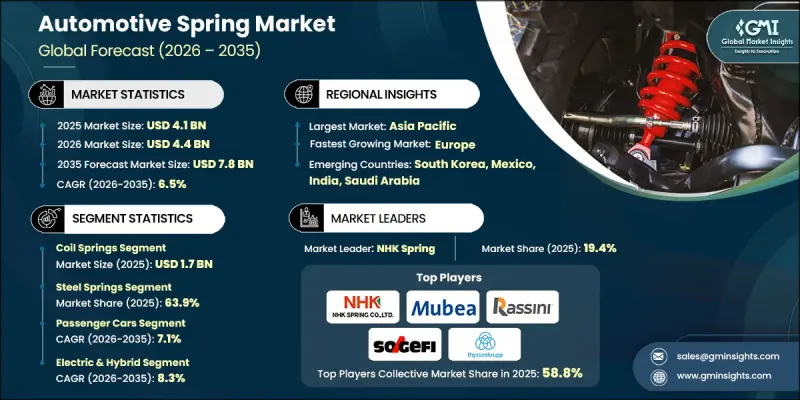

全球汽車彈簧市場預計到 2025 年將價值 41 億美元,預計到 2035 年將以 6.5% 的複合年成長率成長至 78 億美元。

汽車彈簧仍然是乘用車和商用車中支撐負載管理、乘坐舒適性和穩定性的基本結構和懸吊零件。全球汽車產量的穩定成長支撐著彈簧系統的長期需求。在許多經濟體中,可支配收入的增加推動了汽車保有量的上升,進而促進了全球汽車產量的擴張。隨著汽車製造商擴大生產規模以滿足消費者需求,對可靠、高性能彈簧解決方案的需求也持續成長。同時,向電動出行的轉型正在重塑汽車彈簧市場的產品開發策略。製造商優先考慮輕量化技術解決方案,以提高能源效率和續航里程。這種轉變推動了尖端材料和最佳化彈簧設計的應用,以適應不斷發展的汽車架構。此外,亞洲、拉丁美洲以及中東和非洲部分地區新興的汽車製造地為供應商創造了建立本地生產基地並加強與汽車製造商(OEM)長期夥伴關係的機會。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 41億美元 |

| 預測金額 | 78億美元 |

| 複合年成長率 | 6.5% |

預計2026年至2035年間,氣彈簧市場將以8.1%的複合年成長率成長。這些部件正日益被應用於現代車輛系統中,以實現可控運動並提高安全性。它們能夠提供平穩精準的運動,從而提升使用者便利性和運作可靠性。在電動和混合動力汽車中,氣彈簧支撐著需要精確運動控制的特殊結構和內裝部件。隨著全球電動車的普及加速,以應對監管壓力和不斷變化的消費者偏好,先進氣彈簧解決方案的重要性也日益凸顯。

預計到2025年,鋼製彈簧市佔率將達到63.9%,到2035年市場規模將達到48億美元。儘管原料價格波動,但由於鋼材具有優異的強度重量比和耐久性,它仍然是首選材料。在整個預測期內,與複合材料和聚合物基產品等替代品相比,鋼製彈簧預計將繼續廣泛應用。其成本效益、大規模生產能力和穩定的品質標準使其成為OEM生產和售後市場替換需求的可靠選擇。完善的供應鏈網路和具有競爭力的價格進一步鞏固了鋼製彈簧在成熟汽車市場和新興市場的領先地位。

美國汽車彈簧市場預計2025年將達到4.608億美元。美國是一個重要的市場,擁有龐大的汽車製造基地、健全的售後市場生態系統以及乘用車和輕型卡車的強勁產量。持續的汽車生產和老舊車輛帶來的日益成長的更換需求正在推動市場穩步擴張。旨在2030年實現零排放出行的法規結構正在影響懸吊零件的設計要求,迫使製造商開發能夠適應電動車重量分佈和性能特徵的彈簧系統。同時,汽車製造商也面臨著不斷變化的政策環境和日益複雜的供應鏈所帶來的挑戰,這些都影響著籌資策略。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球汽車產量增加

- 商用車需求不斷成長

- 電動車(EV)市場的擴張

- 汽車售後市場需求增加

- 產業潛在風險與挑戰

- 原物料價格波動

- 激烈的競爭和價格壓力

- 市場機遇

- 先進輕質彈簧材料的開發

- 新興汽車市場的成長

- 電動車和混合動力汽車的擴張

- 策略聯盟和OEM夥伴關係

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國國家公路交通安全管理局(NHTSA)

- 加拿大運輸部

- 美國環保署(EPA)

- 加州空氣資源委員會(CARB)

- SAE International

- 歐洲

- 歐盟委員會

- 聯合國歐洲經濟委員會(UNECE)

- 歐洲汽車製造商協會 (ACEA)

- 歐洲標準化委員會(CEN)

- 德國聯邦汽車運輸管理局(KBA)

- 亞太地區

- 中國工業和資訊化部

- 中國汽車技術研究中心(CATARC)

- 印度汽車研究協會(ARAI)

- 韓國交通安全管理局(KOTSA)

- 拉丁美洲

- 國家交通運輸秘書處(SENATRAN)

- INMETRO

- 國土交通省

- 墨西哥國家標準(NOM)

- 中東和非洲

- 波灣合作理事會標準化組織(GSO)

- ESMA(阿拉伯聯合大公國標準化和計量局)

- 沙烏地阿拉伯標準、計量和品質組織(SASO)

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 高強度合金鋼彈簧

- 輕量化複合材料鋼板彈簧

- 將空氣彈簧整合到車輛中

- 新興技術

- 碳纖維增強複合複合材料彈簧

- 奈米塗層可增強疲勞強度和耐腐蝕性

- 當前技術趨勢

- 生產統計

- 生產基地

- 消費中心

- 出口和進口

- 價格趨勢

- 按地區

- 依產品

- 成本細分分析

- 永續性和環境影響

- 環境影響評估

- 社會影響和對當地社區的貢獻

- 公司管治與企業社會責任

- 永續金融與投資趨勢

- 產品生命週期與更換週期分析

- 按彈簧類型和車輛等級分類的平均使用壽命

- 失效模式和常見磨損模式

- 車輛年齡分佈與售後市場需求的相關性

- 車輛電氣化對換車週期的影響

- 季節性需求波動和庫存管理模式

- 車輛電氣化影響分析

- 電動車重量分佈的變化及其對彈簧設計的影響

- 電池組重量補償要求

- 再生煞車對懸吊彈簧規格的影響

- 電動車特有的彈簧耐久性和疲勞性的考量。

- 未來展望與商業機遇

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估價與預測:依產品分類,2022-2035年

- 螺旋彈簧

- 鋼板彈簧

- 扭簧

- 氣彈簧

- 其他

第6章 市場估計與預測:依材料分類,2022-2035年

- 鋼彈簧

- 複合彈簧

- 塑膠彈簧

- 其他

第7章 市場估價與預測:依裝載能力分類,2022-2035年

- 小彈簧

- 中等大小的彈簧

- 大彈簧

第8章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- LCV

- MCV

- 重型車輛(HCV)

- 摩托車

第9章 市場估算與預測:依動力傳動系統,2022-2035年

- 內燃機(ICE)

- 電動車和混合動力汽車

- BEV

- HEV

- PHEV

- FCEV

第10章 市場估價與預測:依最終用途分類,2022-2035年

- 懸吊系統

- 引擎氣門

- 離合器總成

- 動力傳動系統

- 其他

第11章 市場估價與預測:依銷售管道分類,2022-2035年

- OEM

- 售後市場

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 捷克共和國

- 比利時

- 俄羅斯

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 印尼

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- 世界公司

- NHK Spring

- Mubea

- Sogefi

- Rassini

- GKN Automotive

- Mitsubishi Steel

- ZF Friedrichshafen

- Thyssenkrupp

- Lesjofors

- 當地公司

- UNI AUTO

- Kilen Springs

- Olgun Celik

- Clifford Springs

- Soni Auto &Allied Industries

- Emco Industries

- Stanley Spring

- 新興企業

- Hendrickson

- Auto Steels

- Vikrant Auto

- Protopower Springs

The Global Automotive Spring Market was valued at USD 4.1 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 7.8 billion by 2035.

Automotive springs remain a fundamental structural and suspension component across passenger and commercial vehicles, supporting load management, ride comfort, and stability. Steady growth in global vehicle production is sustaining long-term demand for spring systems. Rising vehicle ownership levels, supported by improving disposable incomes in multiple economies, are contributing to higher automobile manufacturing volumes worldwide. As automakers scale production to meet consumer demand, the need for reliable and performance-driven spring solutions continues to increase. In parallel, the transition toward electric mobility is reshaping product development strategies within the automotive spring market. Manufacturers are prioritizing lightweight engineering solutions to enhance energy efficiency and vehicle range. This shift is encouraging the adoption of advanced materials and optimized spring designs that align with evolving automotive architectures. Additionally, the emergence of new vehicle manufacturing hubs across Asia, Latin America, and select Middle Eastern and African regions is creating opportunities for suppliers to establish localized production facilities and strengthen long-term partnerships with original equipment manufacturers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.1 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 6.5% |

The gas springs segment is anticipated to grow at a CAGR of 8.1% from 2026 to 2035. These components are increasingly integrated into modern vehicle systems to enable controlled motion and improved safety. Their ability to deliver smooth and precise movement enhances user convenience and operational reliability. In electric and hybrid vehicles, gas springs support specialized structural and interior applications that require accurate motion management. As global electric vehicle adoption accelerates in response to regulatory pressures and evolving consumer preferences, the importance of advanced gas spring solutions continues to rise.

The steel springs segment accounted for 63.9% share in 2025 and is expected to reach USD 4.8 billion by 2035. Despite fluctuations in raw material pricing, steel remains a preferred material due to its favorable strength-to-weight ratio and durability. Over the forecast period, steel springs are expected to maintain widespread adoption compared to alternatives such as composite or polymer-based variants. Their cost efficiency, large-scale manufacturing capability, and consistent quality standards make them a reliable option for both OEM production and aftermarket replacement demand. Established supply networks and competitive pricing further reinforce their dominance across mature and emerging automotive markets.

U.S. Automotive Spring Market reached USD 460.8 million in 2025. The country represents a significant market due to its extensive vehicle manufacturing base, robust aftermarket ecosystem, and strong production of passenger vehicles and light trucks. Continuous vehicle output and rising replacement demand driven by an aging fleet are supporting steady market expansion. Regulatory frameworks aimed at promoting zero-emission mobility by 2030 are influencing suspension component design requirements, prompting manufacturers to engineer spring systems that accommodate the weight distribution and performance characteristics of electric vehicles. At the same time, automakers are navigating evolving policy environments and supply chain complexities that impact procurement strategies.

Leading companies operating in the Global Automotive Spring Market include ZF Friedrichshafen, Thyssenkrupp, NHK Spring, Mubea, Mitsubishi Steel, GKN Automotive, Sogefi, Rassini, Lesjofors, and UNI AUTO. Companies in the Global Automotive Spring Market are reinforcing their competitive positioning through material innovation, geographic expansion, and strategic collaborations. Manufacturers are investing in lightweight spring technologies, including high-strength alloys and composite materials, to support electric vehicle performance requirements. Partnerships with OEMs are enabling co-development of customized spring solutions tailored to evolving vehicle platforms. Many firms are expanding production footprints in emerging automotive hubs to strengthen supply chain resilience and reduce logistics costs.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Load Capacity

- 2.2.5 Vehicle

- 2.2.6 Powertrain

- 2.2.7 End-Use

- 2.2.8 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production

- 3.2.1.2 Growing demand for commercial vehicles

- 3.2.1.3 Expansion of electric vehicle (EV) market

- 3.2.1.4 Increasing automotive aftermarket demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in raw material prices

- 3.2.2.2 High competition and price pressure

- 3.2.3 Market opportunities

- 3.2.3.1 Development of advanced lightweight spring materials

- 3.2.3.2 Growth in emerging automotive markets

- 3.2.3.3 Expansion of electric and hybrid vehicles

- 3.2.3.4 Strategic collaborations and OEM partnerships

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Transport Canada

- 3.4.1.3 U.S. Environmental Protection Agency (EPA)

- 3.4.1.4 California Air Resources Board (CARB)

- 3.4.1.5 SAE International

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 United Nations Economic Commission for Europe (UNECE)

- 3.4.2.3 European Automobile Manufacturers’ Association (ACEA)

- 3.4.2.4 European Committee for Standardization (CEN)

- 3.4.2.5 Kraftfahrt-Bundesamt (KBA)

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Industry and Information Technology (MIIT), China

- 3.4.3.2 China Automotive Technology and Research Center (CATARC)

- 3.4.3.3 Automotive Research Association of India (ARAI)

- 3.4.3.4 Korea Transportation Safety Authority (KOTSA)

- 3.4.4 Latin America

- 3.4.4.1 National Traffic Secretariat (SENATRAN)

- 3.4.4.2 INMETRO

- 3.4.4.3 Ministry of Infrastructure and Transport

- 3.4.4.4 Mexican Official Standards (NOM)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council Standardization Organization (GSO)

- 3.4.5.2 Emirates Authority for Standardization & Metrology (ESMA)

- 3.4.5.3 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 High-strength alloy steel springs

- 3.7.1.2 Lightweight composite leaf springs

- 3.7.1.3 Air spring integration in vehicles

- 3.7.2 Emerging technologies

- 3.7.2.1 Carbon fiber reinforced composite springs

- 3.7.2.2 Nano-coating for enhanced fatigue and corrosion resistance

- 3.7.1 Current technological trends

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact

- 3.11.1 Environmental impact assessment

- 3.11.2 Social impact & community benefits

- 3.11.3 Governance & corporate responsibility

- 3.11.4 Sustainable finance & investment trends

- 3.12 Product Lifecycle & Replacement Cycle Analysis

- 3.12.1 Average lifespan by spring type and vehicle segment

- 3.12.2 Failure modes and common wear patterns

- 3.12.3 Vehicle age distribution and aftermarket demand correlation

- 3.12.4 Impact of vehicle electrification on replacement cycles

- 3.12.5 Seasonal demand variations and stocking patterns

- 3.13 Vehicle electrification impact analysis

- 3.13.1 Weight distribution changes in EVs and spring design implications

- 3.13.2 Battery pack weight compensation requirements

- 3.13.3 Regenerative braking impact on suspension spring specifications

- 3.13.4 EV-specific spring durability and fatigue considerations

- 3.14 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Coil springs

- 5.3 Leaf springs

- 5.4 Torsion springs

- 5.5 Gas springs

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Steel springs

- 6.3 Composite springs

- 6.4 Plastic springs

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Load Capacity, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Light-duty springs

- 7.3 Medium-duty springs

- 7.4 Heavy-duty springs

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 LCV

- 8.3.2 MCV

- 8.3.3 HCV

- 8.4 Two wheelers

Chapter 9 Market Estimates & Forecast, By Powertrain, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 ICE

- 9.3 Electric & hybrid

- 9.3.1 BEV

- 9.3.2 HEV

- 9.3.3 PHEV

- 9.3.4 FCEV

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 Suspension system

- 10.3 Engine valves

- 10.4 Clutch assemblies

- 10.5 Transmission system

- 10.6 Others

Chapter 11 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Thousand Units)

- 11.1 Key trends

- 11.2 OEM

- 11.3 Aftermarket

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Czech Republic

- 12.3.7 Belgium

- 12.3.8 Russia

- 12.3.9 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.4.10 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 NHK Spring

- 13.1.2 Mubea

- 13.1.3 Sogefi

- 13.1.4 Rassini

- 13.1.5 GKN Automotive

- 13.1.6 Mitsubishi Steel

- 13.1.7 ZF Friedrichshafen

- 13.1.8 Thyssenkrupp

- 13.1.9 Lesjofors

- 13.2 Regional players

- 13.2.1 UNI AUTO

- 13.2.2 Kilen Springs

- 13.2.3 Olgun Celik

- 13.2.4 Clifford Springs

- 13.2.5 Soni Auto & Allied Industries

- 13.2.6 Emco Industries

- 13.2.7 Stanley Spring

- 13.3 Emerging players

- 13.3.1 Hendrickson

- 13.3.2 Auto Steels

- 13.3.3 Vikrant Auto

- 13.3.4 Protopower Springs

汽車時鐘彈簧市場:2026年至2032年全球預測(依產品類型、整合度、動力傳動系統類型、電路數量、安全氣囊點火系統配置、外殼材質、導體類型、車輛類別和銷售管道)

汽車時鐘彈簧市場:2026年至2032年全球預測(依產品類型、整合度、動力傳動系統類型、電路數量、安全氣囊點火系統配置、外殼材質、導體類型、車輛類別和銷售管道) 全球懸吊彈簧市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球懸吊彈簧市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2025-2029年全球汽車鋼板彈簧懸吊市場鋼板鋼板彈簧市場按類型、材質、製造流程和應用分類-2026年至2032年全球預測

2025-2029年全球汽車鋼板彈簧懸吊市場鋼板鋼板彈簧市場按類型、材質、製造流程和應用分類-2026年至2032年全球預測 汽車鋼板彈簧市場 - 全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、類型、材料、地區和競爭格局分類,2020-2030 年預測汽車鋼板彈簧和懸吊市場按產品類型、材料類型、車軸位置、車輛類型和最終用戶分類-2025-2030 年全球預測

汽車鋼板彈簧市場 - 全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、類型、材料、地區和競爭格局分類,2020-2030 年預測汽車鋼板彈簧和懸吊市場按產品類型、材料類型、車軸位置、車輛類型和最終用戶分類-2025-2030 年全球預測 全球懸吊彈簧市場

全球懸吊彈簧市場 按車型、材料、銷售通路、地區、機會和預測對全球汽車彈簧卸扣市場進行評估(2018 年至 2032 年)

按車型、材料、銷售通路、地區、機會和預測對全球汽車彈簧卸扣市場進行評估(2018 年至 2032 年) 到 2030 年汽車鋼板彈簧市場預測:按類型、材料類型、車型、銷售管道、應用和地區進行的全球分析全球汽車板簧市場規模:依彈簧類型、材料、零件類型、車輛、區域、範圍和預測

到 2030 年汽車鋼板彈簧市場預測:按類型、材料類型、車型、銷售管道、應用和地區進行的全球分析全球汽車板簧市場規模:依彈簧類型、材料、零件類型、車輛、區域、範圍和預測