|

市場調查報告書

商品編碼

1982325

2026 年至 2035 年微創手術器材的市場機會、成長要素、產業趨勢與預測。Minimally Invasive Surgical Instrument Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

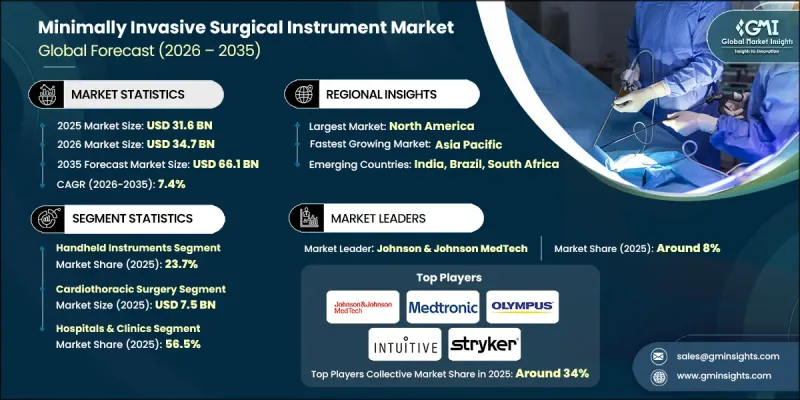

2025年全球微創手術器械市場價值為316億美元,預計到2035年將以7.4%的複合年成長率成長至661億美元。

微創手術需求的激增、機器人輔助手術的日益普及、技術的持續創新以及慢性病盛行率的上升是推動該市場成長的主要因素。人口老化和已開發國家門診手術的日益增加也進一步促進了市場成長。手術器械的最新進展拓展了微創手術在多個專科領域的應用範圍。觸覺回饋等技術增強了外科醫生的觸覺感知能力,而一次性先進能量器材則提高了醫療機構的無菌性和成本效益。機器人輔助平台的廣泛應用使得以往只能透過開放性手術完成的手術現在可以透過微創方式進行。總而言之,先進器械、手術效率的提高以及為醫院帶來的成本節約效益的結合,正在推動這些技術在全球範圍內的普及應用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 316億美元 |

| 預計金額 | 661億美元 |

| 複合年成長率 | 7.4% |

到2025年,手持式器械市場佔有率將達到23.7%。這些器械的創新重點在於人體工學設計、提高操作靈活性以觸及難以到達的解剖區域,以及採用輕便耐用的材料,例如鈦合金和先進聚合物。主要的手持式器械包括腹腔鏡抓鉗、剪刀、持針器和其他專用器械。一次性、無菌器材的需求也是推動此品類成長的重要因素。

預計2025年,心胸外科手術市場規模將達75億美元。與傳統手術方法相比,微創心血管手術通常切口較小,從而縮短恢復時間,降低感染風險,並減少功能障礙。機器人輔助平台可實現3D可視化並提高器械的靈活性,使瓣膜修復等精準手術更有效率且安全。

預計2025年,美國微創手術器械市場規模將達116億美元。該地區的成長主要得益於高昂的人均醫療成本、完善的醫保報銷體係以及對尖端醫療技術的早期應用。私人保險和聯邦醫療保險(Medicare)對微創手術的廣泛覆蓋,支撐了多個外科專科的需求。此外,醫療機構也逐漸意識到縮短住院時間和改善患者預後所帶來的成本效益,從而推動了對微創手術基礎設施的投資。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策及對資料完整性的承諾

- 資訊來源一致性通訊協定

- GMI人工智慧政策及對資料完整性的承諾

- 調查過程和可靠性評分

- 研究路徑的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充資訊

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 慢性病盛行率增加

- 外科器械的技術進步

- 機器人輔助手術的廣泛應用

- 微創手術的需求正在激增。

- 產業潛在風險與挑戰

- 手術器械高成本

- 開發中國家的還款挑戰

- 機會

- 電外科和能量設備領域的技術創新

- 遠端手術和遠端輔助手術的擴展

- 促進因素

- 成長潛力分析

- 監理情勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析

- 救贖方案

- 北美洲

- 歐洲

- 亞太地區

- 政策環境

- 供應鏈分析

- 對環境和永續發展的承諾

- 投資機會和創業投資趨勢

- 波特五力分析

- PESTEL 分析

- 差距分析

- 未來市場趨勢

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 手持裝置

- 夾爪

- 收縮器和升降器

- 擴充器

- 縫合器械

- 其他手持工具

- 監測和可視化設備

- 外科內視鏡

- 腹腔鏡

- 關節鏡

- 泌尿系統內視鏡

- 神經科學用內視鏡

- 其他內視鏡

- 擴充裝置

- 切削刀具

- 導向裝置

- 引導管

- 導管導引線

- 輔助器具

- 電外科設備

第6章 市場估計與預測:依手術類型分類,2022-2035年

- 心胸外科

- 整形外科手術

- 胃腸外科手術

- 泌尿系統手術

- 婦科手術

- 美容和肥胖手術

- 其他類型的手術

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院和診所

- 門診手術中心

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Abbott

- B. Braun

- Becton, Dickinson and Company

- Biorad Medisys

- Boston Scientific

- CONMED

- FUJIFILM

- Intuitive Surgical Operations

- Johnson & Johnson MedTech

- KARL STORZ

- Medtronic

- OLYMPUS

- Smith+Nephew

- Stryker

- WEXLER SURGICAL

- ZIMMER BIOMET

The Global Minimally Invasive Surgical Instrument Market was valued at USD 31.6 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 66.1 billion by 2035.

The market is propelled by a surge in demand for less invasive surgical procedures, wider adoption of robotic-assisted surgeries, ongoing technological innovation, and the increasing prevalence of chronic conditions. Aging populations and the rising trend of outpatient surgeries in developed countries are further supporting market expansion. Recent developments in surgical instruments have expanded the range of minimally invasive procedures across multiple specialties. Technologies such as haptic feedback have enhanced surgeons' tactile perception, while disposable advanced energy devices improve sterility and cost-effectiveness for healthcare facilities. Robotic-assisted platforms have become widely accessible, allowing procedures once limited to open surgeries to now be performed minimally invasively. Overall, the combination of advanced instrumentation, procedural efficiency, and hospital cost-saving benefits is driving the adoption of these technologies globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $31.6 Billion |

| Forecast Value | $66.1 Billion |

| CAGR | 7.4% |

The handheld instruments segment held a 23.7% share in 2025. Innovations in these devices focus on ergonomics, increased articulation for hard-to-reach anatomical areas, and the use of lightweight, durable materials like titanium alloys and advanced polymers. Core handheld tools include laparoscopic graspers, scissors, needle holders, and other specialty instruments. Emphasis on disposable and infection-free instruments is also supporting growth in this category.

The cardiothoracic surgery segment reached USD 7.5 billion in 2025. Minimally invasive cardiac procedures typically use smaller incisions rather than traditional approaches, reducing recovery times, infection risk, and functional limitations. Robotic-assisted platforms provide three-dimensional visualization and enhanced instrument articulation, enabling precise procedures such as valve repairs to be conducted more efficiently and safely.

U.S. Minimally Invasive Surgical Instrument Market was valued at USD 11.6 billion in 2025. Growth in the region is fueled by high per-capita healthcare spending, sophisticated reimbursement systems, and early adoption of cutting-edge medical technologies. The widespread coverage of minimally invasive procedures by private insurance and Medicare supports demand across multiple surgical specialties. Additionally, healthcare providers recognize the cost benefits of shorter hospital stays and improved patient outcomes, encouraging investment in minimally invasive infrastructure.

Key players in the Global Minimally Invasive Surgical Instrument Market include Johnson & Johnson MedTech, Intuitive Surgical Operations, Medtronic, B. Braun, Boston Scientific, Stryker, Abbott, OLYMPUS, Smith + Nephew, Becton, Dickinson and Company, KARL STORZ, ZIMMER BIOMET, WEXLER SURGICAL, FUJIFILM, and Biorad Medisys. Market leaders adopt several strategies to strengthen their presence. They focus heavily on research and development to launch advanced, ergonomically designed instruments and integrate robotic-assisted technology. Companies expand both direct and indirect distribution networks while forming strategic collaborations with hospitals and surgical centers to increase adoption. Marketing campaigns highlight clinical efficacy, procedural efficiency, and cost benefits, while training programs ensure surgeon proficiency with new devices. Firms also pursue mergers, acquisitions, and geographic expansion to gain market share and enhance global competitiveness, leveraging innovation and strong brand recognition to maintain leadership in the rapidly growing minimally invasive surgical instruments sector.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Surgery type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Technological advancements in surgical instruments

- 3.2.1.3 Growing adoption of robotic-assisted surgeries

- 3.2.1.4 Surging demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of surgical instruments

- 3.2.2.2 Reimbursement challenges in developing countries

- 3.2.3 Opportunities

- 3.2.3.1 Technological innovations in electrosurgical and energy devices

- 3.2.3.2 Expansion of tele-surgery and remote-assisted operations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis

- 3.7 Reimbursement scenario

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.8 Policy landscape

- 3.9 Supply chain analysis

- 3.10 Environmental and sustainability initiatives

- 3.11 Investment opportunities and venture capital trends

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

- 3.15 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Handheld instruments

- 5.2.1 Graspers

- 5.2.2 Retractors/elevators

- 5.2.3 Dilators

- 5.2.4 Suturing instruments

- 5.2.5 Other handheld instruments

- 5.3 Monitoring & visualization devices

- 5.4 Surgical scopes

- 5.4.1 Laparoscopes

- 5.4.2 Arthroscopes

- 5.4.3 Urology endoscopes

- 5.4.4 Neuroendoscopes

- 5.4.5 Other scopes

- 5.5 Inflation devices

- 5.6 Cutter instruments

- 5.7 Guiding devices

- 5.7.1 Guiding catheters

- 5.7.2 Guidewires

- 5.8 Auxiliary devices

- 5.9 Electrosurgical devices

Chapter 6 Market Estimates and Forecast, By Surgery Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiothoracic surgery

- 6.3 Orthopedic surgery

- 6.4 Gastrointestinal surgery

- 6.5 Urological surgery

- 6.6 Gynecological surgery

- 6.7 Cosmetic & bariatric surgery

- 6.8 Other surgery types

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals & clinics

- 7.3 Ambulatory surgical centers

- 7.4 Other end-users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 B. Braun

- 9.3 Becton, Dickinson and Company

- 9.4 Biorad Medisys

- 9.5 Boston Scientific

- 9.6 CONMED

- 9.7 FUJIFILM

- 9.8 Intuitive Surgical Operations

- 9.9 Johnson & Johnson MedTech

- 9.10 KARL STORZ

- 9.11 Medtronic

- 9.12 OLYMPUS

- 9.13 Smith + Nephew

- 9.14 Stryker

- 9.15 WEXLER SURGICAL

- 9.16 ZIMMER BIOMET

2026年全球拋棄式護臂市場報告

2026年全球拋棄式護臂市場報告 微創手術市場規模、佔有率和成長分析:按產品類型、手術類型、應用、最終用戶和地區分類-2026-2033年產業預測

微創手術市場規模、佔有率和成長分析:按產品類型、手術類型、應用、最終用戶和地區分類-2026-2033年產業預測 微創手術器材市場-全球產業規模、佔有率、趨勢、競爭格局、機會、預測:按類型、手術類型、最終用戶、地區和競爭格局分類,2021-2031年

微創手術器材市場-全球產業規模、佔有率、趨勢、競爭格局、機會、預測:按類型、手術類型、最終用戶、地區和競爭格局分類,2021-2031年 微創手術器材市場:2026-2032年全球市場預測(依產品類型、技術、易用性、手術類型、最終用戶和銷售管道分類)

微創手術器材市場:2026-2032年全球市場預測(依產品類型、技術、易用性、手術類型、最終用戶和銷售管道分類) 微創手術市場報告:按產品類型、應用、最終用戶和地區分類(2026-2034 年)微創手術市場:按設備類型、技術、應用和最終用戶分類-2026-2032年全球市場預測

微創手術市場報告:按產品類型、應用、最終用戶和地區分類(2026-2034 年)微創手術市場:按設備類型、技術、應用和最終用戶分類-2026-2032年全球市場預測 微創手術器材市場:按類型、手術類型、最終用戶、技術、國家和地區分類 - 全球行業分析、市場規模、市場佔有率和預測(2026-2033 年)2026年全球一次性腹腔鏡手術器械市場報告2026年全球微創尿失禁治療設備市場報告2026年全球微創手術器材市場報告

微創手術器材市場:按類型、手術類型、最終用戶、技術、國家和地區分類 - 全球行業分析、市場規模、市場佔有率和預測(2026-2033 年)2026年全球一次性腹腔鏡手術器械市場報告2026年全球微創尿失禁治療設備市場報告2026年全球微創手術器材市場報告