|

市場調查報告書

商品編碼

1982323

鋰離子電池回收市場機會、成長要素、產業趨勢分析及2026-2035年預測。Lithium-Ion Battery Recycling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

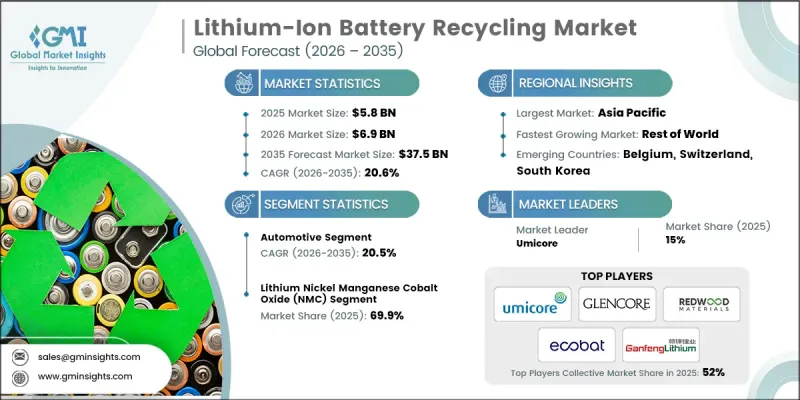

2025年全球鋰離子電池回收市場價值為58億美元,預計2035年將以20.6%的複合年成長率成長至375億美元。

該產業正迅速從專業環境服務領域轉型為全球清潔能源供應鏈的核心組成部分。近年來,濕式冶煉製程因其能夠比傳統冶煉製程更精確地回收鋰、鈷、鎳等高價值金屬而成為首選。更新後的法規結構進一步推動了這一轉變,其中包括獎勵金屬回收效率高的回收商的全球新規,並促進了水基提煉技術的更廣泛應用。此外,作為金屬進一步提取的中間體,黑料的生產和貿易也呈現強勁成長動能。小規模回收商正透過向大規模濕式冶煉廠供應黑料來拓展其在該領域的業務。隨著電動車、儲能計劃和製造業廢棄物產生的電池廢棄物數量不斷增加,預計該市場將在預測期內快速擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 58億美元 |

| 預測金額 | 375億美元 |

| 複合年成長率 | 20.6% |

預計到2035年,非汽車產業將以20.9%的複合年成長率成長。能源儲存系統(ESS)在電網穩定、商業備用電源和再生能源來源的應用日益廣泛,這極大地推動了電池需求,尤其是循環壽命長、安全性高的磷酸鋰鐵鋰電池。隨著老舊儲能系統逐漸達到運作終點,回收這些設備以獲取寶貴材料並確保下一代技術產能的需求日益成長,這進一步促進了市場成長。

預計到2025年,鋰鎳錳鈷氧化物(NMC)電池的市佔率將達到69.9%,並在2026年至2035年間以21%的複合年成長率成長。政府加強對電池處置和關鍵材料再利用的監管和政策措施,正在推動電池回收產業的成長。 NMC電池與已商業性化的熱回收和濕回收製程高度相容,能夠有效回收鎳、鈷和錳等金屬。此外,電動車和固定式儲能應用對高能量密度、長壽命和穩定熱性能的化學成分的需求不斷成長,進一步凸顯了NMC電池的優勢。

美國鋰離子電池回收市場預計2025年將佔86.5%的市場佔有率,到2035年市場規模將達到54億美元。聯邦政府的各項舉措,包括能源部津貼、稅收優惠以及兩黨共同支持的基礎設施立法下的投資,正在加速提升國內的回收能力。這些項目旨在減少對關鍵礦產進口的依賴,提高供應鏈的韌性,並支持循環經濟目標的實現,從而促進大規模回收計劃的發展。此外,電動車的快速普及也增加了廢棄鋰離子電池的數量,進而推動了對完善的回收基礎設施的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系統

- 原物料供應及採購分析

- 生產能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTEL 分析

- 成本結構分析

- 價格趨勢分析(美元/噸)

- 按化學成分

- 科技趨勢與顛覆

- 鹼性電池和可充電電池的市場佔有率擴張

- 鋰離子化學的發展

- 快速充電和高放電電池的創新

- 新興化學技術展望

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

- 競爭性標竿分析

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依化學成分分類,2022-2035年

- 鋰鎳錳鈷氧化物(NMC)

- 磷酸鋰鐵(LFP)

- 鈷酸鋰(LCO)

- 其他

第6章 市場規模及預測:依製程分類,2022-2035年

- 熱冶金

- 濕式冶煉

- 物理/機械

第7章 市場規模及預測:依來源分類,2022-2035年

- 車

- 非汽車

第8章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 法國

- 比利時

- 瑞士

- 德國

- 亞太地區

- 中國

- 韓國

- 日本

- 世界其他地區

第9章:公司簡介

- 3R Recycler

- Accurec Recycling

- ACE Green Recycling

- American Battery Technology Company

- Attero Recycling

- Altilium Metals

- BatX Energies

- Cylib

- Cirba Solutions

- Ecobat

- Eramet

- Glencore

- Ganfeng Lithium

- Lohum Cleantech

- Neometals

- Recyclus Group

- RecycLiCo Battery Material

- Redwood Materials

- SK TES

- Umicore

The Global Lithium-Ion Battery Recycling Market was valued at USD 5.8 billion in 2025 and is estimated to grow at a CAGR of 20.6% to reach USD 37.5 billion by 2035.

The industry has rapidly shifted from a specialized environmental service to a central part of the clean energy supply chain worldwide. Over the past few years, hydrometallurgical processes have become the preferred option due to their ability to recover high-value metals such as lithium, cobalt, and nickel with far greater precision than conventional smelting. This transition is further supported by updated regulatory frameworks, including new global rules that reward recyclers achieving high metal recovery efficiencies, encouraging wider adoption of water-based refining technologies. The industry is also experiencing strong momentum in the production and trade of black mass, which serves as an intermediate material for further metal extraction. Smaller recyclers are increasingly participating in this segment by supplying black mass to larger hydrometallurgical refiners. With the growing volume of battery waste generated from electric mobility, energy storage projects, and manufacturing scrap, the market is positioned for accelerated expansion throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.8 Billion |

| Forecast Value | $37.5 Billion |

| CAGR | 20.6% |

The non-automotive segment is projected to grow at a CAGR of 20.9% by 2035. Increasing deployment of energy storage systems (ESS) for grid stabilization, commercial backup power, and integration of renewable energy sources is driving strong demand for batteries, particularly lithium iron phosphate (LFP) chemistries, due to their long cycle life and enhanced safety. As older ESS units reach the end of their operational lifespan, the need for recycling rises to recover valuable materials and free capacity for next-generation technologies, further fueling market growth.

The lithium nickel manganese cobalt oxide (NMC) segment held a 69.9% share in 2025 and is expected to grow at a CAGR of 21% from 2026 to 2035. Strengthening government regulations and policies focused on battery disposal and critical material reuse are supporting the growth of the battery recycling sector. NMC batteries are highly compatible with both pyrometallurgical and hydrometallurgical recycling processes, which are already commercially mature, enabling efficient recovery of metals such as nickel, cobalt, and manganese. Additionally, growing preference for chemistries offering high energy density, long operational life, and stable thermal performance-key requirements for EVs and stationary storage applications is reinforcing the prominence of NMC batteries.

U.S. Lithium-Ion Battery Recycling Market held 86.5% share in 2025 and is expected to generate USD 5.4 billion by 2035. Federal initiatives, including Department of Energy (DOE) grants, tax incentives, and investments under the Bipartisan Infrastructure Law, are accelerating domestic recycling capacities. These programs aim to reduce reliance on imported critical minerals, improve supply chain resilience, and support circular economy objectives, encouraging large-scale recycling projects. The rapid increase in EV adoption is also producing a growing volume of spent lithium-ion batteries, intensifying demand for robust recycling infrastructure.

Major companies active in the Global Lithium-Ion Battery Recycling Market include Redwood Materials, Ganfeng Lithium, Umicore, Glencore, and Attero Recycling. Companies in the Lithium-Ion Battery Recycling Market are implementing multiple strategies to strengthen their presence and expand their competitive advantage. Many are investing heavily in hydrometallurgical capacity to improve recovery rates and reduce environmental impact, while also modernizing facilities with automation and advanced separation technologies. Firms are forging long-term supply agreements with EV manufacturers and battery producers to secure consistent waste streams. Strategic collaborations with government agencies help unlock funding and regulatory support for large-scale recycling initiatives.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Chemistry trends

- 2.4 Process trends

- 2.5 Source trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis

- 3.8 Price trend analysis (USD/Tons)

- 3.8.1 By chemistry

- 3.9 Technology trends & disruptions

- 3.9.1 Alkaline vs. rechargeable cannibalization

- 3.9.2 Lithium-ion chemistry evolution

- 3.9.3 Fast-charging & high-drain battery innovations

- 3.9.4 Emerging chemistries outlook

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Rest of world

- 4.3 Competitive benchmarking

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Chemistry, 2022 - 2035 (USD Billion & Thousand Tons)

- 5.1 Key trends

- 5.2 Lithium nickel manganese cobalt oxide (NMC)

- 5.3 Lithium iron phosphate (LFP)

- 5.4 Lithium cobalt oxide (LCO)

- 5.5 Others

Chapter 6 Market Size and Forecast, By Process, 2022 - 2035 (USD Billion & Thousand Tons)

- 6.1 Key trends

- 6.2 Pyrometallurgical

- 6.3 Hydrometallurgical

- 6.4 Physical/mechanical

Chapter 7 Market Size and Forecast, By Source, 2022 - 2035 (USD Billion & Thousand Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Non-automotive

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion & Thousand Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Belgium

- 8.3.4 Switzerland

- 8.3.5 Germany

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 South Korea

- 8.4.3 Japan

- 8.5 Rest of World

Chapter 9 Company Profiles

- 9.1 3R Recycler

- 9.2 Accurec Recycling

- 9.3 ACE Green Recycling

- 9.4 American Battery Technology Company

- 9.5 Attero Recycling

- 9.6 Altilium Metals

- 9.7 BatX Energies

- 9.8 Cylib

- 9.9 Cirba Solutions

- 9.10 Ecobat

- 9.11 Eramet

- 9.12 Glencore

- 9.13 Ganfeng Lithium

- 9.14 Lohum Cleantech

- 9.15 Neometals

- 9.16 Recyclus Group

- 9.17 RecycLiCo Battery Material

- 9.18 Redwood Materials

- 9.19 SK TES

- 9.20 Umicore

鋰離子電池回收市場:2026-2032 年全球市場預測,按電池來源、電池化學成分、回收製程、可回收組件、回收材料類型和最終用途細分。

鋰離子電池回收市場:2026-2032 年全球市場預測,按電池來源、電池化學成分、回收製程、可回收組件、回收材料類型和最終用途細分。 鋰離子電池回收:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

鋰離子電池回收:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 全球鋰離子電池回收市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球鋰離子電池回收市場規模、佔有率、趨勢和成長分析報告(2026-2034) 鋰離子電池回收市場預測至 2034 年—按來源、電池組件、回收流程、電池化學成分、最終用戶和地區進行全球分析。

鋰離子電池回收市場預測至 2034 年—按來源、電池組件、回收流程、電池化學成分、最終用戶和地區進行全球分析。 2026年全球鋰離子電池回收市場報告鋰離子電池NMP回收系統市場:依回收方法、電池化學、材料回收、來源、經營模式和應用分類-全球預測,2026-2032年鋰電池NMP回收市場:依製程、電池尺寸、純度等級及應用分類-2026-2032年全球預測鋰電池NMP回收設備市場:按類型、技術、最終用戶、容量、應用和銷售管道分類-2026-2032年全球預測鋰離子電池回收生產線市場:依製程類型、化學成分、回收階段、回收材料和應用分類-全球預測,2026-2032年

2026年全球鋰離子電池回收市場報告鋰離子電池NMP回收系統市場:依回收方法、電池化學、材料回收、來源、經營模式和應用分類-全球預測,2026-2032年鋰電池NMP回收市場:依製程、電池尺寸、純度等級及應用分類-2026-2032年全球預測鋰電池NMP回收設備市場:按類型、技術、最終用戶、容量、應用和銷售管道分類-2026-2032年全球預測鋰離子電池回收生產線市場:依製程類型、化學成分、回收階段、回收材料和應用分類-全球預測,2026-2032年 鋰離子電池回收市場規模、佔有率和趨勢分析:按應用、地區和細分市場預測(2026-2033 年)

鋰離子電池回收市場規模、佔有率和趨勢分析:按應用、地區和細分市場預測(2026-2033 年)