|

市場調查報告書

商品編碼

1982322

汽車電動驅動系統組件的市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。Automotive Electric Drivetrain Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

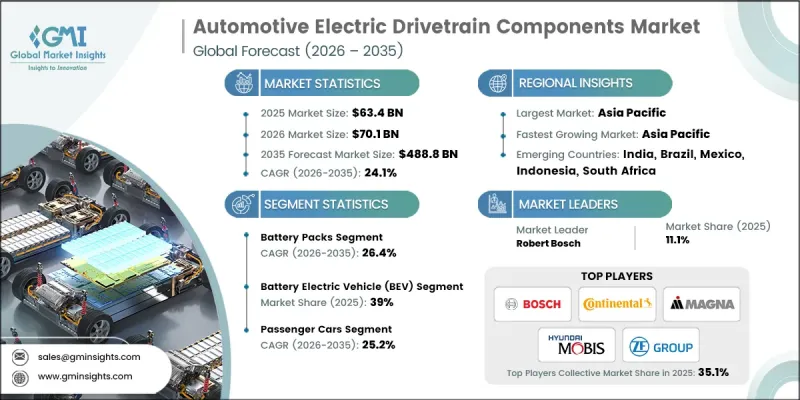

2025 年全球汽車電動傳動系統零件市場規模預計為 634 億美元,預計到 2035 年將達到 4,888 億美元,年複合成長率為 24.1%。

汽車產業整體的快速電氣化正在加速對先進電動驅動系統的需求。日益嚴格的全球排放氣體法規迫使汽車製造商加快向電動車(EV)平台轉型。這些監管壓力正推動電驅動系統、逆變器、電力電子設備和整合式電動推進模組的產量大幅成長。鋰離子電池製造成本的持續降低和生產效率的提高,進一步改變了汽車定價結構,並增強了電動車的競爭力。隨著電池成本的下降,製造商正在擴大輕量化馬達和高效能逆變器系統的生產規模,以滿足不斷成長的全球需求。動力傳動系統的進步也在提升續航里程、充電相容性和整體系統性能,從而促進電動車的廣泛普及。汽車製造商正在將智慧電橋、互聯控制模組和先進的診斷功能整合到電力傳動系統架構中,以最佳化即時監控和能量管理。法規要求、電池成本的下降以及以性能主導的創新,共同推動了電力傳動系統零件在全球汽車產業核心成長引擎中的地位日益提升。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 634億美元 |

| 預計金額 | 4888億美元 |

| 複合年成長率 | 24.1% |

預計到2025年,電池組市佔率將達到26%,並在2026年至2035年間以26.4%的複合年成長率成長。能量密度、電池管理系統和新一代電芯化學技術的持續進步正在提升續航里程和行車安全。業界關注的重點仍然是快速充電能力、更高的耐用性和成本最佳化。新興電池技術和不斷發展的材料成分預計將在整個預測期內進一步提升性能標準和生產規模。

預計到2025年,乘用車市佔率將達到65%,並在2026年至2035年間以25.2%的複合年成長率成長。排放氣體目標和對效率提升的追求正在推動乘用車領域電氣化的擴張。汽車製造商正在引入輕量化動力總成模組、模組化架構和高容量電池系統,以最佳化續航里程和聯網汽車。消費者正受益於不斷擴展的充電網路和政府的支持措施,這些措施正在加速都市區和郊區的普及。現代電動搭乘用融合了再生煞車、即時能量最佳化和車聯網系統等整合技術,而所有這些技術都依賴先進的電動動力總成零件。

預計到2025年,北美汽車電動傳動系統零件市場規模將達172億美元。各主要市場為統一電動車標準所做的區域性努力,正在緩解跨境供應限制,並推動傳動系統的大規模生產。供應商之間的產業合作正在加速下一代電驅動橋技術和整合推進平台的研發。同時,2025年充電基礎設施的持續擴張正在增強消費者信心,並進一步刺激對電動傳動系統零件的需求。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電動車的快速普及和電氣化進程的推進

- 嚴格的排放法規和政府政策

- 更低的電池成本和更高的技術性能

- 擴大電動車充電基礎設施

- 產業潛在風險與挑戰

- 高昂的生產成本和零件成本

- 供應鏈脆弱性與原料供應限制

- 市場機遇

- 先進的電力電子和輕量化模組設計

- 新興和發展中市場

- 永續性和回收解決方案

- 合作夥伴關係和跨行業夥伴關係

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 汽車創新聯盟

- 汽車工業行動小組

- 歐洲

- 歐洲汽車製造商協會

- 聯合國歐洲經濟委員會(UNECE)世界機動車法規協調論壇(WP.29)

- 亞太地區

- 亞太經合組織汽車對話

- 東協汽車聯盟

- 拉丁美洲

- 墨西哥電動車推廣協會

- 巴西電動車協會

- 中東和非洲

- 波灣合作理事會標準化組織

- 南非標準局

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析

- 產品特定定價

- 區域定價

- 生產統計

- 生產基地

- 消費者群體

- 出口和進口

- 成本細分分析

- 供應商成本結構

- 成本構成要素的應用

- 持續營運成本

- 客戶間接費用

- 專利分析

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 關於碳足跡的考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依組件分類,2022-2035年

- 電池組

- 電動驅動模組

- 直流/交流逆變器

- DC/DC轉換器

- 熱力系統

- 電源分配模組(PDM)

- 其他

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 電池式電動車(BEV)

- 混合動力電動車(HEV)

- 插電式混合動力汽車(PHEV)

- 燃料電池汽車(FCEV)

第7章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 輕型商用車

- MCV(中型商用車)

- 重型商用車(HCV)

第8章 市場估算與預測:依銷售管道分類,2022-2035年

- OEM

- 售後市場

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 波蘭

- 羅馬尼亞

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界公司

- Aisin

- BorgWarner

- Continental

- Denso

- Eaton

- Hitachi Astemo

- Hyundai Mobis

- Magna International

- Marelli

- Robert Bosch

- Valeo

- ZF Friedrichshafen

- 當地公司

- BYD Company

- Contemporary Amperex Technology

- Dana

- Infineon Technologies

- LG Energy Solution

- MAHLE

- Nidec

- Panasonic(Automotive Division)

- 新興企業

- American Axle &Manufacturing

- GKN Automotive(Dowlais Group)

- Mitsubishi Electric

- QuantumScape

- WiTricity

The Global Automotive Electric Drivetrain Components Market was valued at USD 63.4 billion in 2025 and is estimated to grow at a CAGR of 24.1% to reach USD 488.8 billion by 2035.

Rapid electrification across the automotive sector is accelerating demand for advanced electric drivetrain systems. Tightening emission standards worldwide compel original equipment manufacturers to transition toward electric vehicle platforms at a faster pace. This regulatory pressure is significantly increasing the production of e-drives, inverters, power electronics, and integrated electric propulsion modules. Continuous cost reductions in lithium-ion battery manufacturing and improvements in production efficiency are further reshaping vehicle pricing structures, making electric vehicles more competitive. As battery costs decline, manufacturers are scaling production of lightweight electric motors and high-efficiency inverter systems to meet growing global demand. Advancements in drivetrain technology are also enhancing vehicle range, charging compatibility, and overall system performance, which supports broader EV adoption. Automakers are integrating intelligent e-axles, connected control modules, and advanced diagnostics into electric drivetrain architectures to optimize real-time monitoring and energy management. The combination of regulatory mandates, falling battery costs, and performance-driven innovation is positioning electric drivetrain components as a core growth engine within the global automotive industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $63.4 Billion |

| Forecast Value | $488.8 Billion |

| CAGR | 24.1% |

The battery packs segment held a 26% share in 2025 and is anticipated to grow at a CAGR of 26.4% from 2026 to 2035. Ongoing advancements in energy density, battery management systems, and next-generation cell chemistries are improving driving range and operational safety. Industry focus remains centered on faster charging capabilities, enhanced durability, and cost optimization. Emerging battery technologies and evolving material compositions are expected to further strengthen performance benchmarks and manufacturing scalability throughout the forecast period.

The passenger cars segment accounted for 65% share in 2025 and is forecast to grow at a CAGR of 25.2% between 2026 and 2035. Emission reduction targets and the pursuit of improved efficiency drive increasing electrification within the passenger vehicle segment. Automakers are deploying lightweight drivetrain modules, modular architectures, and high-capacity battery systems to optimize range and vehicle dynamics. Consumers are benefiting from expanding charging networks and supportive government incentives, which are accelerating adoption across urban and suburban regions. Modern passenger electric vehicles incorporate integrated technologies such as regenerative braking, real-time energy optimization, and connected vehicle systems, all of which rely on advanced electric drivetrain components.

North America Automotive Electric Drivetrain Components Market reached USD 17.2 billion in 2025. Regional efforts to harmonize electric vehicle standards across major markets are reducing cross-border supply constraints and enabling higher-volume manufacturing of drivetrain systems. Industry collaboration among suppliers is fostering the development of next-generation e-axle technologies and integrated propulsion platforms. At the same time, continued expansion of charging infrastructure throughout 2025 is strengthening consumer confidence and stimulating further demand for electric drivetrain components.

Key companies operating in the Global Automotive Electric Drivetrain Components Market include Robert Bosch, BorgWarner, ZF Friedrichshafen, Magna International, Denso, Continental, GKN Automotive, Hyundai Mobis, Dana, and Hitachi Astemo. Companies competing in the Global Automotive Electric Drivetrain Components Market are reinforcing their competitive edge through sustained investment in research and development, strategic partnerships, and vertical integration. Manufacturers are advancing high-efficiency e-drive systems, compact inverters, and integrated e-axle platforms to enhance performance and reduce system weight. Collaborations with automakers secure long-term supply agreements and early-stage integration into new electric vehicle platforms. Firms are expanding production capacity and localizing supply chains to mitigate risk and improve responsiveness.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Application

- 2.2.4 Vehicle

- 2.2.5 Sales channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid EV adoption & electrification push

- 3.2.1.2 Strict emission regulations & government policies

- 3.2.1.3 Declining battery costs & improving tech performance

- 3.2.1.4 Expansion of EV charging infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production & component costs

- 3.2.2.2 Supply chain vulnerabilities & raw material constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Advanced power electronics & lightweight modular designs

- 3.2.3.2 Emerging & developing markets

- 3.2.3.3 Sustainability & recycling solutions

- 3.2.3.4 Collaborations & cross industry partnerships

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Alliance for Automotive Innovation

- 3.4.1.2 Automotive Industry Action Group

- 3.4.2 Europe

- 3.4.2.1 European Automobile Manufacturers’ Association

- 3.4.2.2 UNECE World Forum for Harmonization of Vehicle Regulations (WP.29)

- 3.4.3 Asia Pacific

- 3.4.3.1 APEC Automotive Dialogue

- 3.4.3.2 ASEAN Automotive Federation

- 3.4.4 Latin America

- 3.4.4.1 Mexican Association for the Promotion of Electric Vehicles

- 3.4.4.2 Brazilian Electric Vehicle Association

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council Standardization Organization

- 3.4.5.2 South African Bureau of Standards

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 Pricing by product

- 3.8.2 Pricing by region

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.10.1 Vendor cost structure

- 3.10.2 Implementation of cost components

- 3.10.3 Ongoing operational costs

- 3.10.4 Indirect customer costs

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Thousand units)

- 5.1 Key trends

- 5.2 Battery packs

- 5.3 Electric drive module

- 5.4 DC/AC inverter

- 5.5 DC/DC converter

- 5.6 Thermal system

- 5.7 Power distribution module (PDM)

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Thousand units)

- 6.1 Key trends

- 6.2 Battery electric vehicle (BEV)

- 6.3 Hybrid electric vehicle (HEV)

- 6.4 Plug-in hybrid electric vehicle (PHEV)

- 6.5 Fuel cell electric vehicle (FCEV)

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV (Light commercial vehicle)

- 7.3.2 MCV (Medium commercial vehicle)

- 7.3.3 HCV (Heavy commercial vehicle)

Chapter 8 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Mn, Thousand units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Aisin

- 10.1.2 BorgWarner

- 10.1.3 Continental

- 10.1.4 Denso

- 10.1.5 Eaton

- 10.1.6 Hitachi Astemo

- 10.1.7 Hyundai Mobis

- 10.1.8 Magna International

- 10.1.9 Marelli

- 10.1.10 Robert Bosch

- 10.1.11 Valeo

- 10.1.12 ZF Friedrichshafen

- 10.2 Regional players

- 10.2.1 BYD Company

- 10.2.2 Contemporary Amperex Technology

- 10.2.3 Dana

- 10.2.4 Infineon Technologies

- 10.2.5 LG Energy Solution

- 10.2.6 MAHLE

- 10.2.7 Nidec

- 10.2.8 Panasonic (Automotive Division)

- 10.3 Emerging players

- 10.3.1 American Axle & Manufacturing

- 10.3.2 GKN Automotive (Dowlais Group)

- 10.3.3 Mitsubishi Electric

- 10.3.4 QuantumScape

- 10.3.5 WiTricity

2026-2034年全球汽車電動傳動系統零件市場規模、佔有率、趨勢及成長分析報告全球汽車動力傳動系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)汽車傳動系統市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

2026-2034年全球汽車電動傳動系統零件市場規模、佔有率、趨勢及成長分析報告全球汽車動力傳動系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)汽車傳動系統市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 汽車動力傳動系統市場規模、佔有率、趨勢及預測(依車輛類型、動力傳動系統及地區分類,2026-2034年)

汽車動力傳動系統市場規模、佔有率、趨勢及預測(依車輛類型、動力傳動系統及地區分類,2026-2034年) 電動商用車馬達控制器市場(按控制器類型、額定功率、額定電壓、車輛類型、架構和最終用戶產業分類),全球預測(2026-2032年)

電動商用車馬達控制器市場(按控制器類型、額定功率、額定電壓、車輛類型、架構和最終用戶產業分類),全球預測(2026-2032年) 汽車動力傳動系統技術市場-全球產業規模、佔有率、趨勢、機會及預測(依車輛類型、技術、地區及競爭格局分類,2021-2031年預測)

汽車動力傳動系統技術市場-全球產業規模、佔有率、趨勢、機會及預測(依車輛類型、技術、地區及競爭格局分類,2021-2031年預測) 汽車動力傳動系統市場規模、佔有率和成長分析(按車輛類型、動力傳動系統、零件和地區分類)-2026-2033年產業預測

汽車動力傳動系統市場規模、佔有率和成長分析(按車輛類型、動力傳動系統、零件和地區分類)-2026-2033年產業預測 齒輪刮削機:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

齒輪刮削機:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 內齒輪滑齒機市場規模、佔有率和趨勢分析報告:按機器類型、自動化程度、齒輪尺寸、技術、最終用途、地區和細分市場預測(2025-2033 年)全球鎖轂市場按產品類型、材料類型、最終用途、車輛類型和分銷管道分類-2025-2030 年全球預測

內齒輪滑齒機市場規模、佔有率和趨勢分析報告:按機器類型、自動化程度、齒輪尺寸、技術、最終用途、地區和細分市場預測(2025-2033 年)全球鎖轂市場按產品類型、材料類型、最終用途、車輛類型和分銷管道分類-2025-2030 年全球預測