|

市場調查報告書

商品編碼

1982321

男性女乳症手術市場:成長機會、成長要素、產業趨勢分析及2026-2035年預測Gynecomastia Procedures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

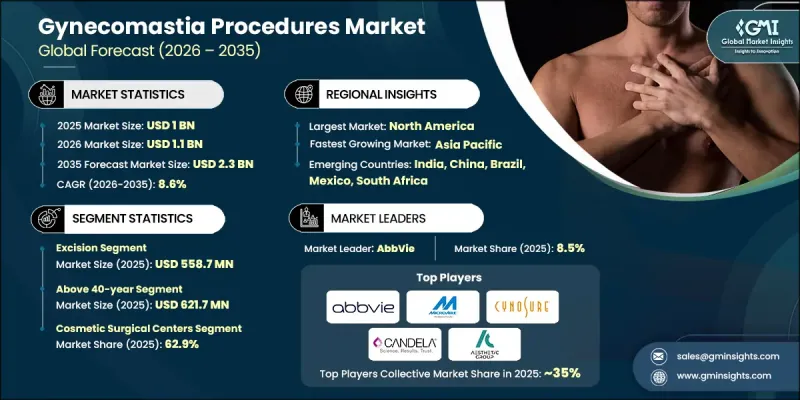

全球男性女乳症手術市場預計到 2025 年價值 10 億美元,預計到 2035 年將以 8.6% 的複合年成長率成長至 23 億美元。

市場成長動能主要受肥胖率上升、男性荷爾蒙失衡問題日益嚴重、外科手術技術持續創新所驅動。體脂率升高與內分泌失調密切相關,而雌激素活性升高(尤其是脂肪組織代謝引起的雌激素活性升高)會顯著增加男性女乳症的發生率。此外,胸部脂肪過度堆積往往是促使患者尋求矯正手術以改善醫療和美容效果的因素之一。肥胖負擔日益加重,加上公眾意識的提高、診斷率的提升以及社會對男性整形手術的接受度不斷提高,正推動著全球範圍內持續成長的手術需求。微創技術的進步和手術精準度的提升進一步增強了患者的信心,並在主要市場建立了長期治療模式。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 10億美元 |

| 預測金額 | 23億美元 |

| 複合年成長率 | 8.6% |

按手術類型分類,市場可分為抽脂術和切除術,其中切除術預計到2025年將創造5.587億美元的市場規模,佔據相當大的市場佔有率。切除術是指透過精心設計的切口精確切除乳房組織,對於僅靠消脂無法解決的緻密乳房組織,此方法能夠有效矯正。此方法可獲得可靠的塑形效果,尤其適用於中度至重度病例。其臨床療效和永久性切除組織的能力正推動著該技術在外科手術領域的持續發展。

以最終用戶分類,預計2025年,整形外科中心將佔據62.9%的市場。這些機構專門提供選擇性的整形手術,擁有專業知識、先進設備和經驗豐富的手術團隊,專注於男性乳房縮小手術。其高效的運作使其能夠接納更多患者並確保治療效果的穩定性。與醫院相比,整形外科中心通常提供更短的等待時間、更具競爭力的價格和更精簡的醫療服務模式。這些優點對自費患者極具吸引力,而自費患者正是尋求男性女乳症矯正手術的大多數患者。

從區域來看,預計到2025年,北美將佔據全球男性女乳症手術市場的40.5%以上。美國市場的成長主要得益於高肥胖率以及人們對男性女乳症作為一種可治療的醫療和美容問題的認知不斷提高。教育的普及、諮詢管道的增加以及數位化醫療的廣泛應用,都鼓勵了更多男性尋求專業治療。人們對男性健康和外表觀念的轉變,也持續推動著全部區域。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 肥胖症盛行率上升

- 越來越多的男性患有荷爾蒙失衡症。

- 科技的快速發展

- 人們對男性女乳症的認知不斷提高

- 產業潛在風險與挑戰

- 治療費用高昂

- 保險不涵蓋的情況

- 市場機遇

- 對微創手術的需求日益成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 科技趨勢

- 當前技術趨勢

- 新興技術

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略儀錶板

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依治療類型分類,2022-2035年

- 抽脂手術

- 切除

第6章 市場估計與預測:依年齡層別分類,2022-2035年

- 18-40歲

- 40歲以上

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 整形外科中心

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- MicroAire Surgical Instruments

- Lumenis

- Aesthetic Group

- Candela Corporation

- Johnson &Johnson

- Cutera

- Cynosure(Hologic, Inc.)

- AbbVie Inc.

- Solta Medical

- Sientra

The Global Gynecomastia Procedures Market was valued at USD 1 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 2.3 billion by 2035.

Market momentum is supported by the growing incidence of obesity, a rising population of men experiencing hormonal irregularities, and continuous technological innovation in surgical techniques. Higher body fat levels are closely linked to endocrine disruption, particularly elevated estrogen activity resulting from adipose tissue metabolism, which significantly increases the likelihood of gynecomastia. In addition, excess fat accumulation in the chest region often leads patients to pursue corrective procedures for both medical and aesthetic improvement. The expanding burden of obesity, combined with greater awareness, improved diagnosis rates, and broader social acceptance of male aesthetic procedures, is translating into sustained procedural demand worldwide. Advancements in minimally invasive technologies and enhanced surgical precision are further strengthening patient confidence and long-term treatment adoption across key markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 8.6% |

By procedure type, the market is categorized into liposuction and excision, with the excision segment generating USD 558.7 million in 2025 and accounting for a substantial share. Excision procedures involve the precise removal of glandular breast tissue through carefully placed incisions, enabling effective correction in cases where dense tissue cannot be addressed through fat removal techniques alone. This method provides reliable contouring outcomes and is particularly suited for moderate to advanced presentations. Its clinical effectiveness and ability to deliver permanent tissue removal continue to drive adoption across surgical practices.

In terms of end use, the cosmetic surgical centers segment captured 62.9% share in 2025. These facilities are specifically structured to deliver elective aesthetic procedures, offering specialized expertise, advanced equipment, and experienced surgical teams focused on male breast reduction treatments. Their operational efficiency supports higher patient throughput and consistent results. Compared to hospital settings, cosmetic surgical centers generally provide shorter scheduling timelines, competitive pricing structures, and streamlined care delivery models. These advantages strongly appeal to self-funded patients, who represent a significant portion of individuals seeking gynecomastia correction.

Regionally, North America accounted for more than 40.5% of the global gynecomastia procedures industry share in 2025. Growth across the U.S. market is largely fueled by the high prevalence of obesity and increasing recognition of gynecomastia as a manageable medical and cosmetic concern. Broader education initiatives, expanded consultation access, and digital health engagement have encouraged more men to pursue professional treatment. Evolving perceptions surrounding male wellness and physical appearance continue to support procedural uptake throughout the region.

Key companies active in the Global Gynecomastia Procedures Market include Johnson & Johnson, AbbVie Inc., Candela Corporation, Cutera, Lumenis, Cynosure, Solta Medical, Sientra, MicroAire Surgical Instruments, and Aesthetic Group. Companies operating in the Gynecomastia Procedures Market are strengthening their competitive position through innovation, portfolio expansion, and strategic collaborations. Leading players are investing heavily in advanced surgical technologies that improve precision, reduce recovery time, and enhance patient outcomes. Many firms are broadening their aesthetic device portfolios to address evolving clinical preferences and surgeon demand. Partnerships with cosmetic surgical centers and specialty clinics are helping manufacturers expand distribution networks and increase product visibility. Organizations are also prioritizing physician training programs and hands-on workshops to build brand loyalty and encourage product adoption. In addition, mergers, acquisitions, and geographic expansion strategies are being implemented to reinforce global presence and capture emerging growth opportunities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Procedure type trends

- 2.2.2 Age group trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of obesity

- 3.2.1.2 Rising number of men affected by hormonal imbalances

- 3.2.1.3 Upsurge in technological advancements

- 3.2.1.4 Increasing awareness regarding gynecomastia

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of procedures

- 3.2.2.2 Lack of reimbursement scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for minimally invasive procedures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Procedure Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Liposuction

- 5.3 Excision

Chapter 6 Market Estimates and Forecast, By Age Group, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 18-40 years

- 6.3 Above 40 years

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Cosmetic surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.4 Italy

- 8.3.5 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 MicroAire Surgical Instruments

- 9.2 Lumenis

- 9.3 Aesthetic Group

- 9.4 Candela Corporation

- 9.5 Johnson & Johnson

- 9.6 Cutera

- 9.7 Cynosure (Hologic, Inc.)

- 9.8 AbbVie Inc.

- 9.9 Solta Medical

- 9.10 Sientra