|

市場調查報告書

商品編碼

1982317

液封真空幫浦市場:成長機會、成長要素、產業趨勢分析及2026-2035年預測。Liquid Ring Vacuum Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

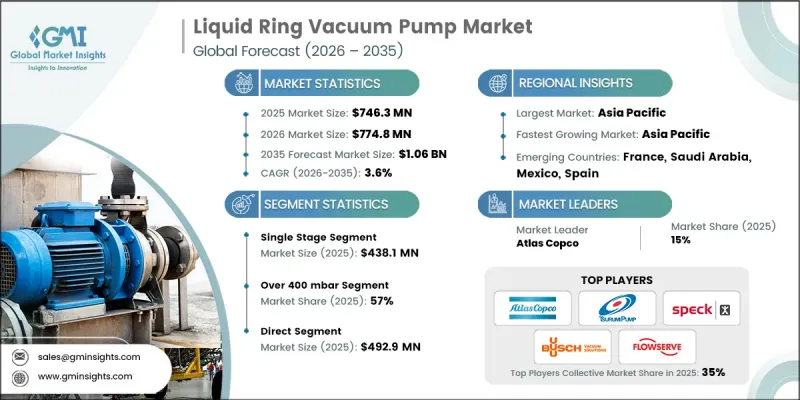

預計到 2025 年,全球液封真空幫浦市場規模將達到 7.463 億美元,年複合成長率為 3.6%,預計到 2035 年將達到 10.6 億美元。

液封真空幫浦的需求主要來自核心製程工業,這些產業對處理潮濕、飽和或受污染氣體至關重要。化學、製藥、食品飲料、石油天然氣以及紙漿造紙等行業越來越依賴即使在製程條件波動的情況下也能穩定可靠運作的真空系統。隨著產能的提升和現有系統的現代化改造,製造商優先考慮那些能夠確保運作穩定性、低維護成本和抗污染性的真空解決方案。液封真空幫浦尤其適用於蒸餾、溶劑回收、真空乾燥、過濾和脫氣等應用,並且已成為許多工業製程中不可或缺的設備。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 7.463億美元 |

| 預測金額 | 10.6億美元 |

| 複合年成長率 | 3.6% |

對能夠長期穩定運作且維護成本低的真空幫浦的需求日益成長,進一步推動了連續加工和自動化的發展。液環泵結構簡單,對異物、液體和腐蝕性蒸氣具有很高的耐受性,是生產含固體或水分氣體的設備的理想選擇。其可靠性和操作柔軟性可最大限度地減少停機時間,尤其是在嚴苛的工業環境中。

到2025年,單級泵浦市場規模將達到4.381億美元。單級液封真空幫浦採用單級壓縮結構,其葉輪在部分充液的泵浦殼內偏心旋轉,形成穩定的液環,從而平穩地壓縮氣體。此設計可實現無脈動運行,並能安全處理潮濕、飽和或受污染的氣體,使其適用於工況波動較大且濕度較高的製程環境。

到2025年,泵壓超過400毫巴的泵浦將佔57%的市場。這些幫浦即使在工況波動的情況下也能保持穩定的吸力,因此非常適合處理高濕度氣體或大顆粒氣體等無需極高真空的應用。其高泵壓性能使其能夠有效地進行蒸氣處理、真空脫氣、過濾器支撐和流體輸送,而無需產生極低的絕對壓力。

預計到2025年,美國液封真空幫浦市佔率將達到82.9%,市場規模將達到1.584億美元。強大的工業基礎,以及化學、製藥、食品加工和能源等行業對真空技術的高需求,正在推動液封真空幫浦的需求成長。液封真空幫浦能夠處理飽和氣體、波動負載和惡劣的運作條件,符合美國對運作安全、製程穩定性和環境法規合規性的要求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 流程工業的需求不斷成長

- 人們越來越關注環境合規性

- 工業化和自動化流程

- 產業潛在風險與挑戰

- 有限真空

- 高用水量

- 機會

- 兩級LRVP設計的進展

- 以永續發展主導的創新

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 單級

- 兩階段

第6章 市場估計與預測:依材料分類,2022-2035年

- 鑄鐵

- 不銹鋼

- 其他

第7章 市場估計與預測:依產能分類,2022-2035年

- 200毫巴或更低

- 200~400 mbar

- 超過400毫巴

第8章 市場估算與預測:依交通量分類,2022-2035年

- 25~600 m3/h

- 600~3000 m3/h

- 3,000~10,000 m3/h

- 超過10,000立方米

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 石油化工/化工

- 製藥

- 食品製造

- 飛機

- 車

- 水處理

- 石油和天然氣

- 發電

- EPS和塑膠

- 紙漿和造紙

- 其他

第10章 市場估價與預測:依通路分類,2022-2035年

- 直接地

- 間接

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- Atlas Copco

- Busch Vacuum Solutions

- Cutes

- Dekker Vacuum

- Finder

- Flowserve

- Graham Engineering

- Ingersoll Rand

- Omel

- PPI Pumps

- Samson

- Speck Pumpen

- Tsurumi

- Vooner

- Zibo Zhaohan

The Global Liquid Ring Vacuum Pump Market was valued at USD 746.3 million in 2025 and is estimated to grow at a CAGR of 3.6% to reach USD 1.06 billion by 2035.

Demand for liquid ring vacuum pumps is primarily driven by core process industries, where handling wet, saturated, or contaminated gases is essential. Industries such as chemicals, pharmaceuticals, food and beverage, oil and gas, and pulp and paper rely heavily on vacuum systems that provide stable, reliable operation under variable process conditions. As production capacity increases and existing systems are modernized, manufacturers are prioritizing vacuum solutions that ensure operational stability, low maintenance, and resilience to contamination. Liquid ring pumps are particularly suitable for applications like distillation, solvent recovery, vacuum drying, filtering, and degassing, making them indispensable for many industrial processes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $746.3 Million |

| Forecast Value | $1.06 Billion |

| CAGR | 3.6% |

The adoption of continuous processing and automation further supports the need for vacuum pumps capable of extended, low-maintenance operation. Liquid ring pumps, with their simple mechanical design and high tolerance for debris, liquids, and corrosive vapors, are ideal for facilities producing gas streams containing solids or moisture. Their reliability and operational flexibility ensure minimal downtime, particularly in demanding industrial environments.

In 2025, the single-stage pumps segment reached USD 438.1 million. Single-stage liquid ring vacuum pumps feature a single compression stage with an impeller rotating eccentrically within a partially liquid-filled casing, forming a stable liquid ring that compresses gas smoothly. This design delivers pulsation-free operation while safely handling wet, saturated, or contaminated gases, making them suitable for processes with variable conditions or high moisture content.

The pumps with discharge capabilities above 400 mbar segment held 57% share in 2025. These pumps maintain steady suction under varying conditions, making them ideal for applications involving high-moisture gases or large particles, where deep vacuum is unnecessary. Their performance at higher discharge pressures allows them to efficiently handle vapors, vacuum degassing, filter support, and fluid transfer without creating extremely low absolute pressure.

U.S. Liquid Ring Vacuum Pump Market accounted for 82.9% share in 2025, generating USD 158.4 million. The strong industrial framework, coupled with significant vacuum technology requirements across chemical, pharmaceutical, food processing, and energy sectors, supports demand for liquid ring vacuum pumps. Their ability to manage saturated gases, variable loads, and extreme operating conditions aligns with the U.S. focus on operational safety, process stability, and environmental compliance.

Key players in the Global Liquid Ring Vacuum Pump Market include Atlas Copco, Dekker Vacuum, Ingersoll Rand, Flowserve, Tsurumi, Samson, Graham Engineering, Vooner, Omel, Speck Pumpen, PPI Pumps, Busch Vacuum Solutions, Finder, Cutes, and Zibo Zhaohan. Companies in the Liquid Ring Vacuum Pump Market are pursuing multiple strategies to strengthen their presence and market foothold. These include expanding manufacturing capacities, developing advanced, energy-efficient, and corrosion-resistant models, and investing in R&D to enhance performance under variable process conditions. Strategic collaborations with end-user industries and after-sales service networks improve market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Capacity

- 2.2.5 Flow rate

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand from process industries

- 3.2.1.2 Growing focus on environmental compliance

- 3.2.1.3 Rising industrialization and automation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Limited vacuum depth

- 3.2.2.2 High water consumption

- 3.2.3 Opportunities

- 3.2.3.1 Advancements in two-stage LRVP designs

- 3.2.3.2 Sustainability-driven innovations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million) (Million Units)

- 5.1 Key trends

- 5.2 Single stage

- 5.3 Two stages

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Million) (Million Units)

- 6.1 Key trends

- 6.2 Cast iron

- 6.3 Stainless steel

- 6.4 Other

Chapter 7 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Million) (Million Units)

- 7.1 Key trends

- 7.2 Up to 200 mbar

- 7.3 200 to 400 mbar

- 7.4 Over 400 mbar

Chapter 8 Market Estimates and Forecast, By Flow Rate, 2022 - 2035 (USD Million) (Million Units)

- 8.1 Key trends

- 8.2 25 - 600 M3H

- 8.3 600 - 3000 M3H

- 8.4 3000 - 10000 M3H

- 8.5 Over 10000 M3

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million) (Million Units)

- 9.1 Key trends

- 9.2 Petrochemical & chemical

- 9.3 Pharmaceutical

- 9.4 Food manufacturing

- 9.5 Aircraft

- 9.6 Automobile

- 9.7 Water treatment

- 9.8 Oil & gas

- 9.9 Power generation

- 9.10 EPS and plastics

- 9.11 Pulp & paper

- 9.12 Others

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Million) (Million Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Atlas Copco

- 12.2 Busch Vacuum Solutions

- 12.3 Cutes

- 12.4 Dekker Vacuum

- 12.5 Finder

- 12.6 Flowserve

- 12.7 Graham Engineering

- 12.8 Ingersoll Rand

- 12.9 Omel

- 12.10 PPI Pumps

- 12.11 Samson

- 12.12 Speck Pumpen

- 12.13 Tsurumi

- 12.14 Vooner

- 12.15 Zibo Zhaohan