|

市場調查報告書

商品編碼

1982315

實體安防市場機會、成長要素、產業趨勢分析及2026-2035年預測Physical Security Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

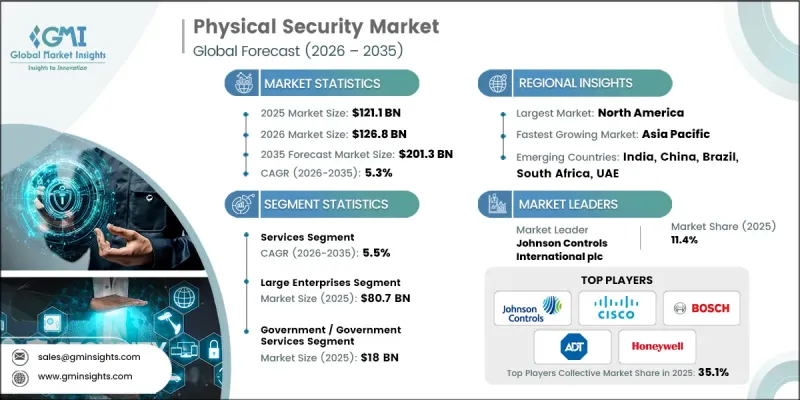

預計到 2025 年,全球實體安全市場價值將達到 1,211 億美元,並以 5.3% 的複合年成長率成長,到 2035 年將達到 2,013 億美元。

隨著人工智慧驅動的監控、智慧影像分析和整合安全系統成為保護商業、工業和關鍵基礎設施資產的必備工具,市場正在不斷擴張。日益成長的都市化計劃以及複雜的網路物理威脅進一步推動了這些技術的應用。商業房地產和工業設施的開發催生了對多層安全解決方案的需求,這些解決方案旨在保護資產、人員和流程。企業和政府機構正在投資物聯網賦能的雲端整合系統,這些系統融合了門禁控制、周界安全和監控功能,以降低與破壞、恐怖主義和營運中斷相關的風險。隨著對合規性、集中監控和即時分析的日益重視,實體安全不再只是一項可選項,而是核心營運需求。製造商不斷創新,致力於提供擴充性、可靠的人工智慧解決方案,以滿足不同行業的多樣化需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 1211億美元 |

| 預測金額 | 2013億美元 |

| 複合年成長率 | 5.3% |

預計到2025年,系統市場規模將達到271億美元,這主要得益於政府、商業和工業領域對整合監控、存取控制和周界防護技術的日益普及。企業正在採用擴充性的、人工智慧驅動的平台來提升威脅偵測能力和營運效率。生物識別、雲端監控和物聯網感測器等先進技術正被廣泛整合,尤其是在智慧城市計劃中,以增強情境察覺並實現對安全事件的即時回應。企業正在開發全面、可互操作系統,以滿足大規模基礎設施計劃的需求。

到2025年,大型企業市場規模將達到807億美元。在多個地點營運的公司正在大力投資端到端安全基礎設施,以保護關鍵資產並確保員工安全。人工智慧、物聯網和雲端對應平臺是先進安全解決方案的核心。遵守監管和企業管治要求進一步推動了這些解決方案的普及,加速了監控、存取控制和集中式監控系統的部署。製造商正專注於提供具備高階分析、擴充性和整合能力的企業級解決方案,以滿足複雜的營運和監管要求。

2025年,北美實體安防市佔率將達到34.3%。該地區的成長主要得益於企業、商業設施和政府機構對整合安防解決方案的廣泛應用。人工智慧驅動的監控、智慧門禁和集中式管理平台正在提升威脅偵測能力和營運效率。監管合規、網路安全整合以及對智慧城市專案的投資,正在推動工業園區、交通樞紐和企業園區等場所部署先進系統。製造商正優先開發面向聯邦政府和企業客戶的互通性且擴充性的平台,並透過人工智慧和雲端技術的整合,提供差異化的產品和服務。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 人工智慧驅動的監控和智慧影像分析

- 商業地產和工業設施的成長

- 恐怖主義、網路和實體威脅日益加劇,以及關鍵基礎設施的保護

- 物聯網、雲端運算和門禁控制技術的整合

- 都市化與智慧城市理念

- 陷阱與挑戰

- 資料隱私問題和監管限制

- 較高的初始實施和整合成本

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新經營模式

- 合規要求

- 供應鏈韌性

- 國防預算分析

- 全球國防費用趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 主要國防現代化項目

- 預算預測(2025-2034 年)

- 對產業成長的影響

- 國防預算

- 分段式國防預算分配

- 人員

- 運作/維護

- 採購

- 研究、開發、測試和評估

- 基礎設施和建築

- 技術與創新

- 永續發展計劃

- 供應鏈韌性

- 地緣政治分析

- 勞動力分析

- 數位轉型

- 併購和策略聯盟的趨勢

- 風險評估與管理

- 重大合約授予情況(2022-2025 年)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域部署對比

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 產品系列比較

- 2022-2025 年重大發展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 永續發展計劃

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依服務類型分類,2022-2035年

- 系統

- 實體存取控制系統

- 影像監控系統

- 邊界入侵偵測與預防

- 實體安全資訊管理(PSIM)

- 實體身分和存取管理 (PIAM)

- 安全掃描

- 影像處理和金屬檢測

- 消防/生命安全

- 服務

- 專業服務

- 託管服務

第6章 市場估計與預測:依公司規模分類,2022-2035年

- 中小企業

- 主要企業

第7章 市場估計與預測:依最終用戶產業分類,2022-2035年

- 銀行、金融服務和保險(BFSI)

- 衛生保健

- 政府

- 零售與電子商務

- 能源與公共產業

- 溝通

- 運輸/物流

- 住宅

- 教育

- 航太/國防

- 資訊科技與資訊科技服務

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- 主要企業

- Johnson Controls International

- Honeywell International Inc.

- Bosch Security Systems(Robert Bosch GmbH)

- Siemens AG

- Schneider Electric SE

- 按地區分類的主要企業

- 北美洲

- ADT Inc.

- Motorola Solutions, Inc.

- Genetec Inc.

- 歐洲

- ASSA ABLOY AB

- Allegion plc

- Axis Communications AB

- 亞太地區

- Hikvision Digital Technology Co., Ltd.

- Dahua Technology Co., Ltd.

- Hanwha Vision(Hanwha Group)

- 北美洲

- 小眾/顛覆者

- Thales Group

The Global Physical Security Market was valued at USD 121.1 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 201.3 billion by 2035.

The market is expanding as AI-driven surveillance, intelligent video analytics, and integrated security systems become essential for protecting commercial, industrial, and critical infrastructure assets. Rising urbanization, smart city initiatives, and the increasing sophistication of cyber-physical threats are further driving adoption. The development of commercial real estate and industrial facilities is fueling demand for multi-layered security solutions that safeguard assets, personnel, and processes. Enterprises and government agencies are investing in IoT-enabled, cloud-integrated systems, combining access control, perimeter security, and surveillance to mitigate risks associated with vandalism, terrorism, and operational failures. Emphasis on regulatory compliance, centralized monitoring, and real-time analytics is making physical security a core operational requirement rather than an optional investment. Manufacturers are innovating to provide scalable, reliable, and AI-powered solutions tailored to diverse industry requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $121.1 Billion |

| Forecast Value | $201.3 Billion |

| CAGR | 5.3% |

The systems segment was valued at USD 27.1 billion in 2025, driven by increasing deployment of integrated surveillance, access control, and perimeter protection across government, commercial, and industrial sectors. Enterprises are adopting scalable AI-enabled platforms for enhanced threat detection and operational efficiency. Advanced technologies such as biometric authentication, cloud monitoring, and IoT sensors are being widely integrated, particularly in smart city projects, enhancing situational awareness and enabling real-time responses to security incidents. Companies are developing comprehensive, interoperable systems to meet the needs of large-scale infrastructure projects.

The large enterprises segment accounted for USD 80.7 billion in 2025. Corporations with multi-site operations are investing heavily in end-to-end security infrastructures to safeguard critical assets and ensure employee safety. AI, IoT, and cloud-enabled platforms are central to advanced security solutions. Compliance with regulations and corporate governance requirements further drives adoption, encouraging deployment of surveillance, access control, and centralized monitoring systems. Manufacturers are focusing on enterprise-grade solutions with advanced analytics, scalability, and integration capabilities to address complex operational and regulatory demands.

North America Physical Security Market held a 34.3% share in 2025. Growth in the region is fueled by the adoption of integrated security solutions across enterprises, commercial facilities, and government institutions. AI-powered monitoring, smart access control, and centralized management platforms are enhancing threat detection and operational efficiency. Regulatory compliance, cybersecurity integration, and investments in smart city initiatives are supporting the deployment of advanced systems for industrial complexes, transportation hubs, and corporate campuses. Manufacturers are prioritizing interoperable, scalable platforms designed for federal and enterprise clients, integrating AI and cloud technologies to create differentiated offerings.

Key players operating in the Global Physical Security Market include Johnson Controls International, Honeywell International Inc., Bosch Security Systems (Robert Bosch GmbH), Hikvision Digital Technology Co., Ltd., Dahua Technology Co., Ltd., Axis Communications AB, ASSA ABLOY AB, Allegion plc, Siemens AG, Schneider Electric SE, Genetec Inc., Motorola Solutions Inc., Hanwha Vision (Hanwha Group), ADT Inc., and Thales Group. Companies in the Global Physical Security Market are implementing several strategies to strengthen their market position and expand global reach. Leading players are investing in AI-powered and IoT-integrated platforms to enhance real-time monitoring, predictive threat detection, and centralized management capabilities. Strategic partnerships with smart city initiatives, commercial developers, and government agencies allow for large-scale deployments and improved market penetration. Firms are focusing on modular, scalable, and interoperable solutions to serve enterprise and multi-site operations efficiently. Product innovation, including biometric authentication, cloud-based management, and integrated perimeter security, is enhancing differentiation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Offering trends

- 2.2.2 Organization size trends

- 2.2.3 End-user industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 AI-enabled surveillance and intelligent video analytics

- 3.2.1.2 Growth in commercial real estate and industrial facilities

- 3.2.1.3 Increasing terrorism, cyber-physical threats, and critical infrastructure protection

- 3.2.1.4 Integration of IoT, cloud, and access control technologies

- 3.2.1.5 Rising urbanization and smart city initiatives

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 Data privacy concerns and regulatory restrictions

- 3.2.2.2 High initial deployment and integration costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Defense Budget Analysis

- 3.12 Global Defense Spending Trends

- 3.13 Regional Defense Budget Allocation

- 3.13.1 North America

- 3.13.2 Europe

- 3.13.3 Asia Pacific

- 3.13.4 Middle East and Africa

- 3.13.5 Latin America

- 3.14 Key Defense Modernization Programs

- 3.15 Budget Forecast (2025-2034)

- 3.15.1 Impact on Industry Growth

- 3.15.2 Defense Budgets by Country

- 3.15.3 Defense Budget Allocation by Segment

- 3.15.3.1 Personnel

- 3.15.3.2 Operations and Maintenance

- 3.15.3.3 Procurement

- 3.15.3.4 Research, Development, Test and Evaluation

- 3.15.3.5 Infrastructure and Construction

- 3.15.3.6 Technology and Innovation

- 3.16 Sustainability Initiatives

- 3.17 Supply Chain Resilience

- 3.18 Geopolitical Analysis

- 3.19 Workforce Analysis

- 3.20 Digital Transformation

- 3.21 Mergers, Acquisitions, and Strategic Partnerships Landscape

- 3.22 Risk Assessment and Management

- 3.23 Major Contract Awards (2022-2025)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Offerings, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Systems

- 5.2.1 Physical access control system

- 5.2.2 Video surveillance systems

- 5.2.3 Perimeter intrusion detection and prevention

- 5.2.4 Physical security information management (PSIM)

- 5.2.5 Physical identity and access management (PIAM)

- 5.2.6 Security scanning

- 5.2.7 Imaging & metal detection

- 5.2.8 Fire & life safety

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates and Forecast, By Organization Size, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 SMEs (Small & Medium-Sized Enterprises)

- 6.3 Large Enterprises

Chapter 7 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Banking, financial services & insurance (BFSI)

- 7.3 Healthcare

- 7.4 Government

- 7.5 Retail & ecommerce

- 7.6 Energy & utilities

- 7.7 Telecommunications

- 7.8 Transportation & logistics

- 7.9 Residential

- 7.10 Education

- 7.11 Aerospace & defense

- 7.12 IT & ITes

- 7.13 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Johnson Controls International

- 9.1.2 Honeywell International Inc.

- 9.1.3 Bosch Security Systems (Robert Bosch GmbH)

- 9.1.4 Siemens AG

- 9.1.5 Schneider Electric SE

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 ADT Inc.

- 9.2.1.2 Motorola Solutions, Inc.

- 9.2.1.3 Genetec Inc.

- 9.2.2 Europe

- 9.2.2.1 ASSA ABLOY AB

- 9.2.2.2 Allegion plc

- 9.2.2.3 Axis Communications AB

- 9.2.3 Asia Pacific

- 9.2.3.1 Hikvision Digital Technology Co., Ltd.

- 9.2.3.2 Dahua Technology Co., Ltd.

- 9.2.3.3 Hanwha Vision (Hanwha Group)

- 9.2.1 North America

- 9.3 Niche / Disruptors

- 9.3.1 Thales Group

實體安全市場:產業趨勢及2035年全球預測-按組件類型、系統類型、企業規模、產業和地區分類

實體安全市場:產業趨勢及2035年全球預測-按組件類型、系統類型、企業規模、產業和地區分類 實體安全市場:按組件、層級、組織規模、最終用戶和收入分類-2026-2032年全球市場預測

實體安全市場:按組件、層級、組織規模、最終用戶和收入分類-2026-2032年全球市場預測 人工智慧在實體安全領域的市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、技術、部署、功能、最終用途、地區和競爭格局分類,2021-2031年

人工智慧在實體安全領域的市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、技術、部署、功能、最終用途、地區和競爭格局分類,2021-2031年 2026年全球核能設施物理保護系統市場報告2026年全球實體安防市場報告

2026年全球核能設施物理保護系統市場報告2026年全球實體安防市場報告 2035年實體安全市場分析及預測:依類型、產品類型、服務、技術、組件、應用、最終用戶及部署類型分類2026年金融級安全晶片全球市場報告實體安防市場-全球產業規模、佔有率、趨勢、機會及預測(依系統類型、服務類型、公司規模、產業垂直領域、地區及競爭格局分類,2021-2031年)

2035年實體安全市場分析及預測:依類型、產品類型、服務、技術、組件、應用、最終用戶及部署類型分類2026年金融級安全晶片全球市場報告實體安防市場-全球產業規模、佔有率、趨勢、機會及預測(依系統類型、服務類型、公司規模、產業垂直領域、地區及競爭格局分類,2021-2031年) 全球零售業實體安全(2026-2030 年)

全球零售業實體安全(2026-2030 年) 實體安防市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034 年)

實體安防市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034 年)