|

市場調查報告書

商品編碼

1982295

硬質地板市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。Hard Surface Flooring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

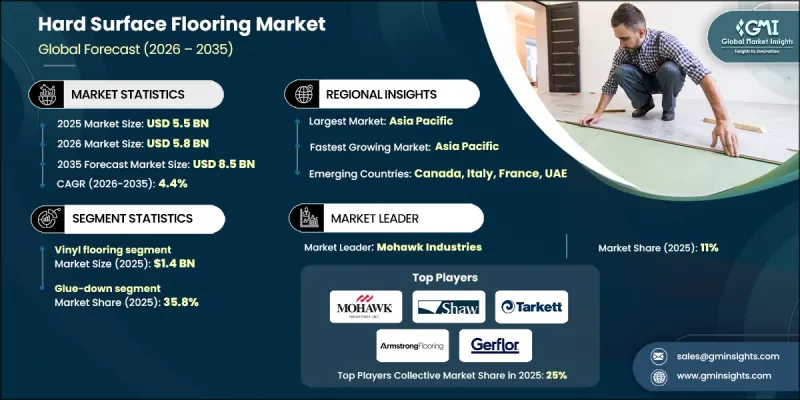

預計到 2025 年,全球硬質地板市場價值將達到 55 億美元,並預計以 4.4% 的複合年成長率成長,到 2035 年達到 85 億美元。

全球都市化和快速發展推動了住宅和商業領域對耐用、易於維護的地板材料解決方案的強勁需求。建設活動的增加,尤其是在亞太地區、非洲、拉丁美洲和其他新興地區,促進了對乙烯基、複合地板、瓷磚和工程木地板等材料的需求。政府推行的經濟適用住宅和智慧城市計劃進一步加速了新建築中硬地面的活性化。消費者可支配收入的成長也推動了對高品質、長壽命地板材料的投資。耐用性、美觀性和易於維護性至關重要,硬質地板正成為現代建築計劃的重要組成部分。辦公室、零售商店和飯店等商業空間,對長期性能和設計吸引力的重視,也推動了對硬地面的需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 55億美元 |

| 預測金額 | 85億美元 |

| 複合年成長率 | 4.4% |

預計到2025年,乙烯基(PVC)地板材料市場規模將達到14億美元。其受歡迎的原因在於價格實惠、用途廣泛且經久耐用,產品採用合成聚氯乙烯(PVC)製成,具有防潮和耐磨的特性。乙烯基(PVC)地板材料有多種形式,包括捲材、地磚和豪華乙烯基(LVP)地板,可為住宅和商業用途提供合適的選擇。先進的印刷技術使乙烯基(PVC)地板能夠模仿木材和石材的外觀,使其成為高檔材料的經濟實惠的替代品。

到2025年,黏合式安裝將佔據35.8%的市場。這種方法使用強力黏合劑將地板材料直接黏合到基層上,形成穩定持久的黏合,從而減少地板隨時間推移的位移。在對耐用性和性能要求極高的商業和住宅應用中,黏合式安裝都是首選。

美國硬地面地板材料市場佔64.4%的市場佔有率,預計2025年市場規模將達到9.111億美元。豪華乙烯基瓷磚、工程木地板和複合地板日益普及是推動市場需求成長的主要因素。住宅翻新和整修是主要驅動力,而商業設施也越來越傾向於選擇耐磨性更佳的地板材料材料。消費者越來越重視地板的功能性和美觀性,並更重視環保產品和時尚設計。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 快速的都市化與建設熱潮

- 可支配收入激增和房屋裝修趨勢

- 技術進步

- 產業潛在風險與挑戰

- 原物料價格波動

- 安裝成本和複雜性

- 機會

- 環保解決方案和生物基解決方案

- 智慧高性能地板材料

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 乙烯基地板材料

- 複合地板

- 實木地板

- 磁磚

- 磁磚

- 天然石材地板材料

- 混凝土地板材料

- 其他

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅

- 商業的

- 辦公室

- 零售空間

- 飯店業

- 飯店

- 餐廳

- 醫療設施

- 教育機構

- 工業建築

- 其他

第7章 市場估價與預測:依建築類型分類,2022-2035年

- 黏合結構

- 浮動的

- 釘子和訂書釘

- 點選鎖定

第8章 市場估算與預測:依通路分類,2022-2035年

- 離線

- 超級市場

- 專賣店

- 其他(百貨公司等)

- 線上

- 電子商務

- 品牌官方網站

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Armstrong Flooring

- Beaulieu International Group

- Congoleum

- Forbo Holding AG

- Gerflor Group

- Interface

- Karndean Designflooring

- Mannington Mills

- Mohawk Industries

- NOX

- Parador GmbH

- Polyflor

- Quick-Step Flooring

- Shaw Industries

- Tarkett

The Global Hard Surface Flooring Market was valued at USD 5.5 billion in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 8.5 billion by 2035.

Urbanization and rapid development worldwide are driving strong demand for durable and low-maintenance flooring solutions across both residential and commercial sectors. Rising construction activity, especially in Asia-Pacific, Africa, Latin America, and other emerging regions, has created a growing need for materials such as vinyl, laminate, ceramic, and engineered wood. Government initiatives to promote affordable housing and smart city projects are further accelerating adoption, as newly developed buildings increasingly utilize hard surface flooring. Consumers' rising disposable income is also encouraging investment in premium, long-lasting flooring options. With durability, aesthetics, and ease of maintenance at the forefront, hard surface flooring is becoming an essential component in modern building projects. Demand is also fueled by commercial spaces, including offices, retail establishments, and hospitality venues, where long-term performance and design appeal are key priorities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.5 Billion |

| Forecast Value | $8.5 Billion |

| CAGR | 4.4% |

The vinyl flooring segment generated USD 1.4 billion in 2025. Its popularity stems from affordability, versatility, and durability, with products manufactured from synthetic polyvinyl chloride (PVC) that resists moisture and wear. Vinyl flooring is available in multiple formats, such as sheets, tiles, and luxury vinyl planks (LVP), offering options suitable for both residential and commercial applications. Advanced printing technology allows vinyl to mimic the appearance of wood or stone, providing a cost-effective alternative to premium materials.

The glue-down installation method held 35.8% share in 2025. This method involves adhering flooring directly to the subfloor using strong adhesives, resulting in a stable and long-lasting bond that reduces movement over time. Glue-down installation is preferred for both commercial and residential applications where durability and performance are critical.

U.S. Hard Surface Flooring Market held 64.4% share, generating USD 911.1 million in 2025. Demand is driven by the growing popularity of luxury vinyl tiles, engineered wood, and laminate flooring. Residential renovations and remodeling are major contributors, while commercial spaces are increasingly choosing hard-wearing flooring solutions. Consumers are placing greater importance on environmentally sustainable products and stylish designs, emphasizing both functionality and aesthetics.

Key players in the Global Hard Surface Flooring Market include Shaw Industries, Polyflor, Quick-Step Flooring, Karndean Designflooring, Tarkett, Interface, Armstrong Flooring, Beaulieu International Group, Congoleum, Forbo Holding AG, Gerflor Group, Mannington Mills, Mohawk Industries, NOX, and Parador GmbH. Companies in the Hard Surface Flooring Market are strengthening their positions through innovation, product diversification, and strategic expansion. Strategies include introducing eco-friendly and sustainable flooring options, enhancing durability and design appeal, and offering a wide range of vinyl, laminate, ceramic, and engineered wood solutions. Firms are investing in R&D to develop high-performance, low-maintenance products and adopting advanced printing and manufacturing technologies to meet changing consumer preferences. Partnerships with construction companies, real estate developers, and distributors expand market reach, while digital marketing and direct-to-consumer sales channels increase brand visibility and accessibility across global markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Installation type

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid urbanization & construction boom

- 3.2.1.2 Surging disposable incomes & renovation trends

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Raw material price volatility

- 3.2.2.2 Cost and complexity of installation

- 3.2.3 Opportunities

- 3.2.3.1 Eco-friendly and bio-based solutions

- 3.2.3.2 Smart, performance-enhanced flooring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Square Ft.)

- 5.1 Key trends

- 5.2 Vinyl flooring

- 5.3 Laminate flooring

- 5.4 Hardwood flooring

- 5.5 Ceramic tiles

- 5.6 Porcelain tiles

- 5.7 Natural stone flooring

- 5.8 Concrete flooring

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Square Ft.)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.3.1 Offices

- 6.3.2 Retail spaces

- 6.3.3 Hospitality

- 6.3.4 Hotels

- 6.3.5 Restaurants

- 6.3.6 Healthcare facilities

- 6.3.7 Education institutions

- 6.3.8 Industrial buildings

- 6.3.9 Others

Chapter 7 Market Estimates and Forecast, By Installation Type, 2022 - 2035 (USD Billion) (Square Ft.)

- 7.1 Key trends

- 7.2 Glue-down

- 7.3 Floating

- 7.4 Nail/staple

- 7.5 Click-lock

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Square Ft.)

- 8.1 Key trends

- 8.2 Offline

- 8.2.1 Supermarkets

- 8.2.2 Specialty stores

- 8.2.3 Others (Departmental stores, etc.)

- 8.3 Online

- 8.3.1 E-commerce

- 8.3.2 Brand websites

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Square Ft.)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Armstrong Flooring

- 10.2 Beaulieu International Group

- 10.3 Congoleum

- 10.4 Forbo Holding AG

- 10.5 Gerflor Group

- 10.6 Interface

- 10.7 Karndean Designflooring

- 10.8 Mannington Mills

- 10.9 Mohawk Industries

- 10.10 NOX

- 10.11 Parador GmbH

- 10.12 Polyflor

- 10.13 Quick-Step Flooring

- 10.14 Shaw Industries

- 10.15 Tarkett

玻璃纖維地板材料市場:2026-2032年全球市場預測(依樹脂類型、安裝方法、價格範圍、終端用戶產業、應用和分銷管道分類)軟木地板材料市場:依產品類型、表面處理類型、厚度、安裝方式、通路和最終用途分類-2026-2032年全球預測

玻璃纖維地板材料市場:2026-2032年全球市場預測(依樹脂類型、安裝方法、價格範圍、終端用戶產業、應用和分銷管道分類)軟木地板材料市場:依產品類型、表面處理類型、厚度、安裝方式、通路和最終用途分類-2026-2032年全球預測 地板材料市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、材質、安裝方法及最終使用者分類

地板材料市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、材質、安裝方法及最終使用者分類 全球夾層樓市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球夾層樓市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球實木地板市場報告

2026年全球實木地板市場報告 地板材料市場-全球產業規模、佔有率、趨勢、機會和預測:按地板材料系統、材料、類型、應用、地區和競爭格局分類,2021-2031年室內地板材料市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、建築類型、最終用戶、地區和競爭格局分類,2021-2031年)建築地板材料市場-全球產業規模、佔有率、趨勢、機會和預測:按最終用戶、印刷技術、材料、地區和競爭格局分類,2021-2031年戶外地板材料市場-全球產業規模、佔有率、趨勢、機會、預測:依材料類型、類型、最終用途、地區和競爭格局分類,2021-2031年水泥基地地板材料市場-全球產業規模、佔有率、趨勢、機會及預測(按應用、最終用戶、地區及競爭格局分類,2021-2031年)

地板材料市場-全球產業規模、佔有率、趨勢、機會和預測:按地板材料系統、材料、類型、應用、地區和競爭格局分類,2021-2031年室內地板材料市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、建築類型、最終用戶、地區和競爭格局分類,2021-2031年)建築地板材料市場-全球產業規模、佔有率、趨勢、機會和預測:按最終用戶、印刷技術、材料、地區和競爭格局分類,2021-2031年戶外地板材料市場-全球產業規模、佔有率、趨勢、機會、預測:依材料類型、類型、最終用途、地區和競爭格局分類,2021-2031年水泥基地地板材料市場-全球產業規模、佔有率、趨勢、機會及預測(按應用、最終用戶、地區及競爭格局分類,2021-2031年)