|

市場調查報告書

商品編碼

1982294

固定式燃料電池市場機會、成長要素、產業趨勢分析及2026-2035年預測。Stationary Fuel Cell Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

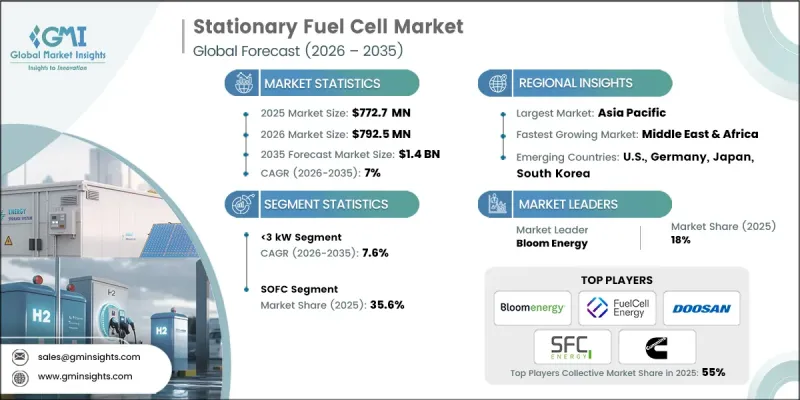

預計到 2025 年,全球固定式燃料電池市場價值將達到 7.727 億美元,年複合成長率為 7%,到 2035 年將達到 14 億美元。

市場成長的驅動力來自氫能基礎設施投資的加速、對高彈性分散式電力系統需求的不斷成長以及全球脫碳政策的支持。固定式燃料電池正逐漸成為住宅、商業和工業領域清潔、可靠、高效現場發電的核心技術。這些系統透過電化學過程將氫氣或含氫燃料轉化為電能和熱能,與傳統的石化燃料發電機相比,顯著降低了排放。人們對電網可靠性的日益關注、不斷上漲的電價以及更嚴格的碳減排目標,正促使公用事業公司、企業和家庭轉向分散式能源解決方案。電堆耐久性、效率、模組化系統設計和成本最佳化的技術進步,進一步推動了市場應用。此外,政府的獎勵、清潔氫能組合標準以及可再生能源併網計畫等舉措,也正在加速已開發市場和新興市場對固定式燃料電池的採用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 7.727億美元 |

| 預計金額 | 14億美元 |

| 複合年成長率 | 7% |

質子交換膜燃料電池(PEMFC)市場預計到2035年將以7%的複合年成長率成長,這主要得益於其高功率密度、低動作溫度和快速啟動能力。 PEMFC系統通常在100 度C以下的溫度下運行,因此反應時間較短,非常適合住宅、商業和小規模分散式發電應用。其緊湊的設計、模組化配置以及與氫氣作為主要燃料的兼容性,使其成為分散式能源發電和備用電源系統的理想解決方案。

預計到2025年,3kW燃料電池的市佔率將達到35.5%,並在2035年之前以7.6%的複合年成長率成長。對小規模電力解決方案日益成長的需求正強勁推動著3kW以下燃料電池的普及,尤其是在住宅和攜帶式備用電源應用領域。住宅正在尋求兼具能源獨立性、永續性和可靠性的系統,促使企業專注於緊湊且高效的解決方案。這些燃料電池因其面積小、運行噪音低以及可與太陽能發電系統無縫整合等優點,在分散式發電領域極具吸引力。此外,它們還能在運作期間提供可靠的能源來源,滿足家庭和小規模企業的關鍵用電需求。

預計2035年,亞太地區的固定式燃料電池市場規模將達11億美元。該地區的主導地位得益於強力的政策支持、大規模的氫能發展藍圖以及日本和韓國的早期商業化努力。政府推出的清潔氫能相關法規、智慧電網基礎設施的擴建以及對可再生能源併網的投資,進一步鞏固了該地區的競爭優勢。此外,快速的工業化進程、不斷成長的電力需求以及日益嚴重的電網不穩定性,正在加速全部區域分散式發電的普及。在北美和歐洲,氫能發展也穩步推進,這主要得益於氫能資助計畫、脫碳目標以及資料中心、醫院和電信設施等關鍵基礎設施中柴油備用電源系統的替代。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系統

- 原物料供應及採購分析

- 生產能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 成本結構分析

- 價格趨勢分析

- 按產能

- 波特的分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTEL 分析

- 新機會和趨勢

- 數位化和物聯網整合

- 進入新興市場

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 公司區域市佔率

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 戰略儀錶板

- 策略舉措

- 競爭性標竿分析

- 創新與科技趨勢

第5章 市場規模及預測:依技術分類,2022-2035年

- PEMFC

- SOFC

- PAFC

- MCFC

- DMFC

- 其他

第6章 市場規模與預測:依產能分類,2022-2035年

- 小於3千瓦

- 3 kW~10 kW

- 10 kW~50 kW

- >50 kW~200 kW

- 200~500 kW

- 500千瓦至1兆瓦

- 超過1兆瓦

第7章 市場規模及預測:依最終用途分類,2022-2035年

- 住宅

- 商業的

- 工業和公共產業

- 資料中心

- 半導體

- 微電網和分散式能源系統(DES)

- 物流倉庫

- 飛機場

- 醫院

- 溝通

- 運輸

- 其他

第8章 市場規模及預測:依應用領域分類,2022-2035年

- 主電源

- 備用/應急

- CHP

- 偏遠/離網

- 其他

第9章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 奧地利

- 亞太地區

- 日本

- 韓國

- 中國

- 印度

- 菲律賓

- 越南

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 拉丁美洲

- 巴西

- 秘魯

- 墨西哥

第10章:公司簡介

- AFC Energy

- Aris Renewable Energy

- Ballard Power Systems

- Bloom Energy

- Ceres Power Holding

- Cummins

- Denso Corporation

- Doosan Fuel Cell

- FuelCell Energy

- Fuji Electric

- GenCell

- Honda Motor

- Horizon Fuel Cell Technologies

- Mitsubishi Heavy Industries

- Nuvera Fuel Cells

- Panasonic Holding Corporation

- Plug Power

- Poscoenergy

- SFC Energy

- Siemens Energy

- Toshiba Corporation

The Global Stationary Fuel Cell Market was valued at USD 772.7 million in 2025 and is estimated to grow at a CAGR of 7% to reach USD 1.4 billion by 2035.

Market growth is driven by accelerating investments in hydrogen infrastructure, increasing demand for resilient distributed power systems, and supportive decarbonization policies worldwide. Stationary fuel cells are emerging as a cornerstone technology for clean, reliable, and high-efficiency onsite power generation across residential, commercial, and industrial applications. These systems convert hydrogen or hydrogen-rich fuels into electricity and heat through electrochemical processes, offering significantly lower emissions compared to conventional fossil-fuel-based generators. Growing concerns over grid reliability, rising electricity prices, and stricter carbon reduction targets are pushing utilities, enterprises, and households toward decentralized energy solutions. Technological advancements in stack durability, efficiency improvements, modular system designs, and cost optimization are further strengthening market adoption. In addition, favorable government incentives, clean hydrogen portfolio standards, and renewable energy integration initiatives are accelerating deployments across developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $772.7 Million |

| Forecast Value | $1.4 Billion |

| CAGR | 7% |

The PEMFC (Proton Exchange Membrane Fuel Cell) segment is anticipated to grow at a CAGR of 7% through 2035, driven by its high-power density, low operating temperature, and rapid start-up capabilities. PEMFC systems typically operate at temperatures below 100°C, enabling faster response times and making them highly suitable for residential, commercial, and small-scale distributed power applications. Their compact design, modular configuration, and compatibility with hydrogen as a primary fuel source position them as an ideal solution for decentralized energy generation and backup power systems.

The 3 kW segment accounted for 35.5% share in 2025 and is projected to grow at a CAGR of 7.6% through 2035. The increasing demand for small-scale power solutions is driving strong adoption of fuel cells under 3 kW, especially for residential use and portable backup power applications. Homeowners are seeking systems that offer energy independence, sustainability, and reliability, prompting businesses to focus on compact and efficient solutions. These fuel cells are particularly appealing due to their small footprint, low operational noise, and seamless integration with solar photovoltaic systems, making them ideal for decentralized power generation. Additionally, they provide a dependable energy source during outages, supporting critical household or small business needs.

Asia Pacific Stationary Fuel Cell Market is expected to reach USD 1.1 billion by 2035. The region's leadership is attributed to strong policy support, large-scale hydrogen roadmaps, and early commercialization efforts in Japan and South Korea. Government mandates promoting clean hydrogen, expansion of smart grid infrastructure, and investments in renewable integration are reinforcing the region's competitive advantage. In addition, rapid industrialization, rising electricity demand, and increasing vulnerability to grid instability are accelerating distributed generation adoption across Asia Pacific. North America and Europe also continue to witness steady deployment, supported by hydrogen funding programs, decarbonization targets, and increasing replacement of diesel backup systems in critical infrastructure such as data centers, hospitals, and telecommunications facilities.

Key players operating in the Global Stationary Fuel Cell Market include Ballard Power Systems, Bloom Energy, Cummins Inc., DENSO Corporation, FuelCell Energy, Plug Power, Toshiba Corporation, SFC Energy AG, Fuji Electric Co., Ltd., and POSCO Energy. Companies in the Stationary Fuel Cell Market are strengthening their foothold through strategic partnerships, product innovation, and hydrogen ecosystem development. Leading players are investing in advanced solid oxide and proton exchange membrane technologies to enhance efficiency, durability, and scalability. Many firms are entering long-term supply agreements and power purchase contracts to secure recurring revenue streams. Expansion into green hydrogen production and electrolyzer integration is enabling vertically integrated solutions. Strategic collaborations with utilities, industrial operators, and government bodies are accelerating project deployments. Companies are also focusing on modular designs that allow flexible capacity expansion, improving cost competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.3.1 Key trends for market estimates

- 1.3.1.1 Quantified market impact analysis

- 1.3.1.2 Mathematical impact of growth parameters on forecast

- 1.3.2 Scenario analysis framework

- 1.3.1 Key trends for market estimates

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360-degree synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Capacity trends

- 2.5 End Use trends

- 2.6 Application trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Cost structure analysis

- 3.6 Price trend analysis

- 3.6.1 By Capacity

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 PEMFC

- 5.3 SOFC

- 5.4 PAFC

- 5.5 MCFC

- 5.6 DMFC

- 5.7 Others

Chapter 6 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 < 3 kW

- 6.3 3 kW - 10 kW

- 6.4 10 kW - 50 kW

- 6.5 > 50 kW-200 KW

- 6.6 >200-500 KW

- 6.7 >500 kW - 1 MW

- 6.8 >1 MW

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industry/Utility

- 7.5 Data Centers

- 7.6 Semiconductors

- 7.7 Microgrid & DES

- 7.8 Logistics warehouse

- 7.9 Airports

- 7.10 Hospitals

- 7.11 Telecommunication

- 7.12 Transport

- 7.13 Others

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MW)

- 8.1 Key trends

- 8.2 Prime Power

- 8.3 Backup/emergency

- 8.4 CHP

- 8.5 Remote/off grid

- 8.6 Others

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Austria

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 South Korea

- 9.4.3 China

- 9.4.4 India

- 9.4.5 Philippines

- 9.4.6 Vietnam

- 9.5 Middle East & Africa

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Peru

- 9.6.3 Mexico

Chapter 10 Company Profiles

- 10.1 AFC Energy

- 10.2 Aris Renewable Energy

- 10.3 Ballard Power Systems

- 10.4 Bloom Energy

- 10.5 Ceres Power Holding

- 10.6 Cummins

- 10.7 Denso Corporation

- 10.8 Doosan Fuel Cell

- 10.9 FuelCell Energy

- 10.10 Fuji Electric

- 10.11 GenCell

- 10.12 Honda Motor

- 10.13 Horizon Fuel Cell Technologies

- 10.14 Mitsubishi Heavy Industries

- 10.15 Nuvera Fuel Cells

- 10.16 Panasonic Holding Corporation

- 10.17 Plug Power

- 10.18 Poscoenergy

- 10.19 SFC Energy

- 10.20 Siemens Energy

- 10.21 Toshiba Corporation

2034年固定式燃料電池市場預測-全球分析(依燃料電池類型、燃料類型、電力、安裝配置、電堆配置、應用、最終用戶、所有權、銷售管道和地區分類)

2034年固定式燃料電池市場預測-全球分析(依燃料電池類型、燃料類型、電力、安裝配置、電堆配置、應用、最終用戶、所有權、銷售管道和地區分類) 固定式燃料電池市場:按類型、功率輸出、燃料類型、安裝類型和最終用途分類-2026-2032年全球市場預測氨氫發電廠市場:依技術、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)

固定式燃料電池市場:按類型、功率輸出、燃料類型、安裝類型和最終用途分類-2026-2032年全球市場預測氨氫發電廠市場:依技術、應用、最終用戶和分銷管道分類,全球預測(2026-2032年) 2026年全球固定式燃料電池市場報告

2026年全球固定式燃料電池市場報告 氫燃料電池固定式電源市場規模、佔有率和趨勢分析報告:按產品、組件、系統、最終用途、地區和細分市場預測,2026-2033年

氫燃料電池固定式電源市場規模、佔有率和趨勢分析報告:按產品、組件、系統、最終用途、地區和細分市場預測,2026-2033年 全球高容量固定式燃料電池市場

全球高容量固定式燃料電池市場 固定式燃料電池市場規模、佔有率和成長分析(按產品類型、額定功率、應用和地區)- 產業預測 2025-2032

固定式燃料電池市場規模、佔有率和成長分析(按產品類型、額定功率、應用和地區)- 產業預測 2025-2032 全球固定式燃料電池產業的成長機會

全球固定式燃料電池產業的成長機會