|

市場調查報告書

商品編碼

1982284

聚氨酯隔熱材料市場機會、成長要素、產業趨勢分析及2026-2035年預測。Polyurethane Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

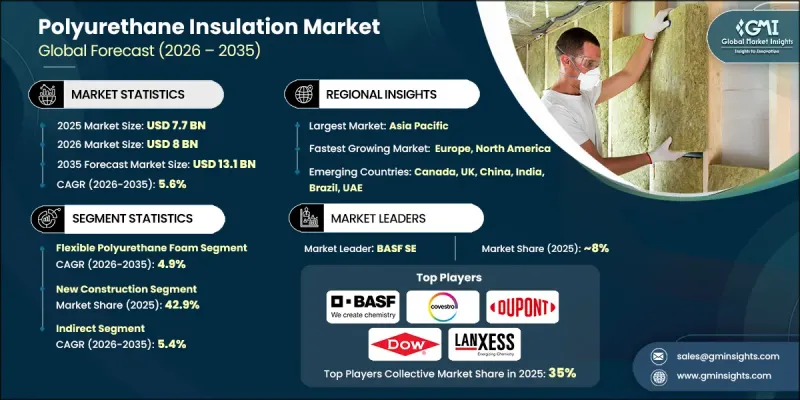

2025年全球聚氨酯隔熱材料市場規模預估為77億美元,預計2035年將以5.6%的複合年成長率成長至131億美元。

聚氨酯隔熱材料產業的成長主要得益於全球日益嚴格的能源效率法規和旨在減少商業及工業基礎設施碳排放的氣候變遷相關法規。監管機構正在加強建築性能標準,並鼓勵開發商採用能夠提高熱效率的先進隔熱材料。同時,向永續建築實踐和節能維修的轉變也加速了該產品的普及。建築商優先考慮能夠降低長期能耗和環境影響的保溫解決方案,而聚氨酯隔熱材料已成為新建和維修計劃的首選材料。冷藏倉儲基礎設施和溫控物流網路的擴張也推動了市場需求,因為處理生鮮產品和溫度敏感產品的行業需要高性能隔熱材料來維持營運效率。聚氨酯隔熱材料憑藉其卓越的隔熱性能、耐久性和能源效率,持續受到青睞,並在多個終端應用行業中保持穩定的市場成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 77億美元 |

| 預計金額 | 131億美元 |

| 複合年成長率 | 5.6% |

預計2025年至2035年間,柔軟性聚氨酯泡棉市場將以4.9%的複合年成長率成長。該細分市場的需求不斷成長,主要得益於其適應性強、結構輕巧以及在廣泛應用領域中展現出的卓越性能。其緩衝性、回彈性和提升舒適度的特性使其成為多個製造業的首選材料。消費者對更舒適、耐用和符合人體工學性能的產品日益成長的需求,也推動了該細分市場在更廣泛的聚氨酯隔熱材料市場中的穩步成長。

預計到2025年,新建建築市場將佔據42.9%的市場佔有率,並在2026年至2035年間以5.8%的複合年成長率成長。快速的城市擴張、持續的基礎設施投資以及日益嚴格的建築能源效率標準正在鞏固這一市場的主導地位。開發商正在將高效的隔熱系統應用於現代建築,以滿足監管標準並提升建築的長期營運性能。人們對永續城市規劃和節能設計的日益關注,也持續推動對聚氨酯隔熱材料的強勁需求。

美國聚氨酯隔熱材料市場預計到2025年將達到16億美元,並在2026年至2035年間以5.1%的複合年成長率成長。永續建設活動、促進能源效率的健全法規結構以及環保建築標準的廣泛應用,都為美國市場的擴張提供了支撐。為了滿足不斷變化的建築需求並降低營運能源成本,住宅、商業和工業領域對隔熱材料維修的投資都在增加。現有建築的持續現代化改造、技術的進步以及人們對經濟高效的保溫解決方案日益成長的認知,進一步鞏固了美國在該領域的主導地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 嚴格的能源效率法規和氣候目標

- 對永續建築和建築維修的需求日益成長

- 低溫運輸物流和冷凍/冷藏行業的擴張

- 產業潛在風險與挑戰

- 嚴格的化學品使用環境法規

- 原物料價格波動

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 硬質聚氨酯泡棉板

- 聚氨酯泡沫塗料(SPF)

- 聚異氰酸酯(PIR)板

- 軟性聚氨酯泡棉

第6章 市場估價與預測:依安裝方式分類,2022-2035年

- 新建工程

- 維修和整修

- 維護/更換

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅建築

- 商業建築

- 工業建築

- 基礎設施

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 屋頂和天花板隔熱材料

- 牆體隔熱材料

- 地板隔熱材料

- 管道隔熱材料

- 冷藏和冷凍

- 儲槽和貨櫃

- 其他(暖通空調、汽車內裝)

第9章 市場估價與預測:依通路分類,2022-2035年

- 直接地

- 間接

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第11章:公司簡介

- Armacell

- BASF SE

- Compagnie de Saint-Gobain SA

- Covestro AG

- Dow Inc.

- DuPont

- Foam Supplies Inc.(FSI)

- FoamPartner

- Gallagher Corporation

- Huntsman Corporation

- IMA Srl

- LANXESS

- Nitto Denko Corporation

- Tosoh Corporation

- Wanhua Chemical Group

The Global Polyurethane Insulation Market was valued at USD 7.7 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 13.1 billion by 2035.

Growth in the polyurethane insulation industry is driven by stricter global energy efficiency mandates and climate-focused regulations aimed at lowering carbon emissions across commercial and industrial infrastructure. Regulatory authorities are reinforcing building performance standards, pushing developers to integrate advanced insulation materials that improve thermal efficiency. At the same time, the shift toward sustainable construction practices and energy-efficient retrofitting is accelerating product adoption. Builders are prioritizing insulation solutions that reduce long-term energy consumption and environmental impact, positioning polyurethane insulation as a preferred material for both newly built structures and renovation projects. Expanding cold storage infrastructure and temperature-controlled logistics networks are also fueling demand, as industries handling perishable and temperature-sensitive goods require high-performance insulation to maintain operational efficiency. Polyurethane insulation continues to gain traction due to its strong thermal resistance, durability, and energy-saving capabilities, supporting consistent market expansion across multiple end-use industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.7 Billion |

| Forecast Value | $13.1 Billion |

| CAGR | 5.6% |

The flexible polyurethane foam segment is forecast to grow at a CAGR of 4.9% from 2025 to 2035. Demand for this segment is increasing due to its adaptability, lightweight structure, and performance efficiency across a broad range of applications. Its cushioning strength, resilience, and comfort-enhancing properties make it a preferred material across several manufacturing sectors. Rising consumer expectations for enhanced comfort, durability, and ergonomic performance are contributing to steady segment growth within the broader polyurethane insulation market.

The new construction segment accounted for 42.9% share in 2025 and is expected to grow at a CAGR of 5.8% between 2026 and 2035. Rapid urban expansion, continued infrastructure investments, and increasingly rigorous building energy codes are reinforcing the dominance of this segment. Developers are integrating high-efficiency insulation systems into modern structures to meet regulatory benchmarks and improve long-term operational performance. The growing emphasis on sustainable urban planning and energy-conscious design continues to create strong demand for polyurethane-based insulation materials.

United States Polyurethane Insulation Market reached USD 1.6 billion in 2025, with projected growth at a CAGR of 5.1% from 2026 to 2035. Market expansion in the country is supported by sustained construction activity, firm regulatory frameworks promoting energy conservation, and widespread adoption of environmentally responsible building standards. Residential, commercial, and industrial sectors are increasing investments in insulation upgrades to align with evolving building requirements and reduce operational energy costs. Continued modernization of existing properties, technological advancements, and heightened awareness of cost-efficient insulation solutions further reinforce the country's leadership position.

Key companies operating in the Global Polyurethane Insulation Market include Armacell, BASF SE, Compagnie de Saint-Gobain SA, Covestro AG, Dow Inc., DuPont, Foam Supplies Inc. (FSI), FoamPartner, Gallagher Corporation, Huntsman Corporation, IMA Srl, LANXESS, Nitto Denko Corporation, Tosoh Corporation, and Wanhua Chemical Group. Companies in the Global Polyurethane Insulation Market are strengthening their market position through capacity expansion, product innovation, and strategic collaborations. Manufacturers are investing in research and development to enhance thermal performance, improve fire resistance, and develop environmentally compliant formulations that align with evolving regulatory standards. Strategic mergers, acquisitions, and joint ventures are being pursued to expand geographic reach and diversify product portfolios. Many players are also focusing on backward integration and supply chain optimization to secure raw material availability and control production costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Installation method

- 2.2.4 Application

- 2.2.5 End-user

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent energy efficiency regulations and climate goals

- 3.2.1.2 Rising demand for sustainable construction and building renovation

- 3.2.1.3 Expansion of cold chain logistics and refrigeration sector

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Stringent Environmental Regulations on Chemical Use

- 3.2.2.2 Volatility in raw material prices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation Landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion)

- 5.1 Key trends

- 5.2 Rigid polyurethane foam boards

- 5.3 Spray polyurethane foam (SPF)

- 5.4 Polyisocyanurate (PIR) boards

- 5.5 Flexible polyurethane foam

Chapter 6 Market Estimates & Forecast, By Installation Method, 2022 - 2035, (USD Billion)

- 6.1 Key trends

- 6.2 New construction

- 6.3 Retrofit/Renovation

- 6.4 Maintenance & replacement

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion)

- 7.1 Key trends

- 7.2 Residential buildings

- 7.3 Commercial buildings

- 7.4 Industrial buildings

- 7.5 Infrastructure

Chapter 8 Market Estimates & Forecast, By End-User, 2022 - 2035, (USD Billion)

- 8.1 Key trends

- 8.2 Roof & ceiling insulation

- 8.3 Wall insulation

- 8.4 Floor insulation

- 8.5 Pipe insulation

- 8.6 Cold storage & refrigeration

- 8.7 Tank & vessels

- 8.8 Others (HVAC, automotive interiors)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Armacell

- 11.2 BASF SE

- 11.3 Compagnie de Saint-Gobain SA

- 11.4 Covestro AG

- 11.5 Dow Inc.

- 11.6 DuPont

- 11.7 Foam Supplies Inc. (FSI)

- 11.8 FoamPartner

- 11.9 Gallagher Corporation

- 11.10 Huntsman Corporation

- 11.11 IMA Srl

- 11.12 LANXESS

- 11.13 Nitto Denko Corporation

- 11.14 Tosoh Corporation

- 11.15 Wanhua Chemical Group

發泡隔熱材料市場:全球市場預測,2026-2032年

發泡隔熱材料市場:全球市場預測,2026-2032年 2026年Icynene噴塗泡沫保溫材料全球市場報告2026年全球噴塗泡沫保溫材料市場報告

2026年Icynene噴塗泡沫保溫材料全球市場報告2026年全球噴塗泡沫保溫材料市場報告 發泡隔熱材料:全球市場牆體隔熱材料市場:依材料類型、形式、應用、最終用途及通路分類,全球預測(2026-2032)

發泡隔熱材料:全球市場牆體隔熱材料市場:依材料類型、形式、應用、最終用途及通路分類,全球預測(2026-2032) 生物基保溫泡棉市場分析及預測(至2035年):依類型、產品、應用、材料種類、技術、最終使用者、形態、功能、安裝類型及製程分類發泡隔熱材料市場分析及預測(至2035年):類型、產品類型、應用、技術、材質類型、最終用戶、安裝類型、功能、工藝

生物基保溫泡棉市場分析及預測(至2035年):依類型、產品、應用、材料種類、技術、最終使用者、形態、功能、安裝類型及製程分類發泡隔熱材料市場分析及預測(至2035年):類型、產品類型、應用、技術、材質類型、最終用戶、安裝類型、功能、工藝 全球噴塗聚氨酯泡棉市場規模、佔有率、趨勢和成長分析報告(2026-2034)鋁箔隔熱材料市場按產品類型、厚度、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測

全球噴塗聚氨酯泡棉市場規模、佔有率、趨勢和成長分析報告(2026-2034)鋁箔隔熱材料市場按產品類型、厚度、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測 發泡隔熱材料市場規模、佔有率及成長分析(按形態、產品類型、最終用途產業及地區分類)-2026-2033年產業預測

發泡隔熱材料市場規模、佔有率及成長分析(按形態、產品類型、最終用途產業及地區分類)-2026-2033年產業預測