|

市場調查報告書

商品編碼

1982278

自動化市場預分析:成長機會、成長要素、產業趨勢以及 2026-2035 年預測。Pre Analytical Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

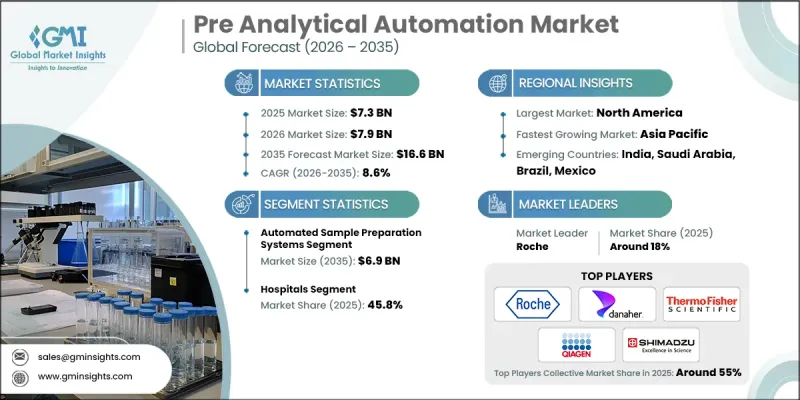

2025 年全球預檢自動化市場價值為 73 億美元,預計到 2035 年將以 8.6% 的複合年成長率成長至 166 億美元。

市場成長主要受診斷檢測數量穩定增加、檢查室自動化需求不斷成長以及為實現快速出具檢測結果而加大對先進檢測設備的資本投入所驅動。全球臨床檢查室面臨著在保持準確性和品質標準的同時提高營運效率的壓力。由於早期疾病檢測的努力以及慢性病和急性疾病負擔的日益加重,每日檢測量顯著增加。為了應對當前和預期的工作量,檢查室正在加速數位轉型,並在其營運架構中部署互聯的自動化平台。現代化的檢體自動化系統簡化了檢體處理流程,提高了工作流程的連續性,並減少了人工干預。這些解決方案支援提高處理能力、最佳化檢體路徑、優先處理緊急病例以及加快處理速度,而無需相應增加人員配備,從而提升了檢查室的整體生產力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 73億美元 |

| 預計金額 | 166億美元 |

| 複合年成長率 | 8.6% |

到2025年,自動化樣品製備系統市佔率將達到39.5%。對快速檢測結果的需求持續推動著處理複雜、高通量檢測的實驗室採用自動化系統。自動化系統透過標準化和可程式設計的工作流程執行必要的預處理任務,從而簡化了複雜的分析前流程。這些平台最大限度地減少了人工操作,降低了人為錯誤的風險,並提高了檢測的一致性和操作準確性。採用先進檢測通訊協定的檢查室越來越依賴自動化樣品製備技術來維持效率、可重複性和品管。

到2025年,醫院領域將佔據45.8%的市場。隨著醫院檢查室診斷工作量的不斷成長,醫療機構正在推進關鍵分析前階段的自動化,以保持效率和準確性。大規模醫療機構由於需要處理大量的住院和門診病人,正在實施自動化,以保持最佳的檢測響應時間並減輕員工的工作負擔。整合分析前功能的綜合自動化生產線正在提升操作標準化程度,並最大限度地減少檢體處理過程中的差異。醫院檢查室採用自動化有助於及時報告、加強品質保證措施並減少對人工操作的依賴。

到2025年,北美實驗室前自動化市佔率將達到38.6%。這一成長主要得益於診斷需求的不斷成長,以及大中型醫療機構在研究、基礎設施和檢查室現代化方面的大量投資。對高通量檢測能力、先進分子診斷和人工智慧驅動的檢測系統日益成長的需求,鞏固了該地區的主導地位。隨著旨在簡化工作流程和提高分析準確性的技術不斷應用,北美將繼續引領檢查室自動化創新。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 檢查室自動化的需求日益成長

- 臨床診斷中進行的檢測數量增加

- 增加對臨床檢查室的投資,以加快檢測結果出爐速度

- 產業潛在風險與挑戰

- 高昂的資本成本和實施成本

- 與現有LIS系統整合面臨的挑戰

- 機會

- 新興市場自動化擴張

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 歐洲

- 亞太地區

- 技術與創新趨勢(基於初步調查)

- 當前技術趨勢

- 新興技術

- 消費者洞察

- 自動化預處理 - 解決方案架構概述

- 供應鏈分析

- 投資環境

- 波特五力分析

- PESTEL 分析

- 差距分析

- 未來市場趨勢(基於初步研究)

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 自動化樣品製備系統

- 自動化樣品處理系統

- 自動化樣品分類系統

- 自動化樣品儲存系統

- 其他產品類型

第6章 市場估算與預測:依最終用途分類,2022-2035年

- 醫院

- 臨床檢查室

- 研究機構

- 其他最終用戶

第7章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- Abbott

- Beckman Coulter(Danaher Corporation)

- Becton, Dickinson and Company

- Copan Diagnostics

- Greiner Bio-One

- HAMILTON

- Inpeco

- QIAGEN

- Roche

- SARSTEDT

- SHIMADZU

- SIEMENS Healthineers

- Sysmex

- TECAN

- Thermo Fisher SCIENTIFIC

The Global Pre Analytical Automation Market was valued at USD 7.3 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 16.6 billion by 2035.

Market growth is propelled by the steady rise in diagnostic test volumes, increasing demand for laboratory automation, and growing capital investments in advanced laboratory instrumentation aimed at accelerating result delivery. Clinical laboratories worldwide are under mounting pressure to enhance operational efficiency while maintaining accuracy and quality standards. The push for early disease detection, coupled with the rising burden of chronic and acute health conditions, has significantly increased the number of tests processed daily. To manage current and anticipated workloads, laboratories are accelerating digital transformation initiatives and implementing interconnected automation platforms within their operational frameworks. Modern pre-analytical automation systems streamline sample handling processes, improve workflow continuity, and reduce manual intervention. These solutions support higher throughput capacity, optimize sample routing, prioritize urgent cases, and enhance processing speed without proportionally increasing staffing requirements, thereby strengthening overall laboratory productivity.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.3 Billion |

| Forecast Value | $16.6 Billion |

| CAGR | 8.6% |

The automated sample preparation systems segment captured a 39.5% share in 2025. The demand for faster turnaround times continues to drive adoption across laboratories handling complex and high-volume testing environments. Automated systems simplify intricate pre-analytical procedures by executing essential preparation tasks through standardized and programmable workflows. By minimizing manual handling and reducing the risk of human error, these platforms enhance consistency and operational precision. Laboratories managing sophisticated testing protocols increasingly rely on automated sample preparation technologies to maintain efficiency, reproducibility, and quality control.

The hospitals segment accounted for 45.8% share in 2025. Rising diagnostic workloads within hospital-based laboratories are prompting institutions to automate key pre-analytical stages to preserve efficiency and accuracy. Large healthcare facilities processing high inpatient and outpatient volumes are integrating automation to sustain optimal turnaround times and alleviate workforce strain. Comprehensive automation lines that unify pre-analytical functions have strengthened operational standardization and minimized variability in sample processing. Automation deployment in hospital laboratories contributes to timely reporting, reinforced quality assurance measures, and reduced reliance on manual processes.

North America Pre Analytical Automation Market held a 38.6% share in 2025. The region's growth is supported by rising diagnostic demand and substantial investments in research, infrastructure, and laboratory modernization by both large-scale and mid-sized healthcare institutions. The increasing need for high-throughput testing capabilities, advanced molecular diagnostics, and AI-enhanced laboratory systems is reinforcing regional leadership. Ongoing technological adoption aimed at improving workflow efficiency and analytical accuracy continues to position North America at the forefront of laboratory automation innovation.

Key companies operating in the Global Pre Analytical Automation Market include Roche, Beckman Coulter (Danaher Corporation), Abbott, SIEMENS Healthineers, Thermo Fisher SCIENTIFIC, Becton Dickinson and Company, QIAGEN, Sysmex, HAMILTON, TECAN, SHIMADZU, SARSTEDT, Inpeco, Copan Diagnostics, and Greiner Bio-One. Companies in the Global Pre Analytical Automation Market are reinforcing their competitive positions through sustained investment in innovation, strategic collaborations, and global expansion initiatives. Market leaders are prioritizing the development of integrated and scalable automation platforms designed to accommodate rising test volumes and evolving laboratory requirements. Partnerships with healthcare institutions and diagnostic networks are enhancing system interoperability and long-term service contracts. Organizations are also incorporating artificial intelligence and advanced data analytics to optimize workflow management and predictive maintenance capabilities. Expansion into emerging healthcare markets and strengthening regional distribution networks remain key growth strategies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for laboratory automation

- 3.2.1.2 Increasing test volumes in clinical diagnostics

- 3.2.1.3 Growing investments in clinical laboratories for faster turnaround times

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital and installation costs

- 3.2.2.2 Integration challenges with existing LIS systems

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of automation in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Consumer insights

- 3.7 Pre analytical automation - Solution Architecture overview

- 3.8 Supply chain analysis

- 3.9 Investment landscape

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Automated sample preparation systems

- 5.3 Automated sample transport systems

- 5.4 Automated sample sorting systems

- 5.5 Automated sample storage systems

- 5.6 Other product types

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Clinical laboratories

- 6.4 Research institutes

- 6.5 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott

- 8.2 Beckman Coulter (Danaher Corporation)

- 8.3 Becton, Dickinson and Company

- 8.4 Copan Diagnostics

- 8.5 Greiner Bio-One

- 8.6 HAMILTON

- 8.7 Inpeco

- 8.8 QIAGEN

- 8.9 Roche

- 8.10 SARSTEDT

- 8.11 SHIMADZU

- 8.12 SIEMENS Healthineers

- 8.13 Sysmex

- 8.14 TECAN

- 8.15 Thermo Fisher SCIENTIFIC

實驗室自動化市場:按類型、交付方式、部署方式、應用程式和最終用戶分類-2026-2032年全球市場預測

實驗室自動化市場:按類型、交付方式、部署方式、應用程式和最終用戶分類-2026-2032年全球市場預測 2026年全球藥物研發實驗室自動化市場報告2026年全球實驗室自動化系統市場報告

2026年全球藥物研發實驗室自動化市場報告2026年全球實驗室自動化系統市場報告 基因組學實驗室自動化市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、流程、設備和解決方案分類實驗室桌上型自動化市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終使用者、流程及部署類型分類實驗室自動化市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、最終使用者、功能、設備分類生物分析實驗室自動化市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、流程、設備和解決方案分類

基因組學實驗室自動化市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、流程、設備和解決方案分類實驗室桌上型自動化市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終使用者、流程及部署類型分類實驗室自動化市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、最終使用者、功能、設備分類生物分析實驗室自動化市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、流程、設備和解決方案分類 全球實驗室自動化系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球實驗室自動化系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本實驗室自動化市場規模、佔有率、趨勢及預測(按類型、設備/軟體、最終用戶和地區分類),2026-2034年實驗室自動化市場-2026-2031年預測

日本實驗室自動化市場規模、佔有率、趨勢及預測(按類型、設備/軟體、最終用戶和地區分類),2026-2034年實驗室自動化市場-2026-2031年預測