|

市場調查報告書

商品編碼

1982276

2026 年至 2035 年住宅照明市場的商業機會、成長要素、產業趨勢與預測。Residential Lighting Fixtures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

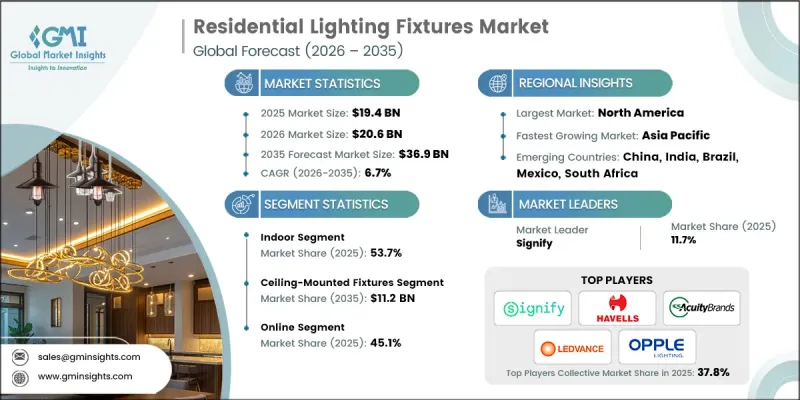

全球住宅照明市場預計到 2025 年價值 194 億美元,預計到 2035 年將達到 369 億美元,年複合成長率為 6.7%。

人口快速成長和城市化進程加速,持續推動新建住宅的強勁需求,直接帶動了照明燈具的銷售。傳統螢光和鹵素燈向LED照明解決方案的廣泛轉變,為市場帶來了巨大的成長潛力。消費者擴大選擇LED技術,因為它具有使用壽命長、能源效率高、發熱量低等優點。鼓勵採用節能照明的扶持性監管措施,進一步增強了市場動力。技術創新也正在重塑市場競爭格局,人工智慧(AI)的整合提升了吸頂燈和檯燈的功能性。消費者對智慧家庭、互聯生態系統和身臨其境型零售環境的日益關注,正在推動消費者參與並影響其購買決策。製造商正大力投資研發,以推出差異化、設計導向且節能的解決方案,從而滿足全球市場不斷變化的住宅需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 194億美元 |

| 預計金額 | 369億美元 |

| 複合年成長率 | 6.7% |

到2025年,室內照明市佔率將達到53.7%。消費者對室內照明的偏好日益轉向舒適、個人化和健康型照明。對暖色調照明、基於晝夜節律的照明系統以及多層次照明方案的需求持續成長。具備自動化功能、語音控制和可自訂場景設定的智慧照明解決方案正逐漸成為住宅的主流選擇。與各種智慧家庭助理和物聯網平台的整合正成為消費者購買時的關鍵考量因素,進一步提升了智慧住宅照明系統的吸引力。

預計到2035年,吸頂式照明燈具市場規模將達112億美元。由於其在住宅空間中的多功能性,市場對這類燈具的需求仍然強勁。消費者青睞兼具節能性和視覺美感的精緻簡約設計,這類燈具通常整合LED模組和智慧調光技術。緊湊型模組化住宅設計的日益普及進一步刺激了對纖薄嵌入式吸頂照明解決方案的需求。製造商正優先考慮色溫調節和應用程式控制等功能,以確保與不斷擴展的智慧家庭生態系統相容。

到2025年,北美住宅照明市佔率將達到31.3%。該地區的成長得益於建築美學、先進數位控制系統和智慧住宅基礎設施的融合。照明技術供應商與智慧建築解決方案開發商之間日益密切的合作正在重新定義產品創新。 2025年11月由法蘭克福展覽公司主辦的「北美照明+智慧建築展」的推出,凸顯了產業向融合照明產品、控制技術和連網家庭系統的整合平台轉型。這種整合模式促進了跨產業夥伴關係,並進一步強化了照明在先進住宅環境中的戰略重要性。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球住宅領域LED照明應用日益普及

- 全球人口成長與都市化

- 支持節能照明的法規

- 美學偏好和對現代、可自訂照明設計的需求。

- 住宅照明領域體驗式與高階零售模式的拓展

- 產業潛在風險與挑戰

- 先進智慧住宅照明設備的初始成本較高

- 開發中國家和價格敏感型市場的住宅敏感性

- 市場機遇

- 由於住宅照明基礎設施老化,對維修和更換的需求日益成長。

- 出租住宅和合租空間對標準化照明昇級的需求日益成長。

- 促進因素

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年重大發展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 吸頂式照明燈具

- 吊掛

- 嵌入式照明燈具

- 壁掛式照明燈具

- 其他

第6章 市場估算與預測:依光源分類,2022-2035年

- LED(發光二極體)

- 螢光

- 鹵素

- 白熾燈

第7章 市場估價與預測:依安裝地點分類,2022-2035年

- 室內的

- 戶外的

第8章 市場估算與預測:依通路分類,2022-2035年

- 線上

- 離線

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- Signify

- Acuity Brands

- Havells

- Ledvance GmbH

- 按地區分類的主要企業

- 北美洲

- Cooper Lighting Solutions

- Hubbell Incorporated

- Lutron

- 歐洲

- ERCO

- Louis Poulsen

- Siteco GmbH

- 亞太地區

- Opple Lighting

- NVC Lighting

- Panasonic

- 北美洲

- 特殊玩家/干擾者

- Cree Lighting USA, LLC.

- GE Lighting(Savant Systems)

- Kichler Lighting

- Thorn Lighting(Zumtobel-Group)

- Visual Comfort &Co.

- WAC Lighting

The Global Residential Lighting Fixtures Market was valued at USD 19.4 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 36.9 billion by 2035.

Rapid population growth and accelerating urban development continue to generate strong demand for new residential construction, directly supporting lighting fixture sales. The widespread transition from conventional fluorescent and halogen bulbs to LED lighting solutions is creating substantial growth prospects. Consumers are increasingly choosing LED technology due to its extended lifespan, superior energy efficiency, and minimal heat emission. Supportive regulatory initiatives encouraging energy-efficient lighting adoption are further reinforcing market momentum. Technological innovation is also reshaping the competitive landscape, as artificial intelligence integration enhances the functionality of ceiling and table lighting products. Growing interest in smart homes, connected ecosystems, and immersive retail environments is driving consumer engagement and influencing purchase decisions. Manufacturers are allocating significant investments toward research and development to introduce differentiated, design-focused, and energy-efficient solutions that align with evolving residential preferences across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $19.4 Billion |

| Forecast Value | $36.9 Billion |

| CAGR | 6.7% |

The indoor category accounted for 53.7% share in 2025. Consumer preferences within indoor lighting increasingly emphasize comfort, customization, and wellness-focused illumination. Demand for warm lighting tones, circadian-based systems, and multi-layered lighting arrangements continues to gain traction. Smart lighting solutions equipped with automation features, voice-enabled controls, and customizable scene settings are becoming mainstream choices among homeowners. Integration with broader smart home assistants and Internet of Things platforms is emerging as a critical purchase consideration, strengthening the appeal of connected residential lighting systems.

The ceiling-mounted fixtures segment is forecast to reach USD 11.2 billion by 2035. Demand for these fixtures remains strong due to their versatility across multiple residential spaces. Buyers are gravitating toward sleek, minimalist designs incorporating integrated LED modules and intelligent dimming technologies that enhance both energy efficiency and visual appeal. The growing popularity of compact and modular housing designs is further stimulating demand for slim and flush-mounted ceiling lighting solutions. Manufacturers are prioritizing adjustable color temperature features and app-based controls to ensure compatibility with expanding smart home ecosystems.

North America Residential Lighting Fixtures Market held a 31.3% share in 2025. Regional growth is being shaped by the integration of architectural aesthetics, advanced digital control systems, and intelligent residential infrastructure. Increasing collaboration between lighting technology providers and smart building solution developers is redefining product innovation. The introduction of Light + Intelligent Building North America by Messe Frankfurt in November 2025 highlights the industry's shift toward unified platforms that merge lighting products with control technologies and connected home systems. This integrated approach is encouraging cross-industry partnerships and reinforcing the strategic importance of lighting within advanced residential environments.

Key companies operating in the Global Residential Lighting Fixtures Market include Opple Lighting, Signify, Havells, Acuity Brands, Ledvance GmbH, Kichler Lighting, GE Lighting (Savant Systems), Visual Comfort & Co., and Thorn Lighting (Zumtobel Group). Leading participants in the Residential Lighting Fixtures Market are strengthening their competitive positions through innovation-driven product development, strategic partnerships, and geographic expansion. Companies are investing heavily in research and development to introduce AI-enabled and IoT-compatible lighting systems that align with smart home trends. Many players are expanding their LED portfolios with energy-efficient, design-oriented solutions to address shifting consumer preferences. Collaborations with technology firms and smart ecosystem providers are enhancing product interoperability and market reach. Businesses are also focusing on brand differentiation through premiumization strategies and experiential retail concepts that allow customers to interact with advanced lighting solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Light source trends

- 2.2.3 Installation location trends

- 2.2.4 Distribution channel trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of LEDs in residential sectors across the globe

- 3.2.1.2 Growing population and urbanization across the globe

- 3.2.1.3 Supportive regulations for energy efficient lightings

- 3.2.1.4 Aesthetic preferences and demand for modern, customizable lighting designs

- 3.2.1.5 Expansion of experiential and premium retail formats in residential lighting

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of advanced and smart residential lighting fixtures

- 3.2.2.2 Price sensitivity among residential consumers in developing and cost-conscious markets

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit and replacement demand from aging residential lighting infrastructure

- 3.2.3.2 Growth in rental housing and co-living spaces requiring standardized lighting upgrades

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Ceiling-mounted fixtures

- 5.3 Suspended/hanging fixtures

- 5.4 Recessed fixtures

- 5.5 Wall-mounted fixtures

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Light Source, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Led (light emitting diode)

- 6.3 Fluorescent

- 6.4 Halogen

- 6.5 Incandescent

Chapter 7 Market Estimates and Forecast, By Installation Location, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Indoor

- 7.3 Outdoor

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Online

- 8.3 Offline

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Signify

- 10.1.2 Acuity Brands

- 10.1.3 Havells

- 10.1.4 Ledvance GmbH

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Cooper Lighting Solutions

- 10.2.1.2 Hubbell Incorporated

- 10.2.1.3 Lutron

- 10.2.2 Europe

- 10.2.2.1 ERCO

- 10.2.2.2 Louis Poulsen

- 10.2.2.3 Siteco GmbH

- 10.2.3 APAC

- 10.2.3.1 Opple Lighting

- 10.2.3.2 NVC Lighting

- 10.2.3.3 Panasonic

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Cree Lighting USA, LLC.

- 10.3.2 GE Lighting (Savant Systems)

- 10.3.3 Kichler Lighting

- 10.3.4 Thorn Lighting (Zumtobel-Group)

- 10.3.5 Visual Comfort & Co.

- 10.3.6 WAC Lighting

全球廚房照明市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球住宅照明市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球廚房照明市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球住宅照明市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球廚房照明市場報告

2026年全球廚房照明市場報告 廚房照明市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、通路、最終用戶、地區及競爭格局分類,2021-2031年預測)

廚房照明市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、通路、最終用戶、地區及競爭格局分類,2021-2031年預測) 全球廚房照明市場全球景觀照明市場全球住宅照明市場

全球廚房照明市場全球景觀照明市場全球住宅照明市場 北美戶外甲板照明市場規模、佔有率、趨勢分析報告:按產品、應用、國家和細分市場預測,2025 年至 2033 年

北美戶外甲板照明市場規模、佔有率、趨勢分析報告:按產品、應用、國家和細分市場預測,2025 年至 2033 年 全球戶外露臺照明市場:市場規模、佔有率、趨勢、產業分析(依產品、應用和地區)、未來預測(2025-2034)

全球戶外露臺照明市場:市場規模、佔有率、趨勢、產業分析(依產品、應用和地區)、未來預測(2025-2034) 景觀照明市場按光源、營運和地區分類

景觀照明市場按光源、營運和地區分類