|

市場調查報告書

商品編碼

1982261

資料中心暖通空調市場:成長機會、成長要素、產業趨勢分析及2026-2035年預測Data Center HVAC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

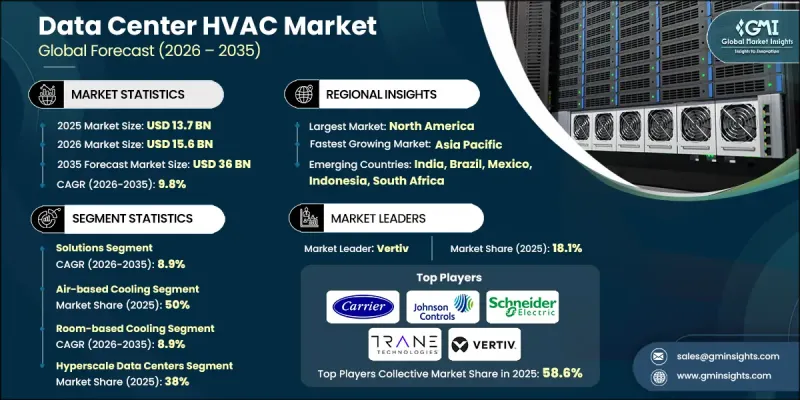

全球資料中心暖通空調市場預計到 2025 年將達到 137 億美元,預計到 2035 年將以 9.8% 的複合年成長率成長至 360 億美元。

全球資料中心暖通空調(HVAC)市場的成長主要受運算強度不斷提高、人工智慧主導工作負載不斷擴展以及超大規模和企業級設施持續發展所驅動。隨著伺服器密度的增加和高效能運算環境熱負荷的不斷成長,先進的冷卻基礎設施對於維持運作穩定性和運作至關重要。整個暖通空調產業的研發工作日益集中於液冷技術和能夠處理高功率密度的新一代溫度控管系統。同時,日益嚴格的能源消耗和環境績效法規迫使營運商提高系統效率並減少碳排放。以環境、社會和治理(ESG)為重點的措施和淨零排放承諾正在推動設施升級,旨在最佳化電源使用效率(PUE)並降低營運成本。基礎設施策略正在透過改善氣流設計、採用永續冷媒以及整合節能冷卻架構進行重組。在持續的監管要求和不斷上漲的能源成本的背景下,資料中心對智慧高效能暖通空調解決方案的需求預計將顯著加速成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 137億美元 |

| 預測金額 | 360億美元 |

| 複合年成長率 | 9.8% |

不斷成長的負載能力、永續發展目標以及監管合規要求,推動了對緊湊型、擴充性且適應性強的暖通空調系統日益成長的需求。產業相關人員正透過設計模組化冷卻平台來滿足這項需求,這些平台能夠最大限度地利用空間,提高能源效率,同時還能在不同地區高效運作。

預計到2025年,解決方案領域將佔據76%的市場佔有率,並在2026年至2035年間以8.9%的複合年成長率成長。由人工智慧(AI)驅動的先進監控工具能夠實現預測性維護、改善氣流管理並降低不必要的電力消耗。液冷技術的日益普及支持高密度伺服器環境,透過節能設計提高可靠性並延長設備使用壽命。

預計到2025年,風冷技術領域將佔50%的市場佔有率,並在2026年至2035年間以8.8%的複合年成長率成長。先進的氣流最佳化系統、變速風扇配置和智慧環境控制可提高熱穩定性並最大限度地減少能源浪費。相容節熱器的設計促進了外部空氣的利用,而模組化冷卻單元則支援超大規模和邊緣運算環境中的擴充性。隨著伺服器功率密度的增加,人們對直接冷卻和浸沒式冷卻方法的興趣日益濃厚,而先進的冷卻液配方則可提高傳熱效率。

預計到2025年,美國資料中心暖通空調(HVAC)市場規模將達到47億美元。日益增強的雲端運算整合和人工智慧密集型應用的興起,正在推動對更高效冷卻架構的需求。電氣化政策和脫碳舉措的投資支持,正在加速智慧暖通空調控制和能源最佳化系統的應用。與智慧建築平台和併網技術的整合,使設施能夠管理尖峰負載、降低需求費用並整合再生能源來源。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 資料中心能源消耗增加

- 更嚴格的溫度控管標準

- 雲端和超大規模基礎設施的成長

- 高密度計算的引入

- 產業潛在風險與挑戰

- 高初始資本投入

- 與舊有系統的複雜整合

- 市場機遇

- 引入液冷技術

- 人工智慧驅動的暖通空調最佳化

- 擴展邊緣資料中心

- 暖通空調即服務 (HaaS)

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國暖氣、冷氣與空調工程師協會

- 美國能源局

- 歐洲

- 歐盟委員會

- Eurovent Certita認證

- 亞太地區

- 新加坡建設局 (BCA)

- JIS-日本工業標準

- 拉丁美洲

- 巴西技術標準協會

- 國家能源委員會

- 中東和非洲

- 阿拉伯聯合大公國(阿拉伯聯合大公國)能源與基礎設施部

- 沙烏地阿拉伯標準、計量和品質組織

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析

- 產品特定定價

- 區域定價

- 生產統計

- 生產基地

- 消費者群體

- 出口和進口

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 關於碳足跡的考量

- 能源效率指標和基準

- 電源使用效率 (PUE) 趨勢

- 水分利用效率(WUE)分析

- 碳利用效率(CUE)指數

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估算與預測:依服務類型分類,2022-2035年

- 解決方案

- 冷卻基礎設施解決方案

- 氣流管理和控制解決方案

- 整合式液冷解決方案

- 暖通空調自動化與控制解決方案

- 熱監測與管理解決方案

- 能源最佳化和自然冷卻解決方案

- 模組化/可擴充冷卻解決方案

- 邊緣資料中心冷卻解決方案

- 服務

- 專業服務

- 諮詢與設計

- 維護和支援

- 安裝和部署

- 託管服務

- 專業服務

第6章 市場估算與預測:依冷凍技術分類,2022-2035年

- 空氣冷卻

- 液冷

- 蒸發冷卻

- 混合冷卻

第7章 市場估計與預測:依設備類型分類,2022-2035年

- 空調系統

- 冷卻器

- 空調機組(AHU)

- 液冷系統

- 冷卻塔

- 節熱器系統

- 控制系統

- 其他

第8章 市場估算與預測:以冷卻方式分類,2022-2035年

- 房間底部冷卻

- 逐行冷卻

- 機架式冷卻

第9章 市場估計與預測:依資料中心分類,2022-2035年

- 企業資料中心

- 託管資料中心

- 超大規模資料中心

- 邊緣資料中心

第10章 市場估價與預測:依最終用途分類,2022-2035年

- 資訊科技/通訊

- BFSI

- 政府/國防

- 衛生保健

- 製造業

- 零售與電子商務

- 能源與公共產業

- 研究與學術

- 其他

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 波蘭

- 羅馬尼亞

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 世界公司

- Alfa Laval

- Carrier Global

- Daikin Industries

- Danfoss

- Hitachi

- Johnson Controls

- Modine

- Schneider Electric

- STULZ

- Trane Technologies

- Vertiv

- 當地公司

- Climaveneta

- Envicool

- Huawei Digital Power

- KyotoCooling

- Mitsubishi Electric

- 新興企業

- Asetek

- CoolIT Systems

- Green Revolution Cooling

- Iceotope Technologies

The Global Data Center HVAC Market was valued at USD 13.7 billion in 2025 and is estimated to grow at a CAGR of 9.8% to reach USD 36 billion by 2035.

Growth in the global data center HVAC market is being fueled by rising computing intensity, expanding AI-driven workloads, and the continued development of hyperscale and enterprise facilities. As server densities increase and high-performance computing environments generate greater thermal loads, advanced cooling infrastructure has become essential to maintain operational stability and uptime. Research and development efforts across the HVAC industry are increasingly focused on liquid cooling technologies and next-generation thermal management systems capable of handling elevated power densities. At the same time, stricter regulatory oversight related to energy consumption and environmental performance is encouraging operators to enhance system efficiency and reduce carbon output. ESG-focused initiatives and net-zero commitments are prompting facility upgrades aimed at optimizing Power Usage Effectiveness and lowering operating expenses. Improvements in airflow engineering, adoption of sustainable refrigerants, and integration of energy-efficient cooling architectures are reshaping infrastructure strategies. As regulatory expectations and energy costs continue to rise, demand for intelligent, high-efficiency HVAC solutions in data centers is expected to accelerate significantly.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.7 Billion |

| Forecast Value | $36 Billion |

| CAGR | 9.8% |

Rising load capacities, sustainability targets, and regulatory compliance requirements are creating pressure for compact, scalable, and adaptable HVAC systems. Industry participants are responding by designing modular cooling platforms that can operate effectively across diverse geographies while maximizing space utilization and energy performance.

The solutions segment accounted for 76% share in 2025 and is forecast to grow at a CAGR of 8.9% from 2026 to 2035. Advanced monitoring tools equipped with artificial intelligence enable predictive maintenance, improve airflow management, and reduce unnecessary power consumption. Increased adoption of liquid-based cooling technologies is supporting high-density server environments while enhancing reliability and extending equipment lifespan through energy-conscious design.

The air-based cooling technologies segment held a 50% share in 2025 and is projected to grow at a CAGR of 8.8% during 2026-2035. Enhanced airflow optimization systems, variable-speed fan configurations, and intelligent environmental controls are improving thermal consistency and minimizing energy waste. Economizer-enabled designs are facilitating greater use of ambient air, while modular cooling units support scalability across both hyperscale and edge environments. Growing server power density is also accelerating interest in direct cooling and immersion-based methods supported by advanced coolant formulations that enhance heat transfer efficiency.

United States Data Center HVAC Market reached USD 4.7 billion in 2025. Increasing cloud integration and AI-intensive applications are driving demand for more efficient cooling architectures. Investments are being supported by electrification incentives and decarbonization initiatives, encouraging broader adoption of intelligent HVAC controls and energy-optimized systems. Integration with smart building platforms and grid-responsive technologies is enabling facilities to manage peak loads, reduce demand charges, and incorporate renewable energy sources.

Key companies operating in the Global Data Center HVAC Market include Vertiv, Schneider Electric, Carrier Global, Daikin Industries, Trane Technologies, Johnson Controls, STULZ, Alfa Laval, Danfoss, and Modine Manufacturing. Companies in the Global Data Center HVAC Market are strengthening their competitive position through continuous innovation, strategic partnerships, and geographic expansion. Leading players are investing heavily in research and development to enhance liquid cooling efficiency, improve airflow intelligence, and integrate AI-driven monitoring systems. Collaborations with cloud service providers and data center developers are enabling customized cooling deployments for high-density environments. Firms are also expanding manufacturing capacity and regional service networks to support rapid infrastructure growth. Sustainability-focused product development, including low-global-warming-potential refrigerants and energy-efficient system architectures, is becoming a central competitive differentiator.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Cooling technology

- 2.2.4 Equipment level

- 2.2.5 Cooling technique

- 2.2.6 Data center

- 2.2.7 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising data center energy consumption

- 3.2.1.2 Stricter thermal management standards

- 3.2.1.3 Growth in cloud & hyperscale infrastructure

- 3.2.1.4 Adoption of high-density computing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital expenditure

- 3.2.2.2 Complex integration with legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 Liquid cooling adoption

- 3.2.3.2 AI-driven HVAC optimization

- 3.2.3.3 Edge data center expansion

- 3.2.3.4 HVAC as a service (HaaS)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 American Society of Heating, Refrigerating and Air-Conditioning Engineers

- 3.4.1.2 U.S. Department of Energy

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 Eurovent Certita Certification

- 3.4.3 Asia Pacific

- 3.4.3.1 BCA - Building and Construction Authority (Singapore)

- 3.4.3.2 JIS - Japanese Industrial Standards

- 3.4.4 Latin America

- 3.4.4.1 Associacao Brasileira de Normas Tecnicas

- 3.4.4.2 Comision Nacional de Energia

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Ministry of Energy and Infrastructure

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 Pricing by product

- 3.8.2 Pricing by region

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Energy Efficiency Metrics & Benchmarking

- 3.13.1 Power Usage Effectiveness (PUE) Trends

- 3.13.2 Water Usage Effectiveness (WUE) Analysis

- 3.13.3 Carbon Usage Effectiveness (CUE) Metrics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Solutions

- 5.2.1 Cooling infrastructure solutions

- 5.2.2 Airflow management & containment solutions

- 5.2.3 Liquid cooling integration solutions

- 5.2.4 HVAC automation & control solutions

- 5.2.5 Thermal monitoring & management solutions

- 5.2.6 Energy optimization & free cooling solutions

- 5.2.7 Modular / scalable cooling solutions

- 5.2.8 Edge data center cooling solutions

- 5.3 Services

- 5.3.1 Professional services

- 5.3.1.1 Consulting & design

- 5.3.1.2 Maintenance and support

- 5.3.1.3 Installation and deployment

- 5.3.2 Managed services

- 5.3.1 Professional services

Chapter 6 Market Estimates & Forecast, By Cooling Technology, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Air-based cooling

- 6.3 Liquid cooling

- 6.4 Evaporative cooling

- 6.5 Hybrid cooling

Chapter 7 Market Estimates & Forecast, By Equipment-Level, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Air conditioning systems

- 7.3 Chillers

- 7.4 Air handling units (AHU)

- 7.5 Liquid cooling systems

- 7.6 Cooling towers

- 7.7 Economizer systems

- 7.8 Control systems

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Cooling Technique, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Room-based cooling

- 8.3 Row-based cooling

- 8.4 Rack-based cooling

Chapter 9 Market Estimates & Forecast, By Data Center, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Enterprise data centers

- 9.3 Colocation data centers

- 9.4 Hyperscale data centers

- 9.5 Edge data centers

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 IT & telecommunications

- 10.3 BFSI

- 10.4 Government & defense

- 10.5 Healthcare

- 10.6 Manufacturing

- 10.7 Retail & e-commerce

- 10.8 Energy & utilities

- 10.9 Research & academic

- 10.10 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.3.8 Poland

- 11.3.9 Romania

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Vietnam

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 Alfa Laval

- 12.1.2 Carrier Global

- 12.1.3 Daikin Industries

- 12.1.4 Danfoss

- 12.1.5 Hitachi

- 12.1.6 Johnson Controls

- 12.1.7 Modine

- 12.1.8 Schneider Electric

- 12.1.9 STULZ

- 12.1.10 Trane Technologies

- 12.1.11 Vertiv

- 12.2 Regional players

- 12.2.1 Climaveneta

- 12.2.2 Envicool

- 12.2.3 Huawei Digital Power

- 12.2.4 KyotoCooling

- 12.2.5 Mitsubishi Electric

- 12.3 Emerging players

- 12.3.1 Asetek

- 12.3.2 CoolIT Systems

- 12.3.3 Green Revolution Cooling

- 12.3.4 Iceotope Technologies

自足式內常冷裝置市場:依產品類型、容量、機架密度、冷卻劑類型、應用、終端用戶產業分類,全球預測,2026-2032年

自足式內常冷裝置市場:依產品類型、容量、機架密度、冷卻劑類型、應用、終端用戶產業分類,全球預測,2026-2032年 企業伺服器電源和冷卻解決方案及服務市場至2030年預測:按解決方案類型、服務類型、部署模式、企業規模、最終用戶和地區的全球分析

企業伺服器電源和冷卻解決方案及服務市場至2030年預測:按解決方案類型、服務類型、部署模式、企業規模、最終用戶和地區的全球分析