|

市場調查報告書

商品編碼

1982260

資料中心熱交換器市場機會、成長要素、產業趨勢分析及2026-2035年預測。Data Center Heat Exchanger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

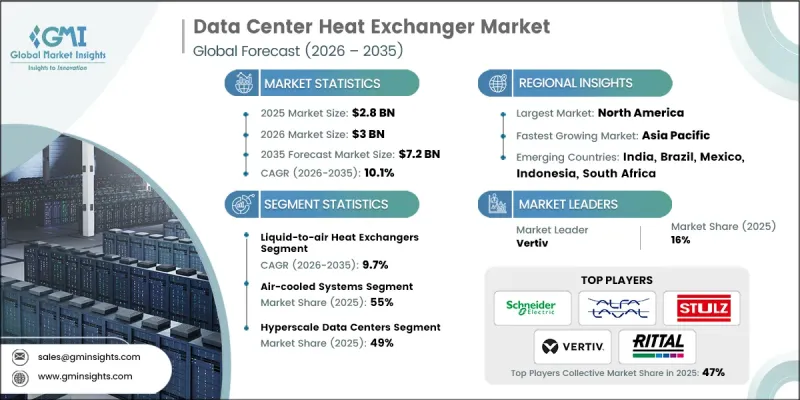

2025 年全球資料中心熱交換器市場價值為 28 億美元,預計到 2035 年將達到 72 億美元,年複合成長率為 10.1%。

隨著先進的溫度控管對於數位基礎設施的性能至關重要,該行業正展現出強勁的發展勢頭。隨著人工智慧 (AI) 應用、雲端環境和分散式運算架構的不斷擴展,資料中心營運商正優先考慮高效且永續的冷卻技術。熱交換器在維持運作、最佳化電源利用效率以及支援高機架密度方面發揮核心作用。市場涵蓋了空氣-空氣、液-液和冷媒冷卻技術,這些技術整合於後門系統、龍頭平台和直接晶片 (DTC) 液冷架構中。機架功率密度超過 30-100 kW 的不斷成長正在加速從傳統風冷模式轉向液冷和混合系統的轉變。人工智慧處理器和高效能運算元件的廣泛應用進一步增加了對緊湊型板式和微通道熱交換器的需求,這些熱交換器旨在最大限度地減少水和能源消耗,同時提高傳熱效率。監管壓力、成本效益目標以及超大規模和託管設施的持續創新也是推動市場成長的因素。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 28億美元 |

| 預測金額 | 72億美元 |

| 複合年成長率 | 10.1% |

預計到2025年,液-氣熱交換器市佔率將達到54%,並在2026年至2035年間以9.7%的複合年成長率成長。此類別是許多資料中心的基礎冷卻方式,包括後門熱交換器、冷水空調系統和整合式盤管技術。這些解決方案利用水卓越的吸熱能力,透過專用熱交換表面將伺服器排氣中的熱能傳遞到資料中心,並在資料中心內循環使用處理後的空氣。與現有基礎設施的高度相容性持續推動該技術的廣泛應用。

到2025年,風冷系統市佔率將達到55%,預計到2035年將以9.8%的複合年成長率成長。此細分市場包括採用直接膨脹式冷媒技術的自然冷卻配置、冷水空氣處理機組、獨立式冷卻器和節熱器。長期以來,風冷系統憑藉其在業界的廣泛認可、久經考驗的可靠性以及與高風量設計的兼容性,鞏固了其市場主導地位。風冷平台尤其適用於每機架運作為5-15千瓦的企業環境,在這些環境中,安裝成本和操作便利性仍是關鍵考量。

美國資料中心熱交換器市場預計到2025年將達到7.821億美元,並在2026年至2035年間以9.4%的複合年成長率成長。超大規模資料中心的持續發展、嚴格的能源效率法規以及聯邦監管機構的監督,都支撐著該市場的主導地位。對運算密集型工作負載和數位服務的需求不斷成長,正在加速向高性能冷卻技術的轉型,而液氣熱交換器因其可靠性和節能性而備受青睞。

競爭格局中的主要參與者包括Airedale、Alfa Laval、CoolIT Systems、Eaton、Munters、Nortek Air、Rittal、Schneider Electric、STULZ和Vertiv等,它們都在為產品創新和全球市場擴張做出貢獻。在全球資料中心熱交換器市場中營運的公司正透過技術創新、策略聯盟和產能擴張來鞏固其市場地位。製造商正大力投資研發,以推出先進的液冷系統、緊湊型微通道設計以及針對高密度資料中心最佳化的節能混合解決方案。與資料中心開發商和基礎設施供應商的策略合作有助於儘早整合客製化溫度控管系統。各公司也正在擴大其製造工廠和區域分銷網路,以滿足北美和其他高成長地區日益成長的需求。此外,他們也致力於以永續發展為導向的產品改進,以減少用水量和碳排放,從而符合監管要求和公司ESG(環境、社會和管治)計劃。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 人工智慧和高效能運算工作負載的快速成長

- 不斷提高的熱密度(50-100 kW 機架)和 GPU 發熱量(每個晶片超過 1200 W)

- 永續發展法規與淨零碳排放目標

- 傳統空氣冷卻方式在現代工作負載下的局限性

- 超大規模資料中心擴建

- 降低能源成本的壓力

- 產業潛在風險與挑戰

- 液冷基礎設施需要大量的初始投資。

- 對用水的擔憂

- 與傳統空氣冷卻基礎設施整合面臨的挑戰

- 液冷系統安裝和維護方面的熟練工人短缺。

- 避免電子設備周圍液體流入的風險。

- 市場機遇

- 傳統資料中心維修市場

- 邊緣和微型資料中心的冷卻解決方案

- 廢熱回收再利用的應用

- 模組化和預製冷卻單元

- 耐候性強的冷卻系統,設計用於承受極端溫度環境。

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國暖氣、冷氣與空調工程師協會(ASHRAE)

- 美國能源局(DOE)

- 歐洲

- 歐盟委員會

- Eurovent Certita認證

- 亞太地區

- 新加坡建設局(BCA)

- 日本工業標準(JIS)

- 拉丁美洲

- 巴西技術標準協會

- 國家能源委員會

- 中東和非洲

- 阿拉伯聯合大公國(阿拉伯聯合大公國)能源與基礎設施部

- 沙烏地阿拉伯標準、計量和品質組織(SASO)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利分析

- 專利申請趨勢(2021-2025)

- 主要專利擁有者

- 價格分析與成本結構

- 按技術類型分類的價格趨勢

- 各地區價格波動

- 成本細分分析

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 關於碳足跡的考量

- 總擁有成本 (TCO) 分析

- 使用案例和成功案例

- 未來展望與新趨勢

- 新一代冷卻解決方案(液體浸沒式冷卻、兩相冷卻、低溫冷卻)

- 人工智慧驅動的預測性溫度控管

- 循環經濟和熱能再利用的潛力

- 智慧模組化和邊緣運算基礎設施

- 營運效率和最佳化

- 能源最佳化方法

- 生命週期成本管理

- 維護和預測性維護實踐

- 與建築管理系統(BMS)整合

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估算與預測:依熱交換器技術分類,2022-2035年

- 液氣熱交換器

- 液-液熱交換器

- 混合式熱交換器

第6章 市場估計與預測:依冷卻方式分類,2022-2035年

- 空冷系統

- 液冷系統

- 混合氣液解決方案

第7章 市場估算與預測:依冷凍裝置配置分類,2022-2035年

- 後門熱交換器(RDHx)

- Inro冷卻裝置

- 直接冷卻液冷卻(冷板)

- 浸沒式冷卻系統

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 伺服器冷

- 電力電子設備(UPS、PDU)的冷卻

- 暖通空調系統整合

- 通風和空氣交換

- 能源回收/餘熱再利用

- 其他

第9章 市場估計與預測:依資料中心分類,2022-2035年

- 超大規模資料中心

- 企業資料中心

- 託管資料中心

- 邊緣/微型資料中心

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 瑞典

- 丹麥

- 波蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 以色列

第11章:公司簡介

- 世界公司

- Airedale

- Alfa Laval

- Emerson

- Mitsubishi Heavy Industries

- Munters

- Nortek Air

- Rittal

- Schneider Electric

- STULZ

- Vertiv

- 當地公司

- Baltimore Aircoil Company(BAC)

- Coolcentric

- Fujitsu

- Hitachi

- Legrand(ColdLogik)

- Motivair

- USystems

- 新興企業和技術基礎設施公司

- CoolIT Systems

- Green Revolution Cooling(GRC)

- ZutaCore

The Global Data Center Heat Exchanger Market was valued at USD 2.8 billion in 2025 and is estimated to grow at a CAGR of 10.1% to reach USD 7.2 billion by 2035.

The industry is gaining strong momentum as advanced thermal management becomes critical to digital infrastructure performance. As artificial intelligence applications, cloud environments, and distributed computing architectures continue to scale, data center operators are prioritizing efficient and sustainable cooling technologies. Heat exchangers now play a central role in maintaining uptime, optimizing power usage effectiveness, and supporting higher rack densities. The market covers air-to-air, liquid-to-liquid, and refrigerant-based technologies integrated into rear-door systems, in-row platforms, and direct-to-chip liquid cooling architectures. Increasing rack power densities exceeding 30-100 kW are accelerating the transition from legacy air-based models toward liquid and hybrid systems. The widespread deployment of AI processors and high-performance computing components is further elevating demand for compact plate and microchannel heat exchangers designed to improve thermal transfer while minimizing water and energy consumption. Growth is also supported by regulatory pressure, cost efficiency goals, and continuous innovation in hyperscale and colocation facilities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.8 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 10.1% |

The liquid-to-air heat exchangers segment accounted for 54% share in 2025 and is anticipated to grow at a CAGR of 9.7% between 2026 and 2035. This category represents the foundational cooling approach within many data centers, incorporating rear-door heat exchangers, chilled-water-based air handling systems, and integrated coil technologies. These solutions rely on water's strong heat absorption capacity, transferring thermal energy from server exhaust air through engineered exchange surfaces before recirculating conditioned air back into the facility. Their established infrastructure compatibility continues to drive widespread adoption.

The air-cooled systems segment held a 55% share in 2025 and is forecast to grow at a CAGR of 9.8% through 2035. This segment includes direct expansion refrigerant technologies, chilled water air handlers, standalone chillers, and economizer-based free cooling configurations. Long-standing industry familiarity, proven reliability, and compatibility with raised-floor airflow designs have reinforced their dominance. Air-cooled platforms remain particularly effective for enterprise environments operating at 5-15 kW per rack, where installation costs and operational simplicity remain primary considerations.

United States Data Center Heat Exchanger Market generated USD 782.1 million in 2025 and is estimated to grow at a CAGR of 9.4% during 2026-2035. Market leadership is supported by continued hyperscale development, strict energy efficiency mandates, and oversight from federal regulatory bodies. Rising demand for compute-intensive workloads and digital services is accelerating the shift toward high-performance cooling technologies, with liquid-to-air heat exchangers recognized for dependable and energy-efficient operation.

The competitive landscape includes key industry participants such as Airedale, Alfa Laval, CoolIT Systems, Eaton, Munters, Nortek Air, Rittal, Schneider Electric, STULZ, and Vertiv, all contributing to product innovation and global market expansion. Companies operating in the Global Data Center Heat Exchanger Market are strengthening their market position through technology innovation, strategic partnerships, and capacity expansion initiatives. Manufacturers are investing heavily in research and development to introduce advanced liquid cooling systems, compact microchannel designs, and energy-efficient hybrid solutions tailored for high-density data centers. Strategic collaborations with data center developers and infrastructure providers enable early integration of customized thermal management systems. Firms are also expanding manufacturing facilities and regional distribution networks to meet growing demand across North America and other high-growth regions. In addition, companies are focusing on sustainability-driven product enhancements that reduce water consumption and carbon emissions, aligning with regulatory expectations and enterprise ESG commitments.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Heat Exchanger Technology

- 2.2.3 Cooling Mechanisms

- 2.2.4 Cooling Deployment Configuration

- 2.2.5 Application

- 2.2.6 Data Centers

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Exponential growth in AI and high-performance computing workloads

- 3.2.1.2 Rising thermal density (50-100 kW racks) and GPU heat generation (1,200 W+ per chip)

- 3.2.1.3 Sustainability mandates and net-zero carbon emission targets

- 3.2.1.4 Inadequacy of traditional air-cooling for modern workloads

- 3.2.1.5 Hyperscale data center expansion

- 3.2.1.6 Energy cost reduction pressure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment requirements for liquid-cooling infrastructure

- 3.2.2.2 Water consumption concerns

- 3.2.2.3 Integration challenges with legacy air-cooled infrastructure

- 3.2.2.4 Skilled workforce shortage for liquid-cooling installation and maintenance

- 3.2.2.5 Risk aversion to liquid near electronic equipment

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit market for legacy data centers

- 3.2.3.2 Edge and micro data center cooling solutions

- 3.2.3.3 Waste heat recovery and reuse applications

- 3.2.3.4 Modular and prefabricated cooling units

- 3.2.3.5 Climate-resilient cooling for extreme-temperature environments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 American society of heating, refrigerating and air-conditioning engineers (ASHRAE)

- 3.4.1.2 US department of energy (DOE)

- 3.4.2 Europe

- 3.4.2.1 European commission

- 3.4.2.2 Eurovent certita certification

- 3.4.3 Asia Pacific

- 3.4.3.1 Building and construction authority (BCA), Singapore

- 3.4.3.2 Japanese industrial standards (JIS)

- 3.4.4 LATAM

- 3.4.4.1 Brazilian association of technical standards

- 3.4.4.2 National energy commission

- 3.4.5 MEA

- 3.4.5.1 UAE ministry of energy and infrastructure

- 3.4.5.2 Saudi standards, metrology and quality organization (SASO)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.8.1 Patent filing trends (2021-2025)

- 3.8.2 Key patent holders

- 3.9 Pricing analysis & cost structure

- 3.9.1 Price trends by technology type

- 3.9.2 Regional price variations

- 3.9.3 Cost breakdown analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Total cost of ownership (tco) analysis

- 3.12 Use cases & success stories

- 3.13 Future outlook & emerging trends

- 3.13.1 Next-generation cooling solutions (immersion, two-phase, cryogenic)

- 3.13.2 AI-enabled predictive thermal management

- 3.13.3 Circular economy & heat reuse potential

- 3.13.4 Smart modular & edge-ready infrastructure

- 3.14 Operational efficiency & optimization

- 3.14.1 Energy optimization techniques

- 3.14.2 Lifecycle cost management

- 3.14.3 Maintenance & predictive monitoring practices

- 3.14.4 Integration with building management systems (BMS)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Heat Exchanger Technology, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Liquid-to-air heat exchangers

- 5.3 Liquid-to-liquid heat exchangers

- 5.4 Hybrid heat exchangers

Chapter 6 Market Estimates & Forecast, By Cooling Mechanisms, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Air-cooled systems

- 6.3 Liquid-cooled systems

- 6.4 Hybrid air/liquid solutions

Chapter 7 Market Estimates & Forecast, By Cooling Deployment Configuration, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Rear door heat exchangers (RDHx)

- 7.3 In-row cooling units

- 7.4 Direct-to-chip liquid cooling (Cold Plates)

- 7.5 Immersion cooling systems

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Server cooling

- 8.3 Power electronics cooling (UPS, PDUs)

- 8.4 HVAC systems integration

- 8.5 Ventilation & air exchange

- 8.6 Energy recovery / waste heat reuse

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Data Centers, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Hyperscale data centers

- 9.3 Enterprise data centers

- 9.4 Colocation data centers

- 9.5 Edge/micro data centers

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Airedale

- 11.1.2 Alfa Laval

- 11.1.3 Emerson

- 11.1.4 Mitsubishi Heavy Industries

- 11.1.5 Munters

- 11.1.6 Nortek Air

- 11.1.7 Rittal

- 11.1.8 Schneider Electric

- 11.1.9 STULZ

- 11.1.10 Vertiv

- 11.2 Regional Players

- 11.2.1 Baltimore Aircoil Company (BAC)

- 11.2.2 Coolcentric

- 11.2.3 Fujitsu

- 11.2.4 Hitachi

- 11.2.5 Legrand (ColdLogik)

- 11.2.6 Motivair

- 11.2.7 USystems

- 11.3 Emerging Players & Technology Enablers

- 11.3.1 CoolIT Systems

- 11.3.2 Green Revolution Cooling (GRC)

- 11.3.3 ZutaCore

2026-2030年全球熱交換器市場

2026-2030年全球熱交換器市場 熱交換器市場:2026-2032年全球市場預測(依產品類型、結構材料、流動佈局、熱交換機制、相態、壓力等級、最終用途、熱負荷、安裝類型和銷售管道)

熱交換器市場:2026-2032年全球市場預測(依產品類型、結構材料、流動佈局、熱交換機制、相態、壓力等級、最終用途、熱負荷、安裝類型和銷售管道) 板式熱交換器市場:按產品類型、應用和地區分類

板式熱交換器市場:按產品類型、應用和地區分類 熱交換器市場規模、佔有率和成長分析:按產品類型、材質、應用和地區分類-2026-2033年產業預測

熱交換器市場規模、佔有率和成長分析:按產品類型、材質、應用和地區分類-2026-2033年產業預測 熱交換器市場規模、佔有率、趨勢和預測:按產品、材質、終端用戶產業和地區分類,2026-2034年

熱交換器市場規模、佔有率、趨勢和預測:按產品、材質、終端用戶產業和地區分類,2026-2034年 氫燃料加註站用熱交換器:全球市場佔有率和排名、總收入和需求預測(2026-2032年)地熱熱交換器市場:類型、技術、安裝配置、應用和最終用途—2026-2032年全球市場預測

氫燃料加註站用熱交換器:全球市場佔有率和排名、總收入和需求預測(2026-2032年)地熱熱交換器市場:類型、技術、安裝配置、應用和最終用途—2026-2032年全球市場預測 2026年板翅式盤管全球市場報告熱交換器市場:按原料、應用和地區分類2026年全球地熱供暖和製冷市場報告

2026年板翅式盤管全球市場報告熱交換器市場:按原料、應用和地區分類2026年全球地熱供暖和製冷市場報告